Stocks and crude a touch firmer, TSMC beats, raises FY guide - Newsquawk US Market Open

- The Trump administration's goal is to bring both sides to the brink of an overarching deal to end the conflict that can then be pushed over the finish line in a second face-to-face meeting.

- A military advisor to the Islamic Revolution Leader says Iranian Armed Forces’ launchers are ready to hit American warships and sink all of them, Press TV reported.

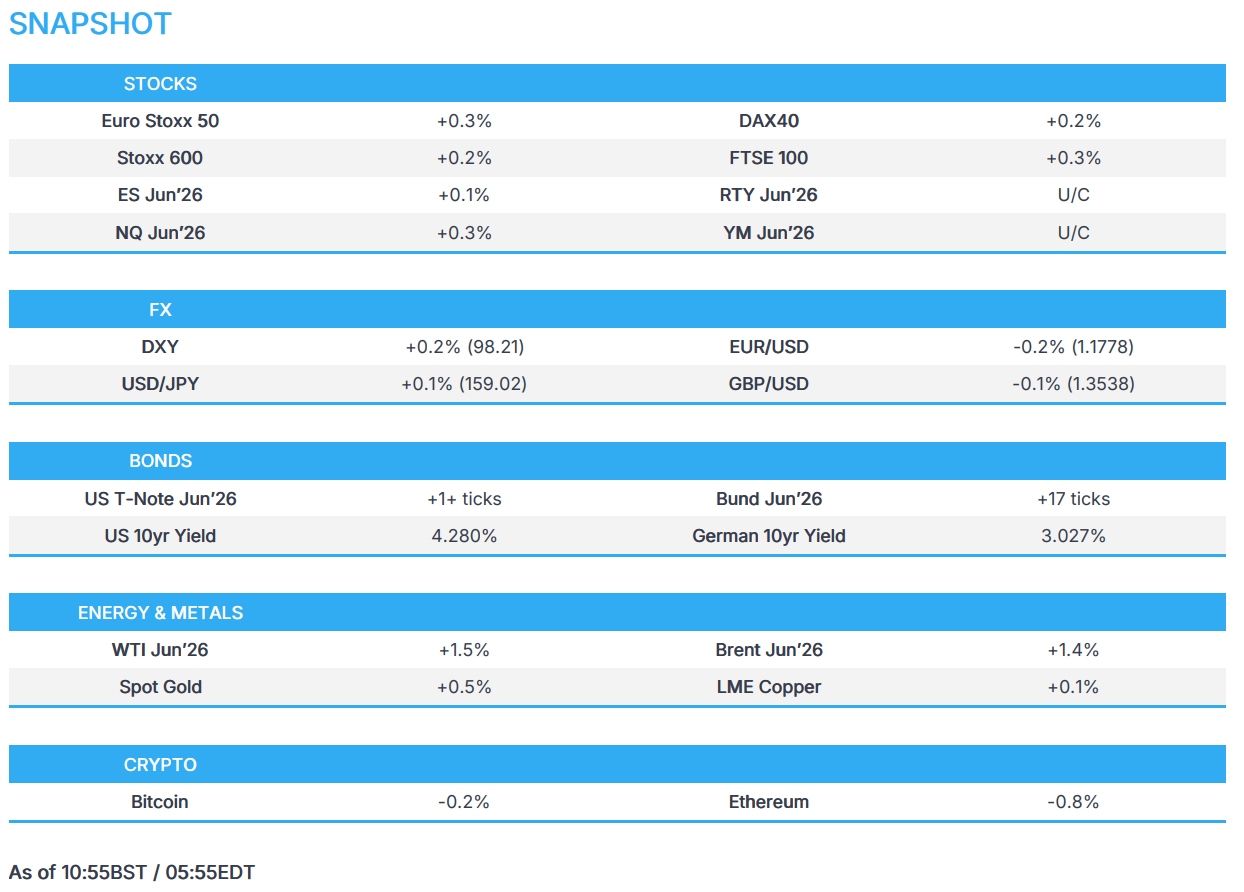

- European bourses printing mild gains, TSMC earnings lift the tech sector; US equity futures muted just shy of ATHs.

- DXY cautiously firms, JPY pares verbal intervention strength while GBP unreactive despite upside GDP surprise.

- Global benchmarks initially firmer, but hit as the risk tone deteriorated.

- Crude tilts higher as markets still await confirmation of any talks/ceasefire.

- Looking ahead, highlights include US Jobless Claims (Apr/11), Philly Fed Index (Apr), Industrial/Manufacturing Production (Mar), New Zealand Food Inflation (Mar), ECB Minutes (Mar). Speakers include Fed’s Williams & Miran, ECB’s Schnabel, Nagel & Lane, RBA’s Hunter & BoE’s Taylor. Earnings from Abbott, Charles Schwab, PepsiCo & Netflix.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- The Trump admin's goal is to bring both sides to the brink of an overarching deal to end the conflict that can then be pushed over the finish line in a second face-to-face meeting, according to ABC, citing officials. The officials acknowledge that technical talks to hammer out the fine details and implementation of the arrangement will likely take longer to complete, perhaps eventually necessitating an extension of the initial ceasefire, but that pushing back the truce’s expiration date isn’t a top priority for the administration at the moment.

- US President Trump told guests Monday night he wants to bring the war in Iran to a swift end; said only way to get Iran back to negotiating table was to increase the pressure, according to WSJ citing officials at the dinner.

- US President Trump posted "Trying to get a little breathing room between Israel and Lebanon. It has been a long time since the two leaders have spoken, like 34 years. It will happen tomorrow. Nice!".

- Pakistani Army Chief is heading to the US on Friday as part of mediation efforts between the US and Iran, Al Jazeera reported citing a Pakistani security source.

- Pakistan’s Foreign Ministry said the US and Iran are willing to hold talks and the process is continuing but no date decided for next round of US-Iran talks.

- A military advisor to the Islamic Revolution Leader said Iranian Armed Forces’ launchers are ready to hit American warships and sink all of them, Press TV reported.

- A senior Iranian official said the fate of Iran’s highly enriched uranium and the duration of its nuclear restrictions remain unresolved, adding that fundamental disagreements persist over nuclear issues. Iranian official said there are greater hopes for extending the ceasefire and holding a second round of talks after the trip, adding that the Pakistani army chief’s visit to Iran helped reduce differences in some areas.

- Iranian officials will meet with Pakistan's army chief on Thursday in Tehran and will discuss US proposals, according to TASS.

- Iran and the Pakistani mediator will discuss details of the messages exchanged between Tehran and Washington tomorrow, Thursday; via Al Jazeera citing Iranian TV.

- Journalist Abas Aslani posted source said Iran-US talks are far less positive [than reported] due to contradictory US stances & Israeli spoiler efforts, media push hyping success of talks is a PR manoeuvre to calm markets and shield Trump from pressure.

- Iran’s ambassador to Pakistan said Islamabad is the sole venue for Iran–US talks.

- Diplomatic sources suggest that "Washington is pressing forcefully to cool down the Lebanese front", via Kan's Kais; "Second round of negotiations between Israel and Lebanon will take place in Washington soon". "Second round of negotiations between Israel and Lebanon will take place in Washington soon, and that the current contacts are focused on achieving a temporary ceasefire that will lay the groundwork for ending the war."

- Two Israeli officials said the meeting of the political security cabinet ended without a decision on a ceasefire in Lebanon, according to Axios's Ravid.

- Israeli media citing informed sources state that a ceasefire in Lebanon will not happen soon despite Trump's statements.

- Israeli army has not received any instructions so far to prepare for a ceasefire in Lebanon, via Al Arabiya citing local reported.

- Lebanese officials say a ceasefire between Israel and Lebanon is expected 'soon', according to FT.

- The next meeting between Israel and Lebanon is expected to be held early next week, via Sky news Arabia citing Israel Hayom.

- Iran's Interior Minister has ordered border governors to neutralise the threat of a naval blockade by strengthening and developing border trade by increasing imports of basic goods and exports of goods, utilising all national and regional capacities.

- Iranian politician affiliated with Resistance Front of Islamic Iran, Mohsen Rezaei said they will not leave the Strait of Hormuz until the full realisation of Iran's rights, adds that this time, Iran has set preconditions.

- Iranian Parliament Speaker Ghalifbaf said US should withdraw from 'Israel first' mistake and must comply with agreement, also said resistance and Iran are one soul both in war and ceasefire.

- Hezbollah fires long-range missiles at Tel Aviv, according to Defapress.

- Iranian military affiliated outlet Defapress claims that four ships broke the US naval blockade over the past 24 hours, citing satellite data.

- Israeli warplanes carried out a strike on the town of Shihabiya in southern Lebanon.

- US Central Command said US blockade has turned back 10 vessels in the Strait of Hormuz today.

- China's Foreign Minister Wang Yi stressed to Iran that the Strait of Hormuz needs to reopen and stressed freedom of navigation in Hormuz, while he said Hormuz reopening is a unanimous call from the international community.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.2%) are broadly gaining, albeit only modestly. The CAC 40 is the outperformer, rebounding from Wednesday’s luxury-driven selloff. The FTSE 100 is also slightly higher this morning, after UK GDP came in far stronger than expected in February (0.5% vs exp. 0.1%).

- Sectors point to a positive bias. Top of the pile lies Technology, supported by strong TSMC earnings, which has lifted peers such ASML. Telecoms is the underperformer, with a downgrade for Telia weighing on the broader sector.

- US equity futures are trading muted, with the NQ outperforming as TSMC lifts the index. ES futures is currently trading just shy of the ATH at 7,093.75 and could break ATHs in today’s cash session.

- TSMC (TSM/2330 TT) reported Q1 net income that beat estimates with revenue and operating profit that grew 35% and 61% respectively on an annual basis. In terms of guidance, its Q2 revenue metric beat analyst expectations while FY26 revenue was raised to above 30% (from “close” to 30%).

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY edged higher throughout the entirety of the European session following punchy Iran rhetoric. The index marked a session high of 98.21, rising from its earlier trough of 97.83 made in Asia. (Full Middle East analysis on the headline feed) As it stands, both US and Iran continue communication, but there is no confirmation yet on second-round talks or a ceasefire extension - not to mention Lebanon, which remains a key point. Aside from geopolitics, POLITICO reported this morning, "a growing chorus of Republicans, eager to install Warsh, are joining the call for the administration to end the probe" into Fed Chair Powell. This comes ahead of Warsh's hearing next week. The session ahead sees remarks from Fed’s Williams (voter), who will speak at a Federal Home Loan Bank of New York event, while Miran (voter, dovish dissenter) will speak on the global outlook.

- GBP knee-jerked higher on a stronger-than-expected UK GDP report from February, but now trades with very mild losses given the Dollar strength this morning. In brief, on a monthly basis, GDP rose 0.5%, while yearly saw an increase of 0.1%. This set of metrics did not encapsulate the US-Iran war and as such, MPC members will likely refer to the second-round effects of the energy shock before opting to adjust rates. Cable continues to trade towards recent highs and is essentially at pre-war levels. The pair attempted to breach 1.36, a rally which faltered at 1.3594.

- Antipodeans trade mixed. While Aussie is a touch firmer against a resilient USD following jobs data - Kiwi sits at the bottom of the pile as bets for RBNZ tightening pare a touch with markets implying 77bps of easing by year end (prev. c. 83bps). NZD/USD began falling in Asia, though losses extended throughout the European morning to trade at session lows of 0.5893, the move likely to face support @ 0.5892.

- JPY had a choppy overnight session with USD/JPY marking a session low of 158.27 after successful jawboning from Finance Minister Katayama; she told G7 members that Japan was watching FX with a high sense of urgency. She also reiterated close communication with the US Treasury. This, as is typically the case with the Japanese Finance Ministry, indicates officials are uncomfortable with the extent of JPY weakness, with JPY nearing the key 160 mark. Since these comments, JPY pared the entirety of the strength Katayama gave to the haven, pressured by the gains in the USD.

FIXED INCOME

- Global fixed benchmarks opened the European session with a positive bias, but have gradually edged off best levels as the risk tone deteriorated as the morning progressed. Initial optimism was facilitated by comments from both Israeli and Lebanese officials, who said that a ceasefire is expected soon, and talks are expected to continue in the near-term. On the Iranian front, President Trump said that “he wants to bring the war in Iran to a swift end”. Thereafter, in early morning trade, a military advisor to the Islamic Revolution Leader said Iranian Armed Forces’ launchers are ready to hit American warships and sink all of them – a comment which weighed on the risk tone at the time, leading to upside in the crude complex, which pressured global fixed paper.

- USTs are firmer by a couple of ticks and currently trades at the lower end of a 111-11 to 111-17 range. Ultimately, moving at the whim of geopolitical developments, with markets now awaiting clear details on when/if the second round of Iran-US talks will begin. From a domestic perspective, weekly initial jobless claims (215k expected from 219k) and continuing claims (exp. 1.84mln from 1.794mln), NY Fed services activity, Philly Fed manufacturing are all due.

- Bunds are firmer by around 15 ticks and currently trade within a 125.32 to 125.62 range. German paper, as above, is off its best levels as the risk tone slipped a bit. Domestic newsflow has been fairly limited this morning, aside from an updated Goldman Sachs call for the ECB; analysts now expect the ECB to deliver 25bps rate hikes in June and September 2026 (prev. saw April and June), citing expectations that energy prices will stay high through 2026, feed through materially into inflation in the coming months and keep ECB communication largely hawkish. As it stands, money markets fully price in a 25bps hike in July. Focus later will be on the ECB Minutes (Mar), where the Bank kept rates steady – traders will be cognizant of any commentary pertaining to the Middle East situation.

- Gilts are incrementally lower and trade within an 88.68 to 89.07 range. Slightly underperforming vs peers, given the hawkish impulses from a stronger-than-expected UK GDP report. In brief, on a monthly basis, GDP rose 0.5%, while yearly saw an increase of 0.1%. ING writes "UK output surged in February, but it's in line with a trend dating back to 2022, where growth is stronger in the first quarter than across the rest of the year. We're taking this latest data with a pinch of salt".

- UK sells GBP 900mln 1.875% 2049 I/L Treasury Gilt: b/c 3.20x (prev. 3.39x), real yield 2.165% (prev. 2.36%).

- France sells EUR 12.994bln vs exp. EUR 11-13.0bln 2.40% 2029, 2.70% 2031, 0.00% 2032 and 3.00% 2033 OAT.

- Spain sold EUR 5.653bln vs exp. EUR 5-6.0bln 3.10% 2031, 3.00% 2033 and 3.50% 2041 Bono.

COMMODITIES

- Regional mediators are actively working to extend the US-Iran ceasefire and secure a second round of talks, with both sides agreeing in principle to reconvene, though no date or venue has been set. The Trump administration is pushing a two-stage strategy: use sustained economic and military pressure to force Iran toward the brink of a broader deal, then finalise it in a follow-up face-to-face meeting, with technical negotiations on implementation likely to extend beyond the current truce. A senior Iranian official said the fate of Iran’s highly enriched uranium and the duration of its nuclear restrictions remain unresolved, adding that fundamental disagreements persist over nuclear issues.

- Pakistan has taken a central mediation role, coordinating messages between Tehran and Washington and engaging both politically and militarily, although officials confirm no timeline has been agreed for the next round. Despite publicly downplaying the need for a ceasefire extension, US officials acknowledge it may ultimately be required to keep negotiations alive as talks progress.

- Crude prices edged higher following yesterday’s losses as traders feel the ceasefire could be prolonged and negotiations restarted. Brent Jun holds above USD 95/bbl this European morning (in a USD 94.43-96.85/bbl range) while WTI Jun sits in a 87.32-89.82/bbl parameter.

- Spot gold trades modestly higher, just above USD 4,800/oz and well within yesterday’s USD 4,786-4,871/oz range. Base metals are flat/positive with 3M LME copper holding above USD 13k/t in a current USD 13,281.00-13,376.58/t range. Overnight data showed China’s Q1 growth accelerated on strong exports (Y/Y printed at the top end of China’s 2026 target of 4.5-5%), while March retail sales rose but slowed from February; analysts said the Iran war still poses risks to the outlook.

- Australia said it secures 100mln litres extra of diesel from Brunei and South Korea.

- Repsol (REP SM) is set to take back operational control of its Venezuelan oil assets and boost production following an agreement with the country’s government, according to FT.

- White House is expected to urge heads of oil and gas companies to increase drilling, according to POLITICO.

- Australia's Energy Minister reported that a fire at Viva Energy's (VEA AT) refinery is still not under control, while diesel and jet fuel output continues, but refinery fire may hit petrol production more.

TRADE/TARIFFS

- UK Europe Minister Nick Thomas-Symonds is expected to offer an update on the state of play in negotiations; EU Trade Chief Sefcovic, and European Parliament President Roberta Metsola, will also provide keynotes, reported Politico.

- USTR Greer said US-China Board of Investment is to be a government forum, adds there's no situation where there's no trade between US and China, also said the Trump admin wants to be pragmatic regarding China.

NOTABLE EUROPEAN DATA RECAP

- EU Inflation Rate MoM Final (Mar) M/M 1.3% vs. Exp. 1.2% (Prev. 0.6%, Low. 1.2%, High. 1.2%).

- EU Inflation Rate YoY Final (Mar) Y/Y 2.6% vs. Exp. 2.5% (Prev. 1.9%, Low. 2.5%, High. 2.6%).

- EU Core Inflation Rate YoY Final (Mar) Y/Y 2.3% vs. Exp. 2.3% (Prev. 2.4%).

- UK Balance of Trade (Feb) -0.720B vs. Exp. -3.6B (Prev. 3.922B).

- UK Goods Trade Balance (Feb) -18.79B vs. Exp. -20.2B (Prev. -14.45B, Low. -20.5B, High. -14B).

- UK GDP YoY (Feb) Y/Y 1.0% vs. Exp. 1.0% (Prev. 0.8%).

- UK GDP MoM (Feb) M/M 0.5% vs. Exp. 0.1% (Prev. 0%, Low. 0.0%, High. 0.3%).

- UK GDP 3-Month Avg (Feb) 0.5% vs. Exp. 0.2% (Prev. 0.2%, Low. 0.2%, High. 0.3%).

- UK Industrial Production MoM (Feb) M/M 0.5% vs. Exp. 0.3% (Prev. -0.1%).

- UK Industrial Production YoY (Feb) Y/Y -0.4% vs. Exp. -0.9% (Prev. 0.4%).

- UK Manufacturing Production YoY (Feb) Y/Y -0.5% (Prev. 1.3%, Low. -0.4%, High. 0.1%).

- UK Manufacturing Production MoM (Feb) M/M -0.1% (Prev. 0.1%, Low. 0.0%, High. 0.7%).

- UK Construction Output YoY (Feb) Y/Y -1.0% vs. Exp. -0.4% (Prev. -0.2%).

- Italian Inflation Rate MoM Final (Mar) M/M 0.5% vs. Exp. 0.5% (Prev. 0.7%).

- Italian Inflation Rate YoY Final (Mar) Y/Y 1.7% vs. Exp. 1.7% (Prev. 1.5%).

CENTRAL BANKS

- ECB officials are said to be leaning towards an April rate hold.

- ECB's Schnabel said that the memory of high inflation remains fresh, and inflation expectations could be more fragile. Can afford to take time to analyse the Iran shock. We are in a relatively favourable position because we were successful in bringing down inflation to 2% before the war started, have monetary policy stance that is broadly neutral. To carefully consider data that may indicate inflation becoming entrenched or having second-round effects.

- ECB’s Demarco said policymakers must be patient on rate decisions, but warns an adverse scenario could materialise; adverse scenario could require two rate hikes; longer-term inflation expectations anchored.

- ECB's Muller said rate move at April meeting still cannot be ruled out, adds may not have all the data this month to determine if interest rates will have to be raised to tame an inflation surge and June meeting will offer greater body of information. No hard evidence of second-round effects of inflation.

- Goldman Sachs expects the ECB to deliver 25bp rate hikes in June and September 2026 (prev. saw hikes in April and June). Analysts expect energy prices to remain persistently high through 2026, significant pass-through into inflation is likely in coming months and ECB’s communication has remained largely hawkish on the path ahead.

NOTABLE US HEADLINES

- US Pentagon approaches automakers and other US manufacturers as the Trump admin want them to play a larger role in weapons production, according to WSJ.

GEOPOLITICS

RUSSIA-UKRAINE

- Ukrainian President Zelensky posted "there can be no normalization of Russia as it is today. Pressure on Russia must work", following heavy drone attacks, via X.

- Explosions reported in Ukraine's capital, Kyiv, while the Mayor said air defence systems have been activated.

CRYPTO

- Bitcoin consolidates below USD 75k, Ethereum pulls back from USD 2.4k.

APAC TRADE

- APAC stocks mostly gained following the positive lead from Wall Street, where the S&P 500 and Nasdaq printed fresh all-time highs, amid tech strength and peace talk optimism.

- ASX 200 bucked the trend and gave back initial gains, and more, as notable outperformance in tech was offset by losses in energy, resources, materials, financials and miners.

- Nikkei 225 rallied to a fresh record high after reclaiming the 59,000 status amid the hopes for a Middle East resolution and with the index led by the momentum in tech stocks.

- Hang Seng and Shanghai Comp were higher with further upside seen as the dust settled following the mixed Chinese GDP and activity data, in which GDP growth for Q1 missed expectations, but GDP Y/Y topped forecasts and printed at the high-end of China's official 2026 GDP growth target. Meanwhile, Industrial Production data for March was better-than-expected, but Retail Sales disappointed.

NOTABLE ASIA-PAC HEADLINES

- Japan's top FX diplomat Mimura said told US Treasury Secretary Bessent will upgrade FX developments as needed, and both sides agreed to coordinate closely on FX.

- Japanese Finance Minister Katayama said regarding exchange rates, agreed to further intensify communication with US Treasury Secretary Bessent.

- Japanese Finance Minister Katayama said many central bankers are adopting a wait-and-see stance, as raising interest rates could have a negative impact on the economy, adds it is impossible to predict when the current situation ends and spillover effects.

- Senior Japanese Financial Regulator official said Japan sees private credit as potential pillar in new strategy to meet corporate funding demand driven by M&A surge, according to reported.

- China NBS said the economy had a good start in Q1, but the external situation is becoming more complex, adds China is to expand domestic demand and optimise supply. China will implement proactive macro policies. Expects a complex, volatile external environment. China will consolidate economic recovery foundation. Sees mixed signs of strong supply and weak demand.

- Deutsche Bank upgrades China's 2026 real GDP growth to 4.9% (prev. 4.5%).

- Barclays raises China 2026 GDP growth view to 4.6% (prev. saw 4.0%).

NOTABLE APAC DATA RECAP

- Chinese GDP Growth Rate YoY (Q1) Y/Y 5.0% vs. Exp. 4.8% (Prev. 4.5%, Low. 4.0%, High. 5.7%).

- Chinese GDP Growth Rate QoQ (Q1) Q/Q 1.3% vs. Exp. 1.4% (Prev. 1.2%, Low. 0.9%, High. 1.8%).

- Chinese Industrial Production YoY (Mar) Y/Y 5.7% vs. Exp. 5.6% (Prev. 6.3%, Low. 4.5%, High. 7.0%).

- Chinese Unemployment Rate (March) 5.4% vs. Exp. 5.2% (Prev. 5.3%).

- Chinese Retail Sales YoY (Mar) Y/Y 1.7% vs. Exp. 2.3% (Prev. 2.8%, Low. 0.8%, High. 3.3%).

- Chinese House Price Index MoM (Mar) M/M -0.2% (Prev. -0.3%).

- Chinese House Price Index YoY (Mar) Y/Y -3.4% (Prev. -3.2%).

- Chinese Industrial Capacity Utilization (Q1) 73.6% (Prev. 74.9%).

- Chinese Fixed Asset Investment (YTD) YoY (Mar) Y/Y 1.7% vs. Exp. 1.8% (Prev. 1.8%).

- Australian Employment Change (Mar) 17.9K vs. Exp. 20K (Prev. 48.9K).

- Australian Unemployment Rate (Mar) 4.3% vs. Exp. 4.3% (Prev. 4.3%).

- Australian Full Time Employment Chg (Mar) 52.5K (Prev. -30.5K).

- Australian Part Time Employment Chg (Mar) -34.6K (Prev. 79.4K).

- Australian Participation Rate (Mar) 66.8% (Prev. 66.9%).

- Australian Consumer Inflation Expectations (Apr) 5.9% (Prev. 5.2%).

Loading...