SNB, Riksbank and BoJ all leave rates unchanged while markets await BoE and ECB - Newsquawk US Market Open

- Iran's armed forces said Iran's retaliation against attacks on its energy infrastructure is not yet complete, SNN reported; any repeat of such attacks will lead to a far stronger retaliation against the enemy, enemy infrastructure and that of their allies.

- US President Trump said Israel violently lashed out at Iran's major facility and that the US did not know about the attack, while he said there will be no more attacks by Israel on South Pars; added that the US will retaliate by massively blowing up the entirety of the South Pars Gas Field if Qatar's LNG is attacked again.

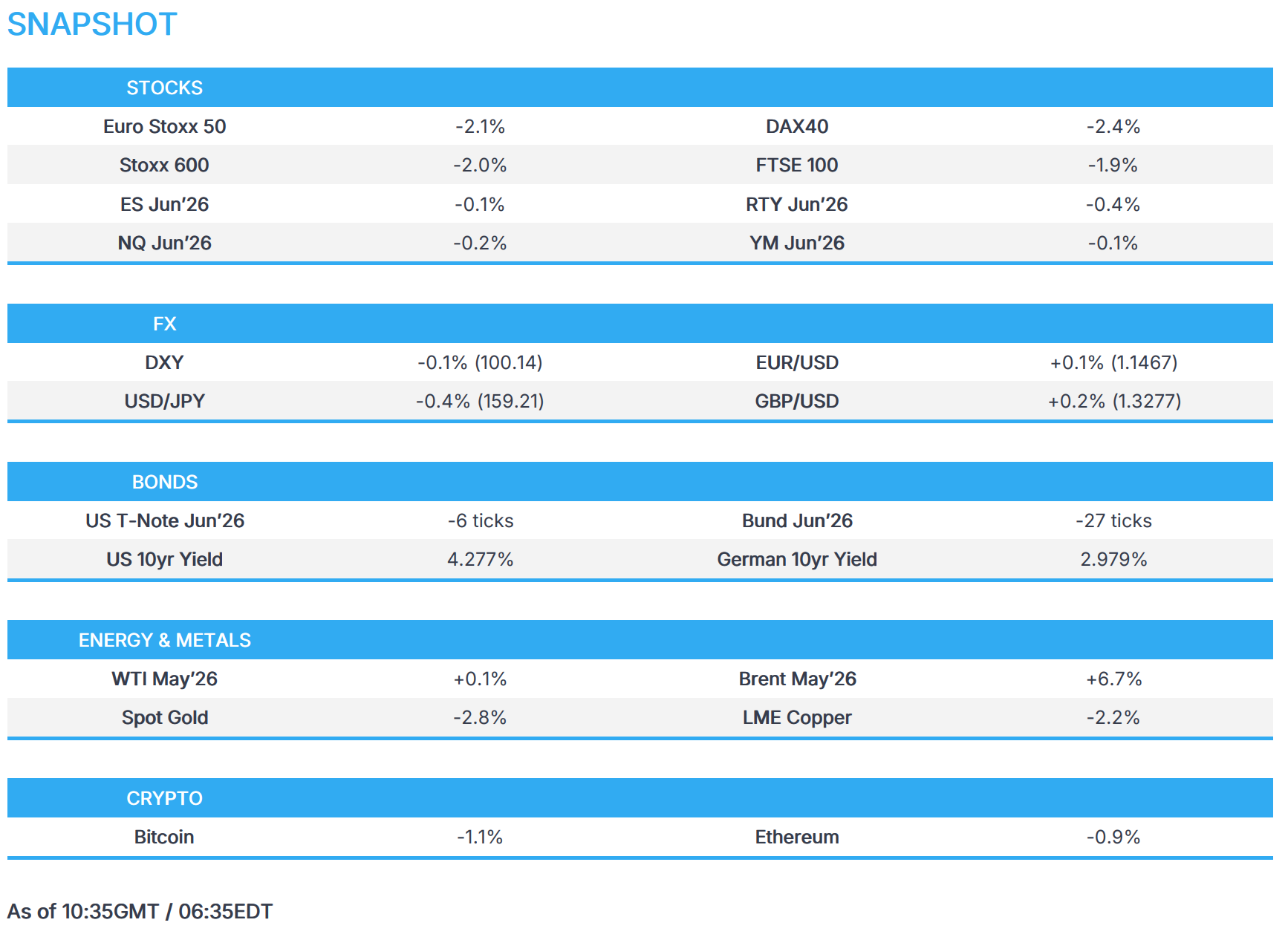

- FX mixed amid the central bank bonanza; SNB, Riksbank and BoJ all left rates unchanged, as expected, while the BoE and ECB await.

- Crude surges as attacks in the Persian Gulf threaten long-term damage to major energy facilities.

- European equities suffer as Energy continues to surge; US equity futures follow suit, Micron slips after increasing capex plans.

- Fixed income weighed on energy upside and hawkish Chair Powell.

- Looking ahead, highlights include US Initial Jobless Claims (Mar/14), Atlanta Fed GDP, New Zealand Trade Balance (Feb), BoE & ECB Policy Announcements. Speakers include ECB's Lagarde. Supply from the US. Earnings from FedEx.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European Bourses are broadly lower as renewed attacks on energy infrastructure weigh on risk sentiment. The DAX 40 underperforms, pressured by Vonovia despite its return to profitability and plans to sell around EUR 5bln in assets to reduce debt.

- Sectors are weak across the board. Basic Resources lag as precious metals decline, while Travel & Leisure also underperforms. Energy is the relative outperformer, supported by elevated prices and policy support in Italy, benefiting names such as Eni.

- US equity futures extend losses, with ES slipping below its 200-SMA. Weakness is compounded by Micron Technology, which falls despite earnings beating estimates after flagging higher capex, alongside broader risk-off sentiment.

- Alibaba Group (9988 HK / BABA) Q3 (CNY): Revenue 284.8bln (prev. 289.8bln), Adj. EBITDA 34.1bln (exp. 39.6bln), well-positioned to drive growth on both enterprise AI and consumer AI fronts.

- CK Hutchinson (0001 HK) FY (HKD): Net Income 11.84bln (exp. 21.74bln), Total Revenue 507.3bln (exp. 483.5bln), EBIT 57.6bln (exp. 59.3bln).

- Samsung Electronics (005930 KS) plans in excess of KRW 110tln (exp. 65tln) of capex and R&D spending during 2026. Seeking meaningful M&A for robots, medical tech, auto electronics and HVAC.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is flat but off lows, holding above 100 in a 99.99–100.31 range as higher oil prices and a hawkish Fed backdrop support the dollar. Powell signalled policy remains restrictive with no imminent cuts, reinforcing inflation concerns tied to the Middle East energy shock.

- JPY is firmer post-BoJ, driven by hawkish signals from Governor Ueda highlighting improving wage momentum. USD/JPY trades towards the lower end of a 159.04–159.87 range.

- EUR is flat, with USD recovery capping upside while elevated energy prices limit downside ahead of the ECB. Focus is on whether the ECB shifts to a more hawkish tone amid rising inflation risks, though growth concerns remain. EUR/USD trades in a 1.1443–1.1491 range.

- GBP trades subdued, sitting near the bottom of a 1.3245–1.3298 range as USD strength offsets limited domestic drivers. BoE expected to hold, with potential dovish dissent, though the energy shock may anchor a unanimous decision.

- CHF is weaker post-SNB after explicit FX intervention language signals readiness to counter excessive strength. Initial CHF weakness pares as this stance was largely expected, with EUR/CHF moving up towards 0.9100.

- SEK trades largely unchanged following the Riksbank decision, which keeps policy steady and maintains flexibility amid uncertainty from the Middle East-driven energy shock.

- Antipodeans are firmer, recovering recent losses. NZD/USD shrugs off weak GDP, while AUD/USD remains choppy after mixed labour data, with gains supported by broader USD stabilisation.

FIXED INCOME

- UST are bearish following the hawkish tone from Powell and continued strength in energy prices. Futures drop around 15 ticks post-Fed, holding near session lows around 111-08 as higher oil and gas prices reinforce inflation concerns and keep yields elevated.

- Bund futures are weaker, down 40 ticks at most with a trough near 125.70 as surging Dutch TTF gas and elevated crude push ECB pricing more hawkish. Focus turns to the ECB, which is expected to hold rates but likely revise inflation higher and growth lower.

- Gilts underperform, gapping lower by 92 ticks and extending to an 88.32 low amid the global fixed income sell-off driven by energy and central bank hawkishness. Attention turns to the BoE, where rates are expected unchanged, with focus on the vote split and policy guidance.

- France sold EUR 12.399 vs exp. EUR 10.5-12.5bln 2.40% 2029, 2.50% 2030, 2.70% 2031 and 3.50% 2033 OAT.

- Spain sold EUR 5.546 vs exp. EUR 5.0-6.0bln 2.60% 2031, 2.55% 2032 and 3.30% 2036 Bono.

COMMODITIES

- Crude futures surge on escalation in the Iran war, with attacks on Gulf energy infrastructure across Saudi Arabia, Qatar, and Kuwait driving a sharp risk premium. Brent approaches USD 119.5/bbl at peak, with WTI lagging and trading at a wide ~USD 12/bbl discount, the largest spread since 2015. The disruption is amplified by threats to alternative routes such as Saudi Arabia’s Yanbu, a key Red Sea export hub used to bypass Hormuz, although prices pull back slightly after reports loadings resume.

- Spot gold extends losses, breaking below USD 4,700/oz as a firmer USD and rising rate expectations (driven by energy-led inflation risk) outweigh safe-haven demand despite ongoing conflict.

- Base metals remain under pressure in a risk-off environment. Copper erases 2026 gains as higher oil prices weigh on global growth expectations and demand, with prices trading in a USD 12,041–12,326/t range.

- Saudi Arabia's Yanbu port reportedly resumes oil loadings, sources say. This comes following reports that oil loading were stopped.

- Gazprom said Ukraine increased attacks on Turkstream and Bluestream pipelines on 17-19th March; said all attacks were foiled.

- Abu Dhabi government noted operations have been suspended at the Habshan gas facility, while authorities are dealing with two incidents of falling debris from successfully intercepted missiles that targeted that gas facility.

TRADE/TARIFFS

- European Parliament's Trade's Committee officially approves legislation to cut import duties for US products as part of the Turnberry trade agreement with the US.

- China's Commerce Ministry, on reported of NVIDIA (NVDA) H200 purchases; said not aware of the situation.

- China's Commerce Ministry, on proposed US-China board of trade and investment, said both sides agreed in Paris to study a framework.

- US and Mexico announce next steps ahead of USMCA review, while USTR said they are to explore options to boost manufacturing jobs.

NOTABLE EUROPEAN DATA RECAP

- UK Unemployment Rate (Jan) 5.2% vs. Exp. 5.3% (Prev. 5.2%, Low. 5.2%, High. 5.3%).

- UK Employment Change (Jan) 84K vs. Exp. -4K (Prev. 52K).

- UK Average Earnings excl. Bonus (3Mo/Yr) (Jan) 3.8% vs. Exp. 4.0% (Prev. 4.2%, Low. 4.0%, High. 4.3%).

- UK Average Earnings incl. Bonus (3Mo/Yr) (Jan) 3.9% vs. Exp. 3.9% (Prev. 4.2%).

- UK HMRC Payrolls Change (Feb) 20K vs. Exp. 5K (Prev. -11K).

- UK Claimant Count Change (Feb) 24.7K vs. Exp. 25.8K (Prev. 28.6K).

CENTRAL BANKS

- BoJ kept its short-term rates at 0.75%, as unanimously forecast, with the decision made by 8-1 vote, as board member Takata voted for a 25bps hike. BoJ refrained from any major surprises, reiterating that it will continue to raise policy rates if the economy and prices move in line with its forecasts and will conduct monetary policy as appropriate from the perspective of sustainably and stably achieving the 2% inflation target. Furthermore, it stated the economy is likely to continue growing moderately and inflation expectations have risen moderately, while consumer inflation is likely to briefly slow below 2% and re-accelerate due to the impact of rising oil prices, with the price trend is to be in line with the goal in the second half of the outlook.

- SNB maintains its Policy rate at 0.00% as expected; prepared to intervene in currency markets to country currency appreciation if needed; "willingness to intervene in the foreign exchange market has increased". The statement points to heightened uncertainty given the Middle East conflict. The main point of the statement was the FX language, commentary that sparked immediate pressure in the CHF as the SNB stated explicitly that it would counter rapid and excessive appreciation.

- Riksbank leaves its policy rate unchanged at 1.75% as expected; rate is expected to remain at this level for some time to come. The Riksbank has kept its optionality open in whether the Middle East shock will lead to tighter or looser or monetary policy. A point evidenced by the scenario analysis that explores the avenues that could lead to either option. Additionally, the forecast adjustment for 2026 underscores this with the CPIF view increased while the growth view has been cut. But, pertinently, the policy path projection is unchanged vs the last MPR.

- Norges Bank Q1 Regional Network Survey: Expect minor changes in output growth in the period to summer. Contacts expect annual wage growth of 4.2% in 2026 and 3.9% in 2027.

- Brazilian Interest Rate Decision 14.75% vs. Exp. 14.75% (Prev. 15%), decision was unanimous. BCB reaffirms serenity and caution. Future interest rate decisions will incorporate new information on Middle East conflict depth and duration. Committee deemed it appropriate to begin the monetary policy calibration cycle.

- Taiwan Central Bank leaves rates unchanged at 2.00%, as expected.

NOTABLE US HEADLINES

- Top Senate Democrats Schumer, Warren and Wyden plan to urge President Trump to end tariffs, issue refunds and stop the Iran war, arguing his policies are raising costs, Semafor reported.

- US President Trump's meeting with Japanese PM Takaichi at the White House is scheduled for 11.15EDT/15:15GMT on Thursday and they will have dinner at 19:15EDT/23:15GMT.

GEOPOLITICS

MIDDLE EAST

- Iran's armed forces said Iran's retaliation against attacks on its energy infrastructure is not yet complete, SNN reported.

- Iranian lawmaker said parliament is mulling passing a bill that would impose toll and tax on ships seeking safe passage in the Strait of Hormuz, ISNA reported.

- US embassy says Americans should leave Saudi Arabia immediately.

- US President Trump said Israel violently lashed out at Iran's major facility and the US did not know about the attack, while he called for no more attacks by Israel on South Pars and threatens the US will retaliate if Qatar's LNG is attacked again.

- US officials say President Trump wants no more energy strikes but supported the attack on South Pars, and could once again be open to targeting additional Iranian energy facilities depending on Iran's actions in Strait of Hormuz, according to WSJ.

- US President Trump's administration is considering deploying thousands of additional US troops to the Middle East as Trump weighs Iran next steps, according to sources cited by Reuters.

- US Pentagon seeks more than USD 200bln in budget requests for Iran war, according to Washington Post.

- Israeli official said war has moved into a new phase and may last several more weeks.

- Saudi Foreign Minister said Iran must review 'misjudgements', and attacks will bring no gains, demands Iran stop proxy support and protect maritime navigation immediately, adds Iran has dealt with neighbours not in a brotherhood but with a hostile view. Added that Saudi Arabia reserves the right to take military action against Iran.

- Saudi Arabia's Defence Ministry said a drone has fallen on the Samref refinery, currently assessing the damage.

- Missile reportedly hit the Yanbu refinery in Saudi Arabia's Red Sea coast, according to Iran's semi official SNN.

- Kuwait Petroleum Corporation said one of the operational units at Mina Al-Ahmadi refinery was targeted on Thursday by a drone, resulting in limited fire, no casualties reported.

- QatarEnergy said natural gas and LNG facilities at were subjected to missile attacks causing fire and more severe damage.

- French President Macron said he spoke with the Emir of Qatar and President Trump following the strikes that hit gas production sites in Iran and Qatar. Said, "It is in the common interest to implement without delay a moratorium on strikes targeting civilian infrastructure, particularly energy and water infrastructure.".

- Security sources say a drone attack targets Iraqi naval forces based near Umm Qasr Port, although no casualties or damage that were reported.

- Iraqi armed group Kataib Hezbollah announces suspension of attacks on the US embassy for five days, subject to conditions.

- The escalation on the Lebanon front may continue regardless of the Iran war, Al Arabiya reported citing an Israeli security source.

RUSSIA-UKRAINE

- Russia's Kremlin said trilateral US-Russia-Ukraine negotiations are on pause, but investment talks are to continue.

CRYPTO

- Bitcoin falls below USD 71k, while Ethereum remains above USD 2k.

APAC TRADE

- APAC stocks declined as the region took its cue from the losses stateside, where the major indices suffered amid higher oil prices and yields, following energy infrastructure attacks in the Middle East and hawkish Powell comments.

- ASX 200 was dragged lower by losses in miners, materials and real estate, with sentiment not helped by mixed jobs data.

- Nikkei 225 suffered from the higher oil prices and as markets awaited the BoJ policy decision, which provided no major surprises, while the attention now turns to more central bank announcements, as well as the Trump-Takaichi summit later.

- Hang Seng and Shanghai Comp conformed to the broad risk-off mood with tech hit by weakness in semiconductors and following Tencent's earnings, while miners and airlines were also pressured after a decline in metal prices and surge in oil.

NOTABLE ASIA-PAC HEADLINES

- China's Industry Minister said China is to focus on advanced basic materials, key strategic materials, and frontier new materials; called for exploring AI application in materials research, testing, and production.

- China's government releases list of policies to strengthen, benefit and enrich the agricultural sector during this year. said policies cover subsidies for soybean, corn planting and producing, also covers cultivated land facility protection subsidies. Policies cover subsidies for inter-provincial employment and transportation subsidies.

- Japan's Finance Minister Katayama said decided on energy subsidy as an emergency step, adds FX movements have been driven partly by speculators. Speculators can move easily due to the Bank of Japan and the summit. There has been some speculative trading in oil markets and authorities will do their utmost to respond to currency moves at any time. The ministry is prepared to take necessary actions against market volatility and is watching financial markets with an extremely high level of vigilance.

NOTABLE APAC DATA RECAP

- Australian Unemployment Rate (Feb) 4.3% vs. Exp. 4.1% (Prev. 4.1%, Low. 4.0%, High. 4.2%).

- Australian Employment Change (Feb) 48.9K vs. Exp. 20.3K (Prev. 17.8K).

Loading...