Starmer vows to stay on and fight; USTs softer as US CPI awaits - Newsquawk Daily US Market Open

- UK PM Starmer said he will not be setting out a timetable for departure. This came after over 81 Labour MPs calling for the PM to resign, enough to launch a leadership challenge.

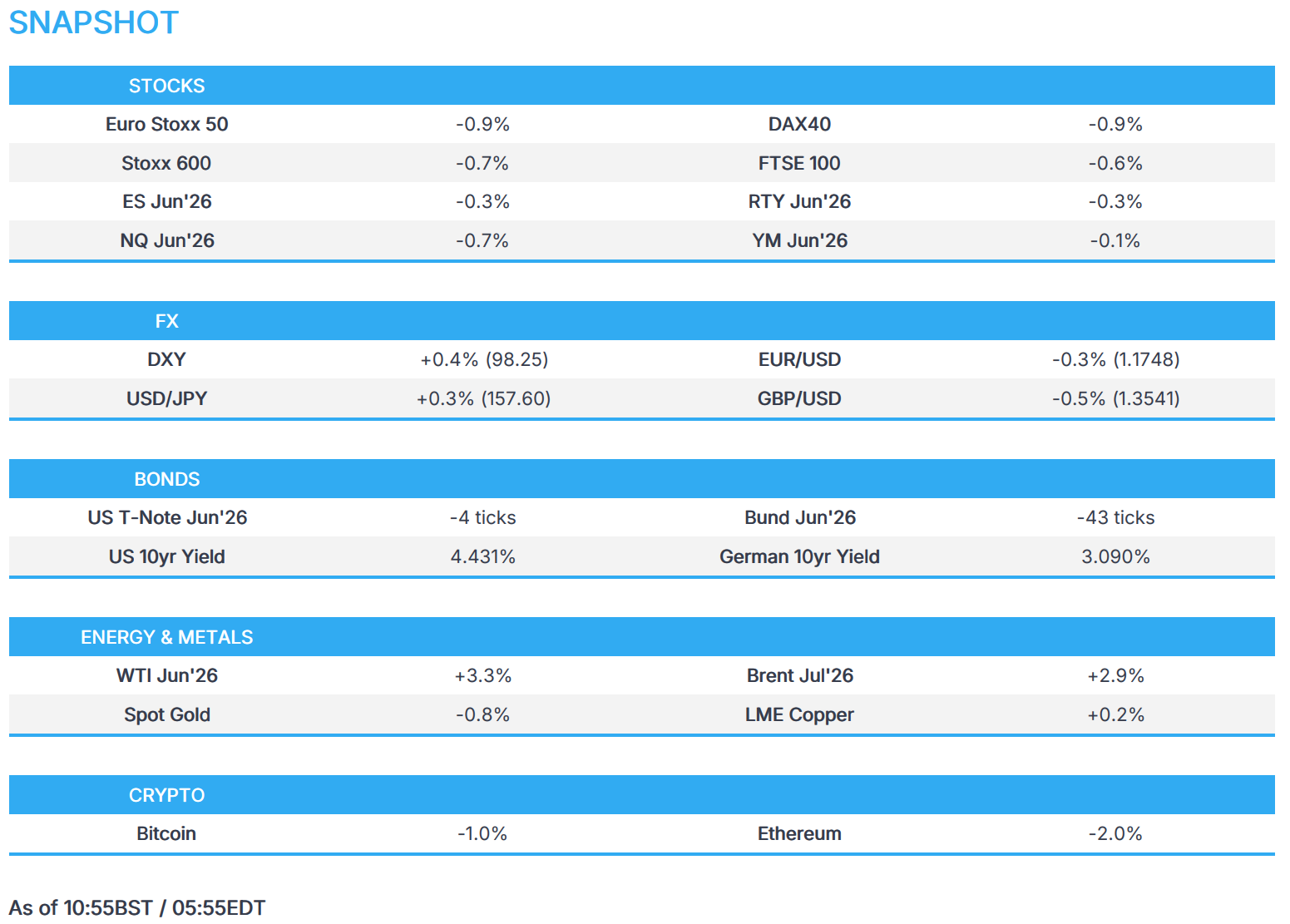

- European bourses are entirely in the red, with UK Banks hit on political turmoil; US equity futures pull back from ATHs.

- DXY is firmer, buoyed by geopols; GBP underperforms amidst political unrest, while JPY remains on intervention watch.

- Gilts underperform, USTs lower ahead of US CPI.

- Crude rises as US-Iran woes mount, with no off-ramp in sight.

- Looking ahead, highlights include US CPI (Apr), ADP Employment Change Weekly, EIA STEO (May), and EU Informal Meeting of Energy Ministers (May 12-13). Speakers include ECB’s Elderson, Fed’s Goolsbee. Supply from the US. Earnings from Under Armour.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.7%) trade with losses across the board, driven by multiple factors: 1) Iran-US war seemingly not having an end in sight, 2) UK political turmoil, and 3) mixed earnings. Overnight, US President Trump said that the ceasefire is unbelievably weak and reiterated that Iran’s proposal is unacceptable. Further reporting by Axios stated that Trump held a meeting with his national security team to discuss a way forward, which included the possible resumption of military action. This drove energy prices higher and, in turn, weighed on equities globally.

- European sectors are broadly in the red, with Energy outperforming as WTI and Brent regain the USD 100/bbl and USD 106/bbl respectively. Outside of Banks, Retail sits at the bottom of the pile.

- US equity futures (ES -0.3%, NQ -0.7%, RTY -0.3%) are under pressure, pulling back from the ATHs made in Monday’s session.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- Snapshot: DXY is firmer this morning, benefiting from continued geopolitical uncertainty. The JPY is mildly lower, but performing a bit better vs peers after an aggressive bout of strength seen in early morning trade – potentially intervention. GBP is the clear underperformer this morning, as markets eye turmoil in the Labour Party. EUR was little moved to better-than-feared ZEW sentiment metrics.

- DXY is firmer by around +0.4%, and currently at the upper end of a 97.95-98.28 range; holding just shy of its 21-DMA at 98.31. Strength today has been facilitated by ongoing geopolitical uncertainty, with President Trump suggesting the US-Iran ceasefire is “on life support”, and repeated that Iran’s proposal was unacceptable. (Detailed analysis piece on the Newsquawk feed). Domestically, focus will shift to the US CPI report this afternoon. Headline M/M is expected to rise 0.6% (prev. 0.9%); the core metrics are expected to rise modestly from the prior.

- GBP is underperforming this morning and trades at the bottom end of a 1.3502-1.3614 range. This morning has seen Cable slip below its 21-DMA (1.3542). Next level to the downside includes the round 1.3500 mark, and a dip below that level could see a test of its 100-DMA at 1.3482.

- As it stands, PM Starmer reportedly announced that he will remain as PM, adding that he will not be setting out a timetable for departure. A move which essentially invites a leadership challenge; as it stands, the only real imminent challenge would be via Wes Streeting, though Rayner is an outside possibility. This, however, could bring further division into the Labour party, as an early challenge might split Labour between Starmer, Streeting and Burnham supporters. In the near-term, we look for a formal challenge and/or more ministerial-level resignations in a bid to pressure Starmer into changing his mind.

- JPY is mildly lower, with focus on a) potential intervention and b) Bessent-Takaichi meeting. On the point of intervention, an aggressive move lower was seen in USD/JPY from around 157.71 to 156.72 (today’s range 156.72-157.75). A move which lacked a clear driver, raising speculation of further intervention. Overnight, Treasury Sec. Bessent and PM Takaichi met where the pair discussed the financial market situation, including forex, while she reaffirmed close cooperation based on the prior accord but refrained from any significant currency jawboning. Commentary post-meeting lacked any real surprises, with the USD/JPY ultimately little moved following the details of the discussions.

- Click for NY OpEx Details

FIXED INCOME

- A bearish start for fixed income as energy benchmarks climb after overnight rhetoric (see the feed for more), and with the intensifying scrutiny around UK PM Starmer weighing on Gilts and dragging peers lower as well.

- Bunds and USTs began the morning with modest losses, of a handful and around 20 ticks, respectively. While USTs haven't dipped much further, they are down to a 110-06+ low ahead of US supply and CPI. If the pressure continues, we look to 110-00+ from last week before the 109-24 contact low from March.

- Bunds saw a bout of pressure in the European morning, before the Gilt open, seemingly as the press reporting around UK PM Starmer intensified further early doors. Enough to send Bunds below the 125.00 mark.

- Gilts opened lower by 73 ticks and hit an 85.82 trough. Thereafter, UK paper trundled lower to make a contract low at 85.45 ahead of leaked comments from the PM, where Starmer reportedly announced his intention to remain as the PM. Gilts moved from 85.52 to 85.81 in the moments after his comments, as it potentially signals that Chancellor Reeves will remain at her post in the near-term. In brief, his comment essentially invites a leadership challenge; as it stands, the only real imminent challenge would be via Wes Streeting, though Rayner is an outside possibility. This, however, could bring further division into the Labour party, as an early challenge might split Labour between Starmer, Streeting and Burnham supporters. In the near-term, we look for a formal challenge and/or more ministerial-level resignations in a bid to pressure Starmer into changing his mind.

- Germany sells EUR 4.630bln vs exp. EUR 6bln 2.50% 2028 Schatz: b/c 1.4x (prev. 1.7x), average yield 2.70% (prev. 2.47%), retention 22.8%.

- UK sells GBP 4bln 4.125% 2031 Gilt: b/c 3.36x (prev. 3.33x), average yield 4.651% (prev. 4.228%), tail 0.2bps (prev. 0.3bps).

- The Netherlands sold EUR 2.745bln vs exp. EUR 2-3bln 2.75% 2036 DSL: average yield 3.209% (prev. 2.955%).

- Japan sold JPY 1.95tln 10yr JGBs, b/c 3.90x (prev. 2.57x), average yield 2.540% (prev. 2.350%).

COMMODITIES

- In geopolitics, US President Trump said he has a plan on Iran and repeated that Tehran’s proposal is unacceptable. He added that the ceasefire is unbelievably weak and “on life support”, although a diplomatic solution is still possible. Meanwhile, Axios reported Trump met with his national security team to discuss options, including possible renewed military action against Iran. US officials said Trump still wants a deal, but Iran’s refusal to make major nuclear concessions has put the military option back on the table. Two US officials said Trump is leaning toward some form of military action to increase pressure on Iran. That being said, it was also reported that US officials said Trump is unlikely to authorise military action before returning from China later this week.

- From an Iranian perspective, Iran reiterated that enrichment is not negotiable and rejected transferring enriched uranium outside the country. An Iranian parliamentary spokesperson said one option in the event of another attack could be 90% uranium enrichment.

- In reaction, WTI and Brent futures are firmer by 3.1% and 2.6% respectively, with the former towards the upper end of USD 98-101.47/bbl range and the latter just shy of session highs (USD 104.23-107.29/bbl band). Dutch TTF is firmer by some 2.5% above EUR 47/MWh.

- Spot gold is softer amid the energy-induced rise in the USD, with the bullion hovering on either side of USD 4,700/oz (in a USD 4,686-4,773/oz band) as traders look ahead to US CPI later today, alongside further headlines risk on the US-Iran front, in which a macro update will likely ultimately dictate price action.

- Base metals are mixed/mostly lower given the cautious risk sentiment and firmer USD. Copper overnight edged higher in choppy trade amid the mixed overnight risk appetite. 3M LME copper currently resides between USD 13,831.70- 13,980.38/t.

- US released another 53.3mln barrels from Strategic Petroleum Reserve to companies including Trafigura, Marathon Petroleum (MPC), and Exxon Mobil (XOM) in an effort to ease soaring fuel prices caused by the Iran war and disruptions in the Strait of Hormuz.

- US House could vote on a gas-tax holiday as early as next week, according to multiple sources familiar with the planning cited by Punchbowl.

- China has reportedly raised fuel surcharge for domestic flight from May 16th.

- Pemex reported control of the incident at the Salina Cruz refinery (330k BPD capacity).

- Indian Oil Minister said LPG production has increased.

- Indian banks resume gold and silver imports after paying a 3% tax, according to sources.

TRADE/TARIFFS

- US President Trump said need more tariffs.

- White House said US President Trump will meet with Chinese President Xi on Thursday at 10:15 AM in Beijing (03:15BST/22:15EDT) and banquet will be held at 18:00 on Thursday (11:00BST/06:00EDT). Working lunch on Friday will take place at 12:15 (05:15BST/00:15EDT).

- France presses EU to crack down on platforms like Shein and Temu, according to FT.

- US Treasury Secretary Bessent posted that he held talks with Japanese Economy Minister Akazawa; "I highlighted the continued positive collaboration between the United States and Japan on issues pertaining to critical minerals and supply chains".

UK POLITICS

- UK PM Starmer said he will not be setting out a timetable for departure. He reiterated that he takes full responsibility for the election results.

- Plenty of Cabinet Ministers spoke following the meeting with McFadden saying no one directly challenged PM Starmer during the cabinet meeting, Kendall stating Starmer has her "full support" and Kyle saying Starmer provides "steadfast leadership."

- "[UK PM] Starmer did not give his critics any chance to speak against him in this morning's meeting", Telegraph's Diver reported.

- UK PM Starmer is, according to a 'very senior minister', going to fight, ITV's Peston reported. Further reporting by Mail on Sunday's Hodges stated that UK PM Starmer "is reportedly is looking for a dignified way of ending all this. But he doesn't want to be seen to be forced out."

- Over 81 Labour MPs have now called for UK PM Starmer to resign, Politics UK reported; "This is officially enough to launch a leadership challenge if they unite behind a single candidate".

- UK Junior Minister Fahnbulleh resigns (the first Ministeral level resignation) and called on PM Starmer to set a timetable for a transition.

- UK Chief Secretary to the PM, Jones, indicates that PM Starmer could be about to announce a timetable for his resignation, according to Times' Swinford. Jones said "I'm not going to get ahead of the PM's decision."

- Four UK cabinet ministers, led by the Home Secretary, have gone into Number 10 to tell the prime minister to set out a timetable for him to resign, according to ITV News. UK Deputy PM Lammy urges PM Starmer to set out a timetable to quit.

- Four people with knowledge of conversations involving the UK Cabinet believe some ministers will move today, Politico Playbook reported. As many as six ministers could ask for the PM to outline his exit plans at the Cabinet meeting.

- "Senior Labour figures are very nervous about the market reaction this morning, hence some in the Cabinet pushing the PM to go in a way that doesn't destabilise the party", Eurasia journalist Rahman posted.

- UK Foreign Minister Cooper told UK PM Starmer he should see an orderly transition of power.

- UK Greater Manchester Mayor "Burnham's allies say a seat has been lined up for him to stand - with an announcement aimed possibly today", The Times' Kendix reported.

- Allies of UK Greater Manchester Mayor Burnham state that a timetable of a new Labour leader/PM by end-September would provide Burnham with enough time to return to the House of Commons, Sky's Rigby reported.

- UK Chancellor Reeves has pulled out of her speech at the Global Risks Summit, according to Daily Express' Spyro.

NOTABLE EUROPEAN DATA RECAP

- EU ZEW Economic Sentiment Index (May) -9.1 vs. Exp. -20 (Prev. -20.4).

- German ZEW Economic Sentiment Index (May) -10.2 vs. Exp. -20.5 (Prev. -17.2, Low. -35.0, High. -10).

- German ZEW Current Conditions (May) -77.8 vs. Exp. -77.5 (Prev. -73.7, Low. -80.0, High. -68.0).

- German Inflation Rate MoM Final (Apr) M/M 0.6% vs. Exp. 0.6% (Prev. 1.1%, Low. 0.6%, High. 0.6%).

- German Inflation Rate YoY Final (Apr) Y/Y 2.9% vs. Exp. 2.9% (Prev. 2.7%, Low. 2.9%, High. 2.9%).

- Italian Industrial Production YoY (Mar) Y/Y 1.5% (Prev. 0.5%).

- Italian Industrial Production MoM (Mar) M/M 0.7% vs. Exp. 0% (Prev. 0.1%).

- UK BRC Retail Sales Monitor YoY (Apr) Y/Y -3.4% vs. Exp. 0.8% (Prev. 3.1%).

CENTRAL BANKS

- Fed Chair nominee Warsh clears Senate procedural hurdle and a Senate confirmation vote is expected as early as Wednesday.

- BoJ Summary of Opinions from the April meeting noted a member said that given real interest rates are at a significantly low levels, it is appropriate for the BoJ to continue raising policy rates. Member said Japan’s real policy interest rate is by far at the lowest level globally, BoJ must to continue to adjust the negative real interest rate in preparation for the second-round effects of price rise.

- ECB's Nagel said ECB mandate requires to act if inflation expectations de-anchor; "we'll see in June"; baseline includes two rate hikes.

- ECB’s Patsalides said there are scenarios in which the ECB may avoid raising interest rates.

NOTABLE US HEADLINES

- US President Trump to confront Chinese President Xi at the upcoming summit over China's backing of Iran and Russia, Fox News reported. Officials said the leaders are also expected to discuss Taiwan, cybersecurity, artificial intelligence and rare earth supply chains during the summit.

GEOPOLITICS

MIDDLE EAST

- IRGC Navy official Akbarzadeh said Iran has significantly expanded its definition of the Strait of Hormuz strategic zone to include the coasts of Jask and Siri beyond the main islands, Al Mayadeen reported.

- Iran Parliament Speaker Ghalibaf said "There is no alternative but to accept the rights of the Iranian people as laid out in the 14-point proposal. Any other approach will be completely inconclusive; nothing but one failure after another."

- Iranian Parliamentary spokesperson said "One of Iran's options in the event of another attack could be 90 percent enrichment. We will review it in the parliament.".

- Deputy Foreign Minister for Legal and International Affairs of Iran Gharibabadi said US draft plan about Strait of Hormuz shows an attempt to change the face of the issue. Considered this action to be an attempt to change the face of the issue, and said that while Iran is the target of threats, pressure and attacks, some are trying to turn the consequences of a military aggression and illegal blockade into a case against Iran.

- IRGC Navy deputy said in a recent case, Iranian forces fired warning shots after an American frigate showed “provocative behaviour” in the Strait of Hormuz, prompting it to change course, Fars reported.

- Iran’s ambassador to China said Tehran views its strategic partnership with China as key to countering US pressure and advancing demands for a lasting ceasefire, IRNA reported.

- CNN White House Correspondent Treene posted "Many in Trump’s orbit want Pakistani mediators to be far more direct in their communications with the Iranians", adds "some Trump aides say that he is now more seriously considering a resumption of major combat".

- Washington was on the verge of making a decision a week ago to resume attacks on Iran, Al Hadath reported. Those close to Trump convinced him last week at the last minute to freeze the decision to return to war. Israel assesses that Khamenei is still preventing any progress in the negotiations as the Supreme Leader.

- Pakistan's ambassador to Russia is convinced that the US will not resort to a new military operation against Iran, according to TASS citing an interview.

- Israeli Navy shells Khan Yunis coast, according to Noor News, while Israel also conducts airstrikes on multiple towns in southern Lebanon, according to Al Jazeera.

- UAE has carried out military strikes on Iran, according to WSJ citing sources; UAE strikes have included attack on a refinery on Iran's Lavan Island back in early April. The strikes, which the UAE hasn’t publicly acknowledged, have included an attack on a refinery on Iran’s Lavan Island which took place in early April around the time Trump was announcing a cease-fire.

- Israeli strikes in southern Lebanon killed six and fighting continues despite April 17th ceasefire, according to AFP.

- Hezbollah said it targeted a Merkava tank in the town of Bayada with a guided missile and it was seen burning.

- Secretary General of Lebanon's Hezbollah said "We are ready to cooperate with the authorities to achieve the sovereignty of Lebanon by stopping Israeli aggression by land, sea and air", ISNA reported.

- Qatar orders ships at its LNG port to “go dark” under new safety measures.

RUSSIA-UKRAINE

- Russian Defence Ministry said Russian forces continue the Special Military Operation as the ceasefire with Ukraine expired, RIA reported.

- Ukraine's capital of Kyiv is under drone attack following expiration of the truce.

CRYPTO

- Bitcoin returned back below USD 81k, Ethereum slipped below USD 2.3k.

APAC TRADE

- APAC stocks traded mixed following the mild gains on Wall St, where the S&P 500 and NDX extended record highs, but with the upside capped by higher oil prices and geopolitical uncertainty after US President Trump said the ceasefire is unbelievably weak and is on life support, but added that a diplomatic solution with Iran is still possible. Furthermore, Trump was said to be now more seriously considering a resumption of major combat operations than he has in recent weeks, although sources also stated that a major decision on how to proceed is unlikely to be made prior to the president’s departure to China.

- ASX 200 was dragged lower as weakness in the tech, healthcare, financials and consumer sectors offset the commodity-related gains, while sentiment was also not helped by a soft NAB Business Survey.

- Nikkei 225 ultimately gained, but with price action choppy amid a softer currency, disappointing Household Spending data and hawkish undertones from the BoJ Summary of Opinions, while participants also reflected on the record earnings from SoftBank.

- Hang Seng and Shanghai Comp were mixed with the Hong Kong benchmark led higher by Kuaishou Technology after it was reported that the Co. plans to spin off its Kling AI video unit at a USD 20bln valuation, while the mainland lacks conviction as participants await the looming Trump-Xi summit in Beijing.

NOTABLE ASIA-PAC HEADLINES

- AUSTRALIAN BUDGET: Australia sees 2025/26 budget deficit at AUD 28.3bln (vs AUD 36.8bln projected); sees 2026/27 budget deficit at AUD 31.5bln, 2027/28 deficit AUD 31.0bln; Treasurer says budget helps, rather than harms, the fight against inflation.

- US Treasury Secretary Bessent said he made no request to PM Takaichi regarding monetary policy; in very close contact with Japan's finance ministry and the relationship with it is working well; both believe FX volatility is undesirable. Japan's economic fundamentals are strong and resilient, and that will be reflected in exchange rates. Expects inflation to be a short-term and transient blip. Has great confidence BoJ Governor Ueda will guide the Bank to a very successful monetary policy. PM Takaichi did not make requests about China.

- Japanese Finance Minister Katayama said had meeting with US Treasury Secretary Bessent and discussed financial market situation, including forex, while she reaffirmed close cooperation based on joint statement last year.

- Japanese Finance Minister Katayama said the Bessent-Takaichi talks were very positive, in which they discussed Mythos and critical minerals.

- Japan's Finance Ministry declines to comment on market speculation about rate checks.

- South Korean policy chief Kim said AI citizen dividend will be from excess tax and that AI dividend does not mean a windfall tax.

NOTABLE APAC DATA RECAP

- Australian NAB Business Conditions (Apr) 3 (Prev. 6).

- Australian NAB Business Confidence (Apr) -24 (Prev. -29).

- Japanese Coincident Index Prel (Mar) 116.5 (Prev. 116.3).

- Japanese Leading Economic Index Prel (Mar) 114.5 vs. Exp. 114.6 (Prev. 113.3).

- Japanese Foreign Exchange Reserves (Apr) 1383.0B (Prev. 1374.7B).

Loading...