Trump gives 48-hour deadline for Iran to reopen the Strait; Precious metals slip on further hawkish pricing - Newsquawk US Market Open

- US President Trump gave Iran a 48-hour ultimatum on Saturday evening at 19:44EDT/23:44GMT to fully open the Strait of Hormuz or the US will “obliterate their various POWER PLANTS, STARTING WITH THE BIGGEST ONE FIRST”.

- Iran’s Revolutionary Guards warned that if US President Trump executes threats to target Iran’s energy facilities, the Strait of Hormuz will be completely closed and will not reopen until damaged plants are rebuilt.

- Crude buoyed amid US-Iran threat exchange, Brent trading above USD 100/bbl.

- European equities fall further into correction territory; US equity futures weak with ES holding at 6,500.

- DXY buoyed by geopolitics, AUD hit as metals prices sink.

- Fixed income falters as energy climbs and pricing turns ever more hawkish, also weighing on metals prices.

- Looking ahead, highlights include EU Consumer Confidence Flash (Mar), US Chicago Fed National Activity Index (Feb), Atlanta Fed GDP, Australian Flash PMIs (Mar), Japanese CPI (Feb). Speakers include ECB's Cipollone, Lane and Fed's Miran. Supply from the EU.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

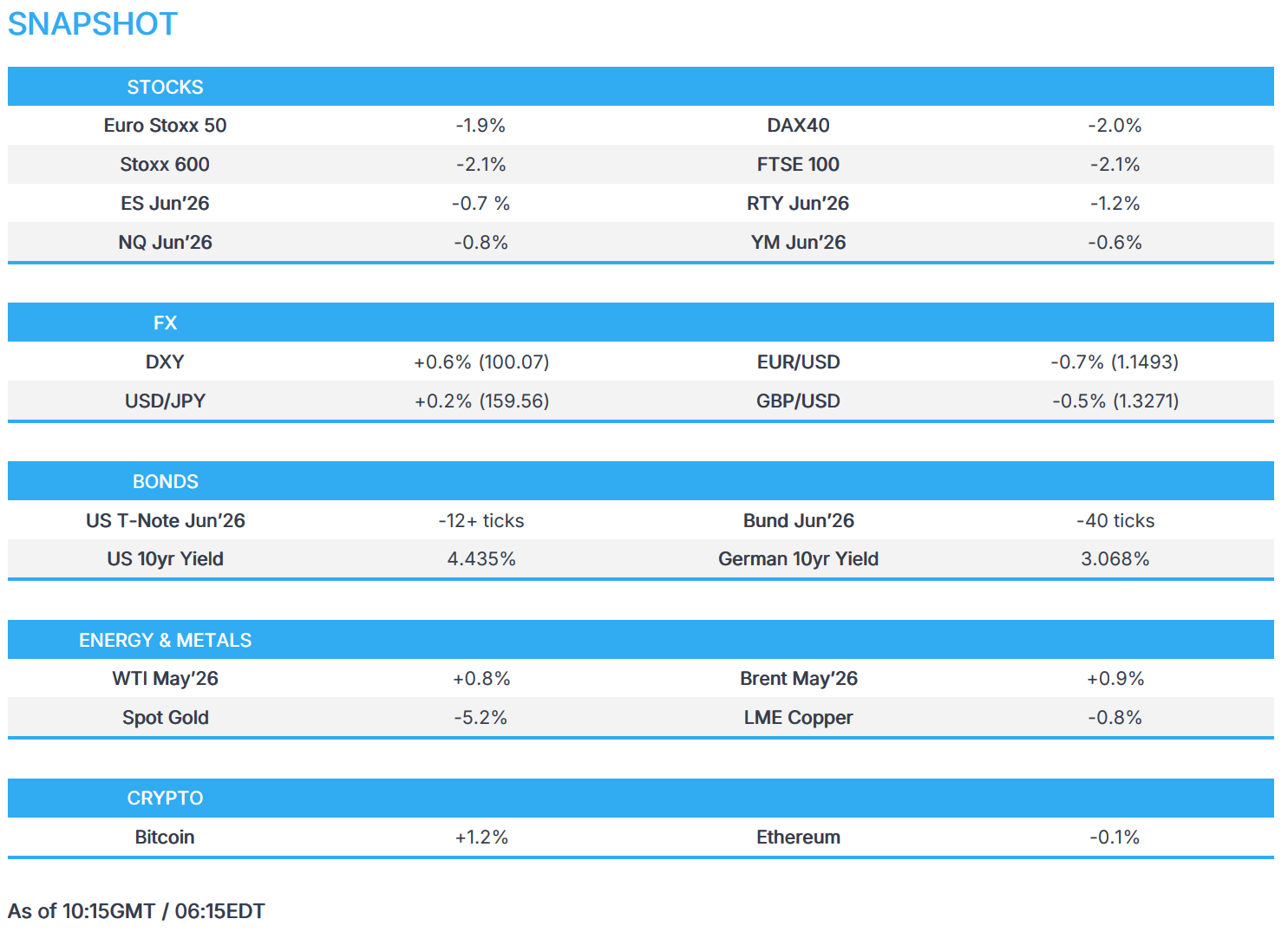

- European bourses (STOXX 600 -2.1%) start the trading week under significant pressure as Iran and the US exchanged threats over the weekend, with President Trump giving Iran a 48-hour deadline to reopen the Strait of Hormuz otherwise Iran's power plants will be targeted. IBEX 35 is the biggest loser, closely followed by the FTSE MIB.

- Sectors are entirely in the red, with Real Estate and Basic Resources residing at the bottom of the pile as higher yields weigh on the housing sector, while metals slip lower on a stronger dollar and further rate hikes being priced in. Consumer Products and Services sit at the top of the pile.

- US equity futures (ES -0.7% NQ -0.8% RTY -1.2%) remain under pressure, following the global risk tone. For the NQ, the 20-, 200-SMA are about to cross. The last time this happened, in 2025, the NQ sold off an additional 17%. JPM's tactical positioning monitor has also turned the most bearish for the SPY since July 2024 and its positioning indicator shows ETF selling/shorting has picked up.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is stronger this morning and currently holds towards the upper end of a 99.51 to 100.01 range. As has been the case for the past few weeks, geopolitics remains the main driver for the index – and the downbeat risk tone plays in favour of the USD. A full geopolitical analysis piece is on the Newsquawk feed (08:30 GMT), but in brief US President Trump gave Iran a 48-hour ultimatum on Saturday, noting that if it does not fully open the Strait of Hormuz it would “obliterate” various power plants. Iran responded by suggesting it would completely close the Strait if its power plants were struck, and not reopen until they were rebuilt. It seems, for now, that Iran is calling Trump’s bluff.

- G10s are broadly lower vs the USD. The Aussie underperforms, hampered by the significant losses in precious/base metals prices; AUD/USD has slipped below its 50 DMA (0.6995), to a session low of 0.6938. Other net importers of energy also remain on the backfoot – the CHF, EUR and GBP all extend losses. Perhaps a little redundant at the moment (given geopolitics), but there were some regional political updates out of France and Germany. For the former, local election results were mixed with France's far-right RN winning in smaller cities, whilst losing in bigger ones. For Germany, Chancellor Merz’s CDU won in Rhineland-Palatinate elections, clouding the outlook for SPD, who had previously been in power for 35 years. This brings the potential of two extremes for the dwindling SPD, ING writes. 1) SPD becomes a “genuine junior partner” and pass through reforms proposed by the CDU, 2) SPD blocks reforms, leading to government breakup.

- JPY fares a bit better vs peers, with USD/JPY remaining within a 159.01-159.65 range. On the wages front, Japan's largest trade union group Rengo said prelim data shows average wage hikes of 5.26% for 2026 (vs last year's prelim 5.46%). As a reminder, BoJ Governor Ueda said at March's post-policy press conference that "prelim data shows wage momentum at small and medium sized firms could be better than in past years". The second round is expected on March 27, while final data is typically released in early July. Revisions to the prelim data are generally expected. In the meantime, some attention on potential intervention, with Top FX Diplomat Mimura the latest official to provide some jawboning. Nonetheless, intervention surrounding the current volatile environment seems unlikely at this stage.

FIXED INCOME

- A bearish session for fixed benchmarks, pressure stems from the weekend's geopolitical escalation, which has once again lifted energy prices. Furthermore, given those moves and a continued hawkish assessment of Central Bank expectations, yields are on the up. Specifically, US yields are firmer across the curve in bear-flattening action as the short-end very much leads. The 2yr has peaked at 3.99%, its highest since August 2025 when 3.999% printed; thereafter, we look of course to the figure and then the 4.424% 2025 peak.

- Action that has pushed USTs to a 110-04+ contract low. For the Fed, we continue to see a hawkish reassessment, though, unlike global peers, a hike is not yet fully priced in 2026. As it stands, pricing peaks in October with c. 20bps of tightening implied.

- Bunds are lower, at a 124.80 base with losses of near 50 ticks at most. The story is much the same as above. For the ECB, pricing is much more extreme with three 2026 hikes currently fully priced and at extremes this morning a 50/50 chance of a fourth hike. As a reminder, the ECB's baseline forecasts were based on market pricing as of the 13th, around which point around 40bps of tightening was implied. For EGBs, it is worth noting that the weekend's political updates relating to Germany and France would typically be of note for the complex, but in today's energy/Central Bank-driven market, the pertinence of the results has been significantly diminished. In terms of spreads, the BTP-Bund 10yr yield spread has eclipsed 100bps for the first time since June 2025 when 102.4bps printed.

- For the BoE the dynamic is even more extreme, with 100bps of 2026 tightening implied by end-2026. For Gilts, the benchmark opened with losses of 63 ticks and then slipped almost another 50 to a 86.07 trough.

- Germany Q2 debt issuance plan unchanged from its original plan in December 2025.

COMMODITIES

- Firmer price action across crude after US President Trump at the weekend threatened attacks on power plants around the Strait of Hormuz if Iran does not open the Strait by Monday. Iran’s Revolutionary Guards warned that if US President Trump executes threats to target Iran’s energy facilities, the Strait of Hormuz will be completely closed and will not reopen until damaged plants are rebuilt. Furthermore, Iranian Parliamentary speaker suggested if “power plants and infrastructure in our country are targeted, the critical infrastructure, energy infrastructure, and oil facilities throughout the region will be considered legitimate targets and will be destroyed in an irreversible manner, and the price of oil will remain high for a long time”. This morning, Iran's Defense Council threatened to deploy naval mines across the 'entire Persian Gulf' if a land invasion happens, AP reported.

- Crude prices rose overnight as investors assessed Trump’s ultimatum; Brent climbed toward USD 114.43/bbl (vs low 110.22/bbl) and WTI rise to a USD 101.67/bbl peak before waning to sub-USD 100/bbl and then a bit more, with the US largely cushioned from the Middle Eastern supply woes given domestic production capabilities.

- Spot gold has now erased its 2026 gains, falling again as the Middle East war, now in its fourth week, increased inflation risks and expectations that central banks will struggle to lower rates. The bullion has fallen from a USD 4,536/oz peak down to USD 4,099.02/oz in just today’s session thus far, and found support just above its 200 DMA (USD 4,090.97/oz) before rebounding to ~USD 4,250/oz.

- In terms of base metals, copper fell to its lowest in more than three months amid the reduced risk appetite, inflation and growth concerns. 3M LME copper resides sub-USD 12k/t in a current USD 11,707.00- 11,911.00/t range. Elsewhere, Mysteel Global suggested Chinese copper inventories had their biggest weekly drop this year, as the rapid slump in prices of the metal amid the Iran war kept demand afloat.

- IEA chief Birol said Asia is at the forefront of this energy crisis and the situation in the Middle East is severe, adds this crisis is worse than the two oil crises in the 1970s put together. Said this is the single biggest solution to the current problems is to reopen the Strait of Hormuz.

- Saudi Aramco cuts crude oil supplies to Asian buyers for April loading.

- Indian PM Modi said the government is ensuring uninterrupted oil and gas supply; India has over 5.3mln metric tons of strategic petroleum reserves; India is working on 6.5mln metric tons more of reserves.

- China's NDRC said to raise gas prices by CNY 1,160/ton and diesel prices by CNY 1,115/ton, effective March 24th; adds measures will be temporarily used to regulate oil prices.

- Greek PM said Greece is to offer fuel subsidies worth EUR 300mln to help households with rising energy costs.

- Sinopec (0338 HK) VP said there is not much Russian oil available under the waiver and are evaluating risks of buying Iranian oil.

- ADNOC Gas said it made temporary adjustments to LNG production.

- China state refiners are said to be exploring Iran oil deals following US waiver.

- Japan is to spend around JPY 800bln from budget reserves to curb gasoline prices, according to NHK.

NOTABLE EUROPEAN HEADLINES

- German Chancellor Merz’s CDU was projected to have won 30.8% of the vote vs. Social Democrats with 26% in Rhineland-Palatinate, to remove the Social Democrats from power in the state after 35 years.

- France's far-right RN sees mixed results in local elections winning in smaller cities, but losing in big targets such as Marseille and Toulon, while RN ally Ciotti was elected Mayor of Nice, according to FT.

CENTRAL BANKS

- ECB's Kazimir says will not hesitate to take action if inflation was at risk of staying above target for a prolonged period; can do little about the inflation spoke in the next few months; yet to leave our "good place".

- ECB's de Guindos said he sees Euro zone avoiding recession and can't prevent initial surge from energy, adds ready to respond as necessary.

- ECB Wage Tracker: 2026 annual 2.270% (prev. 2.388%). Quarterly, 2026. Q1 1.887% (prev. 2.058%). Q2 2.100% (prev. 2.169%). Q3 2.521% (prev. 2.617%). Q4 2.574% (prev. 2.709%).

- Academics and reflationists Toichiro Asada and Ayano Sato have been confirmed as BoJ board members.

- NBP's Glapinski said deflationary pressures are to offset high energy prices.

NOTABLE US HEADLINES

- US President Trump posted "I don’t think we should make any deal with the Crazy, Country Destroying, Radical Left Democrats unless, and until, they Vote with Republicans to pass “THE SAVE AMERICA ACT.”.

- US senators are to introduce a bipartisan legislation on Monday to prohibit entities regulated by the CFTC, including prediction-market exchanges Kalshi and Polymarket’s US platforms, from listing contracts related to sporting events, WSJ reports

- Laguardia Airport official said the airport will be shut until at least 14:00 EDT / 18:00 GMT, via Bloomberg.

GEOPOLITICS

MIDDLE EAST

- US President Trump gave Iran a 48-hour ultimatum on Saturday evening at 19:44EDT/23:44GMT to fully open the Strait of Hormuz or the US will “obliterate their various POWER PLANTS, STARTING WITH THE BIGGEST ONE FIRST”. US President Trump posted earlier on Saturday that he is considering "winding down" the Iran war because the US was "getting very close" to meeting its military objectives.

- Iran’s Revolutionary Guards warned that if US President Trump executes threats to target Iran’s energy facilities, the Strait of Hormuz will be completely closed and will not reopen until damaged plants are rebuilt, while it warned that all Israeli power plants, energy infrastructure and ICT systems will be widely targeted. Iran also threatened that all similar companies in the region that have American shareholders will be ‘completely destroyed’ and power plants in regional countries that host US bases will become legitimate targets.

- Iran's Defense Council threatens to deploy naval mines across the 'entire Persian Gulf' if a land invasion happens, AP reported.

- Iranian Foreign Ministry denies the allegations that it targeted the Diego Garcia base with missiles; calling the attack an "Israeli false flag".

- US fighter jet has reportedly crashed in Kuwait, Al-Ahd News reported; jet was hit and fell a few minutes ago, reported suggest jet was hit in Iranian airspace and subsequently crashed in Kuwait, Iranian press reported.

- Power outages reported in Tehran amid Israeli strikes, according to NYT.

- Israeli military said it has begun a wide-scale wave of strikes targeting Iranian infrastructure in Tehran.

- Iraqi pro-Iranian military group Kata'ib Hezbollah extends pause on US embassy attacks by five days but warns of a response if attacked, according to AFP.

- UK PM Starmer spoke with US President Trump and discussed the need to reopen the Strait of Hormuz.

RUSSIA-UKRAINE

- Russia's Primorsk and Ust-Luga ports have reportedly suspended oil and fuel loadings since March 22nd amid drone attacks, sources suggest.

- Ukraine said it struck the Saratov refinery in an attack that targeted Russian energy facilities.

CRYPTO

- Bitcoin finds support at USD 68k, Ethereum nears USD 2k.

APAC TRADE

- APAC stocks were pressured after the US and Iran exchanged threats over the weekend, with US President Trump announcing a 48-hour ultimatum for Iran to fully open the Strait of Hormuz or the US will obliterate Iranian power plants, while Iran responded with its own threats, including completely shutting the Strait of Hormuz until damaged plants are rebuilt and warned that all power plants in regional countries that host US bases will become legitimate targets.

- ASX 200 retreated amid continued underperformance in miners, materials and resources, while defensives were at the other end of the spectrum amid the broad risk-off mood.

- Nikkei 225 slumped firmly beneath the 52,000 level and suffered intraday losses of more than 2,000 points on return from a 3-day weekend amid energy-related headwinds, while Japanese Foreign Minister Motegi denied that Japan was considering unilateral negotiations with Iran to secure passage for vessels through the Strait of Hormuz.

- Hang Seng and Shanghai Comp conformed to the broad downbeat mood as participants reflected on a slew of earnings, while rehashed rhetoric from PBoC Governor Pan that they will continue to implement appropriately loose monetary policy, provided little solace.

NOTABLE ASIA-PAC HEADLINES

- Japan's largest trade union group Rengo says prelim data shows average wage hikes of 5.26% for 2026 (vs last year's prelim 5.46%).

- Japan's top FX diplomat Mimura said will do utmost to respond to FX as needed, and that the government will take steps against FX moves at any time.

- Japan is considering a reducing buyback of inflation-linked government bonds as investor demand increases amid rising inflation expectations, according to sources.

- Japan's Chief Cabinet Secretary Kihara said the government may consider a provisional budget to prepare for unforeseen circumstances.

Loading...