Stocks bid as crude slides; GBP unreactive to calls for PM to resign - Newsquawk US Market Open

- Israel and Lebanon 10-day ceasefire took effect from 17:00EDT on Thursday. Despite this, reports indicate that Israel bombed several villages in southern Lebanon after announcing the ceasefire agreement.

- US President Trump said the Iran war is going swimmingly and should be ending pretty soon, added going to see some incredible results.

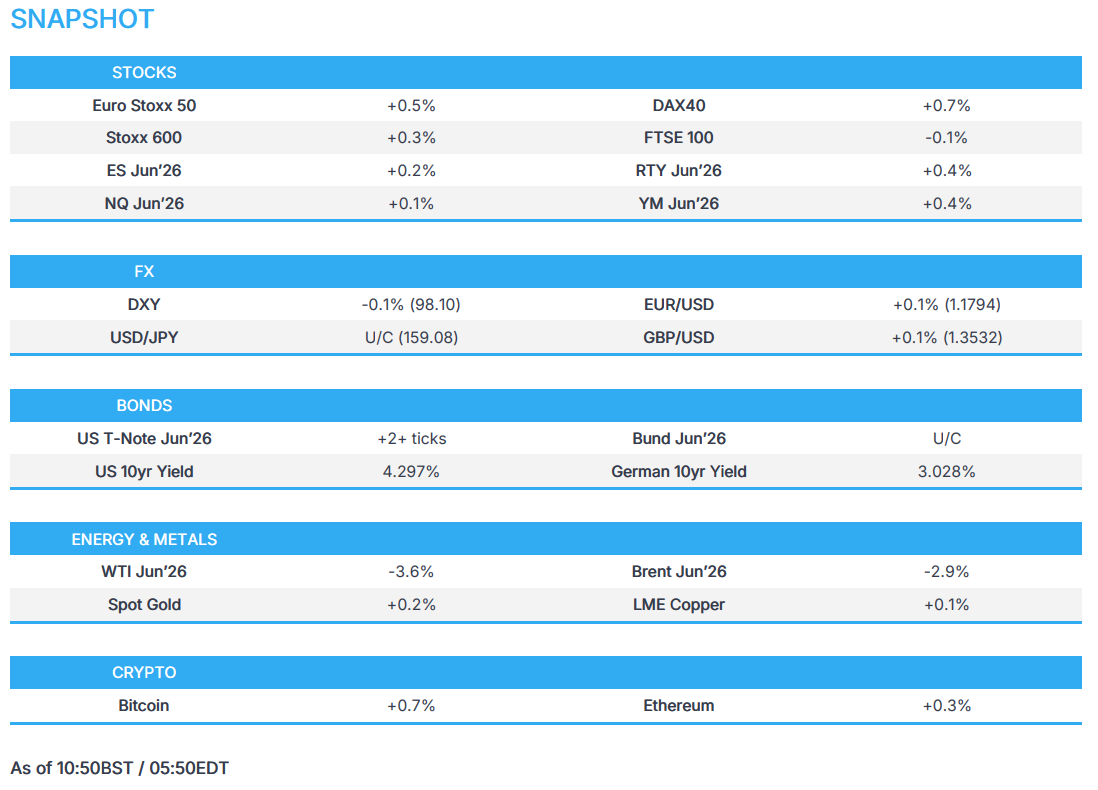

- European bourses mixed; US equity futures remain near ATHs, NFLX slips after maintaining guidance and co-founder stepping down.

- DXY slightly softer, G10s mixed, GBP unreactive on UK politics.

- Global fixed benchmarks broadly unchanged awaiting Fed speak.

- Crude pressured despite light newsflow, Israel/Lebanon ceasefire shows fragility.

- Looking ahead, highlights include Canadian Housing Starts (Mar). Speakers include BoE's Pill, Fed’s Daly, Barkin & Waller. Earnings from State Street. Credit Reviews include Morningstar DBRS reviews credit rating on the EU and Italy.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.3%) are broadly gaining on the last day of the trading week. The FTSE MIB is the slight outperformer, while the FTSE 100 lags as miners underperform.

- European sectors are mixed. Media tops the sector pile, closely followed by Technology while Basic Resources resides at the bottom of the pile.

- US equity futures continue to gain, hovering around ATHs. Despite the positiveness, Netflix shares have slumped (-10.1% pre-market) as analysts were left disappointed after the co. reiterated its FY guidance despite beating its Q1 top-line metrics; focus also on its co-founder to step down.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is a touch lower on the day with crude benchmarks trading lower by around -3% as news emerged that a Pakistani-flagged tanker became the first crude carrier to surpass the US Blockade since Monday. Elsewhere on geopolitics, reports suggested Indian refiners are paying for Iranian crude in CNY, reporting which may have added to pressure in the USD. (Comprehensive geopolitical analysis on the headline feed)

- DXY trades a touch above the 98.00 level, which it has tested in recent days, while USD/JPY reversed from a high of 159.53 to move towards the 159.00 mark. On the latter, BoJ Governor Ueda was on the wires overnight, he reiterated that monetary conditions remain highly accommodative.

- Elsewhere, AUD mildly leads given its high-beta characteristics with gold also firmer, and the aforementioned reports that CNY was used to pay for Iranian crude. AUD/USD lifted from a 0.7154 base to mark a session high of 0.7182

- Sterling resilient to the political risks that emerged on Thursday afternoon. The UK PM is now facing calls to resign after news that Mandelson failed his vetting process for the Foreign Office. Some MPs have been calling for Starmer to resign: “I fail to see how Starmer survives this.”, one told the iPaper. Though close aides, like Chief Secretary Darren Jones, said the PM won't resign and didn't mislead Parliament. Starmer himself has denied any knowledge of the failed vetting. Given these reasons and the fact that PM has repeatedly said he wishes to see out his term with cabinet ministers recently voicing support for him, Gilts and Sterling, which initially weakened on the news, pared their respective losses.

FIXED INCOME

- Global fixed benchmarks are mixed/flat, but have held an upward bias throughout the European session, with the crude complex residing towards lows. Focus remains on the geopolitical front, with Lebanon-Israel having agreed to a ceasefire (but there have been reports of flare-ups in the south of Lebanon), whilst the US-Iran have yet to agree on a second round of talks. Nonetheless, President Trump continues to remain positive, suggesting that “they are making a lot of progress on Iran, and he is not sure the ceasefire needs to be extended”.

- USTs are currently trading firmer by a couple of ticks and toward the upper end of a 111-04 to 111-09+ range. Aside from lower energy prices, US paper has not had much to digest, and this has been reflected in the fairly lacklustre price action. The US data docket is lacking, so more focus will be on Fed speak via Daly, Barkin and Waller later today.

- Bunds are flat, but have been moving higher throughout the European morning, alongside the pressure seen in the crude complex. Currently trading at the upper end of a 125.11 to 125.46 range. Earlier, there was some commentary from ECB’s Muller, who struck a familiar hawkish tone, noting that an April hike cannot be excluded; comments which add on to the hawkish tone struck by other ECB members and the Minutes released on Thursday.

- Gilts are firmer by around 10 ticks, where UK paper reacted to domestic politics. In brief, reports on Thursday suggested that Mandelson failed his vetting process for the Foreign Office – this has led to the Top Foreign Official to leave his role. This renewed some pressure for the PM to leave his position, but Chief Secretary Darren Jones, said the PM won't resign – he struck a familiar line, where he suggested that Starmer had no knowledge of the failed vetting process. At least in the near term, the pressure on Starmer appears to be limited in nature, though MUFG highlights that the Labour Party could run into issues surrounding the local elections in early May. UK paper currently trades within a 87.83 to 88.38 range.

COMMODITIES

- In geopolitics, a 10-day Israel-Lebanon ceasefire took effect at 17:00EDT/22:00BST on Thursday, though Israeli PM Netanyahu rejected Hezbollah’s demand for a full Israeli withdrawal from southern Lebanon, saying forces would remain in a security zone extending to the Syrian border. A Hezbollah source said Lebanon retains the right to resist by all means while Israeli forces remain, while Iran welcomed the ceasefire but also called for a full withdrawal. This morning, reports made the rounds that Israeli forces targeted an ambulance team in southern Lebanon (which breaches the ceasefire), although reporting on this was light overall. On Iran, President Trump struck an optimistic tone on prospects for a permanent US-Iran ceasefire and said Tehran had agreed to reopen the Strait of Hormuz, though some European and Gulf Arab leaders cautioned a deal could still take around six months; Trump nevertheless said an announcement could come soon. Meanwhile, a source told Al-Mayadeen that starting Friday at noon (10:00 BST), anyone wishing to cross Bab al-Mandab should be more vigilant than ever before in all six directions, while other reports said the warning was made by a resistance commander.

- Crude price action has been choppy this morning, prices fell on hopes of reduced Middle East supply disruption, with Brent Jun'26 moving towards USD 98/bbl (USD 96.15-98.98/bbl range) and WTI Jun'26 sub-90/bbl (in a USD 87.46-90.34/bbl range), before recovering slightly on the Lebanon ambulance report. New lows were hit shortly after wires re-ran overnight reports of a Pakistani-flagged tanker exiting the Persian Gulf, whilst other reports suggested Indian refiners are paying for Iranian crude in CNY. Do note the low for today is a moving target, at the time of writing.

- Spot gold trades within a narrow range, awaiting the next macro impulse. Ranges are narrow within USD 4,768-4,806/oz. Spot silver found some support near its 100 DMA (USD 77.95/oz) but remains contained to a USD 77.77-79.26/oz.

- Base metals flat/mixed with copper futures contained within a narrow band amid a lack of macro headlines ahead of a weekend of risk. 3M LME copper resides in a USD 13,182.53-13,300.60/t range at the time of writing.

- Indian refiners are reportedly settling rare cargoes of Iranian oil purchased under a temporary US sanctions waiver using CNY through ICICI Bank.

- Cumulative crude and condensate supply losses in the Middle East have reached 521mln barrels, according to Kpler's Baker.

- South Korean officials say that a South Korean tanker, carrying crude oil, has passed through the Red Sea route from Saudi's Yanbu port, AP reported.

- IEA chief said markets must brace for significant price surges if critical oil transit route remains closed, while IEA signals it's not ready yet to release more reserves, though the option is being evaluated.

- Shanghai weekly copper inventories: 240.5k (prev. 266.5k).

- Commerzbank sees silver prices at USD 90/oz by the end of 2026.

NOTABLE EUROPEAN HEADLINES

- UK PM Starmer's Chief Secretary Darren Jones said PM won't resign and didn't mislead Parliament, via BBC. The PM has not knowingly or unknowingly misled Parliament. He also stated that PM Starmer is furious; does not think it brings his future into question.

- Senior UK Minister said PM Starmer has not considered resigning amidst called for resignation following Mandelson scandal, according to BBC.

- UK Foreign Office senior official Sir Olly Robbins is leaving his post following the Mandelson vetting row, according to The Guardian's Political Editor Crerar.

- UK PM Starmer faces resignation called over Mandelson vetting, according to The Telegraph.

- EU is planning its biggest relaxation of corporate merger rules in decades, while EU competition commissioner Ribera said merger rules are to favour scale and innovation, according to FT.

NOTABLE EUROPEAN DATA RECAP

- EU Balance of Trade (Feb) 11.5B vs. Exp. 11.1B (Prev. -1.9B)

- EU Current Account (Feb) 21.09B (Prev. 13B).

- Italian Balance of Trade (Feb) 4.944B vs. Exp. 3.83B (Prev. 1.089B).

- Italian Current Account (Feb) 3654M (Prev. -1785M).

CENTRAL BANKS

- BoJ Governor Ueda said G20 discussed impacts of Middle East on prices and on the global economy, adds many said the Middle East is an important factor and remains uncertain. Supply shock-driven inflation is harder to tackle than demand-driven. Rising oil prices put upward pressure on underlying inflation, but worsen Japan's terms of trade and weigh on the economy. Monetary conditions remain highly accommodative and Japan's real interest rate is low. BoJ will decide policy based on likelihood of forecast materialising and risk at each meeting.

- ECB's Muller said market's rate bets are not completely unreasonable, its hard to argue there is an obvious case for an April hike; can not fully exclude it. Dangerous to assume energy shocks are temporary. ECB is better placed than it was in 2022 - does not have to wait to see second-round effects.

- BoE's Breeden says the Middle East conflict raises the risk of correlated shocks across markets. On repo markets, would authorise considering reforms to gilt repo markets to improve resilience.

- Danske Bank sees two rates hikes by the Riksbank by August.

NOTABLE US HEADLINES

- The US Congressional Progressive Caucus discussed trying to force repeated House votes on Iran war powers resolutions, Punchbowl reports.

- US House plans overnight FISA vote, according to POLITICO.

- US President Trump posted "Sadly, Mayor Mamdani is DESTROYING New York! It has no chance! The United States of America should not contribute to its failure. It will only get WORSE. The TAX, TAX, TAX Policies are SO WRONG. People are fleeing".

GEOPOLITICS

MIDDLE EAST

- IRNA states that security and traffic measures have been intensified in Islamabad, preparing itself for a major international event, while highlighting that Pakistani officials have not yet confirmed or denied any negotiations, Iran International reported.

- US President Trump said Iran war is going swimmingly and should be ending pretty soon, adds going to see some incredible results.

- Israel and Lebanon 10-day ceasefire takes effect.

- US President Trump posted "I hope Hezbollah acts nicely and well during this important period of time. It will be an GREAT moment for them if they do. No more killing. Must finally have PEACE!".

- Israel reportedly launched airstrikes on southern Lebanon minutes before the ceasefire, according to an Asharq correspondent.

- Iran stresses the need for full Israeli withdrawal from southern Lebanon, according to Iranian media citing a Foreign Ministry spokesman.

- Iran welcomes ceasefire in Lebanon, said was part of Iran-US ceasefire understanding mediated by Pakistan, Iranian media reported.

- Lebanon's Army noted intermittent shelling on southern Lebanese villages after the ceasefire took effect.

- ISNA noted that the Lebanese army announced that the Israeli regime bombed several villages in southern Lebanon after announcing the ceasefire agreement.

- "Israeli forces target ambulance team in south Lebanon", Al Jazeera reported.

- IRGC said the army and the IRGC are ready to respond forcefully to any "aggressive and criminal act of the enemies", IRGC public relations channel reported.

- US Central Command said USS Abraham Lincoln transits the Arabian Sea and no vessels are violating the blockade so far.

- US Treasury Secretary Bessent met with Italy's Giorgetti yesterday; also met with Ukraine PM; and with UK Chancellor Reeves and EU Commissioner Dombrovskis. Discussed Iran and Energy. Also met with Japan Finance Minister.

- French President Macron and UK PM Starmer are to hold a summit today on a plan to secure the Strait of Hormuz and are expected to brief US President Trump following the meeting, according to FT.

RUSSIA-UKRAINE

- Governor said that Russian drones attack damaged port infrastructure facilities in Ukraine’s Odesa region overnight.

- G7 reaffirmed backing for Ukraine, including energy needs ahead of winter, and agreed to sustain pressure on Russia while they discussed Chernobyl repair efforts and IMF reform progress.

CRYPTO

- Bitcoin regains the USD 75k handle, Ethereum holds above USD 2.3k.

APAC TRADE

- APAC stocks were mostly lower as markets lost steam following the recent rallies and with participants paring risk heading into the weekend, despite the Israel-Lebanon ceasefire taking effect and optimism by US President Trump regarding a deal between the US and Iran, which he said could resume talks over the weekend.

- ASX 200 was subdued with weakness seen in gold miners, financials and the consumer sectors, although the downside is limited amid a lack of fresh catalysts and a quiet data calendar.

- Nikkei 225 pulled back from its all-time record highs and just about returned to beneath the 59,000 level, with underperformance seen in some miners, manufacturers and semiconductor names.

- Hang Seng and Shanghai Comp conformed to the uninspired mood with the Hong Kong benchmark dragged lower by tech weakness, while participants also digested some earnings releases, including from Kweichow Moutai, which reported a 5% drop in FY profit.

NOTABLE ASIA-PAC HEADLINES

- Chinese scientists have reportedly developed diamond coating, which could improve cooling efficiency of AI data centres by around 80%, SCMP reported.

- China State Planner Vice Chair said economic operations are showing positive changes with significant improvements on both supply and demand side. Will reserve a batch of macro policy measures and roll out in a timely way based on needs.

- Fitch said China's credit outlook remains constrained by weak domestic demand, adds Iran war has added external pressure through weaker energy, trade and global demand.

- Japanese Finance Minister Katayama said Japan Bank for International Cooperation is to establish new investment window of up to JPY 600bln to assist Asian nations in securing energy supplies.

NOTABLE APAC DATA RECAP

- New Zealand Electronic Retail Card Spending YoY (Mar) Y/Y 2.7% (Prev. 1.5%).

- New Zealand Food Inflation YoY (Mar) Y/Y -0.6% (Prev. -0.1%).

- New Zealand Electronic Retail Card Spending MoM (Mar) M/M 0.7% (Prev. 1.4%).

Loading...