Trump highlights the desire to keep current deals; Nvidia earnings awaits - Newsquawk EU Market Open

- APAC stocks traded higher as the region took impetus from the rebound on Wall Street after Anthropic's presentation helped soothe some AI/software concerns, and with tech also bolstered by the USD 60bln Meta-AMD chip deal; Euro Stoxx 50 futures up 0.2% after the cash market closed flat on Tuesday.

- US President Trump talked up the economy in his State of the Union Address, saying that the nation is back, bigger, better and stronger than before, while he added that we've seen nothing yet.

- Regarding tariffs, Trump said the Supreme Court decision on tariffs is very unfortunate but added that tariffs will remain in place and nearly all countries want to keep the trade deals.

- Trump also commented on Iran, which he claimed is working on missiles that could soon reach the US, and noted Iran wants to make a deal but hasn't yet said that it won't pursue nuclear weapons.

- Antipodeans were firmer amid the positive risk appetite, and with AUD/USD leading the advances following firmer-than-expected monthly CPI data from Australia.

- Looking ahead, highlights include German GfK (Mar), GDP Final (Q4), Swiss Sentiment (Feb), EZ HICP Final (Jan). Speakers include RBA’s Bullock, Fed’s Musalem, Barkin & Schmid. Supply from Germany & US. Earnings from NVIDIA, Salesforce, Snowflake, TJX Companies, Lowe's, Synopsys & Bayer.

SNAPSHOT

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

US TRADE

EQUITIES

- US stocks gained as the initial weakness, amid declines in NVIDIA shares, was reversed and buoyed by the Anthropic presentation just after the open, which boosted many names that Anthropic announced they are, or will be, partnering with, potentially quelling some AI disruption fears surrounding these names. As such, a lot of the stocks that were recently hit by AI disruption fears like software turned, while sectors were predominantly firmer, with Consumer Discretionary and Technology atop the breakdown, in which the latter was also boosted by AMD (+8.7%), after they signed a deal with META, while Salesforce (+4.1%) gained after Anthropic, in their presentation, noted they are “leading the transformation”.

- SPX +0.77% at 6,890, NDX +1.09% at 24,977, DJI +0.76% at 49,175, RUT +1.20% at 2,652.

- Click here for a detailed summary.

STATE OF THE UNION

- US President Trump talked up the economy in his State of the Union Address, saying that the nation is back, bigger, better and stronger than before, while he added that we've seen nothing yet and this is the golden age of America. Trump said they have achieved a transformation like never before and a turnaround for the ages, as well as stated that low interest rates will solve the housing problem, and they want to protect home values and keep them up. He also commented that inflation is plummeting, salaries are rising, and the roaring economy is roaring like never before. Regarding tariffs, Trump said the Supreme Court decision on tariffs is very unfortunate, but added that tariffs will remain in place and nearly all countries want to keep the trade deals, while he also stated that congressional action won't be needed on tariffs. Trump also commented on Iran, which he claimed is working on missiles that could soon reach the US, and noted Iran wants to make a deal but hasn't yet said that it won't pursue nuclear weapons, while he reiterated that his preference is to resolve Iran's nuclear issue through diplomacy.

TARIFFS/TRADE

- US House Speaker Johnson said codifying some of the tariffs would be difficult and they will have discussions on tariffs in the coming weeks, according to a Fox Business Interview.

- US Commerce Department official understands that no NVIDIA (NVDA) H200s have been sold to China yet. In other news, the US Commerce Department set preliminary countervailing duties on solar panels from India, Indonesia and Laos.

- German Chancellor Merz said decoupling from China would hamper economic opportunities, while he added it is crucial that Sino-German competition is fair and transparent.

- Chinese Premier Li said in a meeting with German Chancellor Merz that China is willing to bolster dialogue, communication and mutual trust.

NOTABLE HEADLINES

- Fed's Barkin (2027 voter) said it is clear sense that the job market has loosened and it is hard to calibrate what's going on with labour supply, while he added that inflation data has been consistently above target. Furthermore, Barkin said he is hopeful inflation is retreating to 2%, but wants data to show this clearly and said monetary policy is currently well positioned for risks.

- Fed's Collins (2028 voter) said they are quite likely to hold current rates for some time and noted that policy is mildly restrictive and may be close to neutral, while she added that recent job data has been promising and the job market softened last year, but wasn't soft. Collins said she wants more confidence that inflation is easing, and the Baseline view is that inflation will wane later this year, as well as noted that the latest tariff news hasn't changed the outlook much.

APAC TRADE

EQUITIES

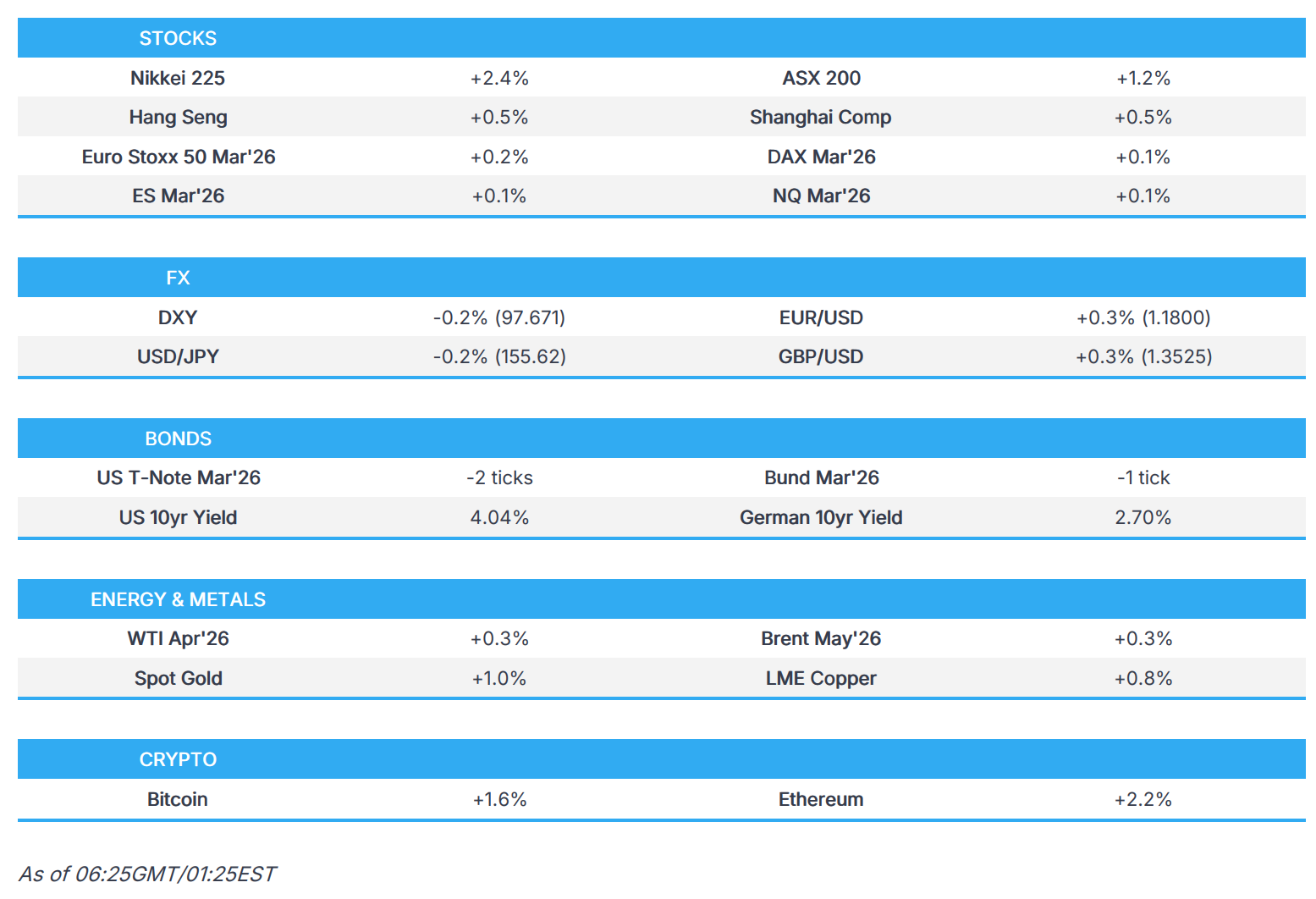

- APAC stocks traded higher as the region took impetus from the rebound on Wall Street after Anthropic's presentation helped soothe some AI/software concerns, and with tech also bolstered by the USD 60bln Meta-AMD chip deal.

- ASX 200 advanced with gains led by notable outperformance in the tech, consumer staples and mining sectors, while participants continue to digest an overload of earnings and are unfazed by firmer-than-expected CPI data.

- Nikkei 225 rallied to a fresh record high as exporters benefitted from recent currency weakness after it was reported that Japanese PM Takaichi relayed to BoJ Governor Ueda her reservations about further rate hikes.

- Hang Seng and Shanghai Comp conformed to the broad upbeat risk sentiment, with attention in Hong Kong on the annual budget and with the mainland underpinned with the PBoC conducting a CNY 600bln MLF operation.

- US equity futures were rangebound after the prior day's rebound and with a muted reaction to US President Trump's State of the Union Address, where he talked up the US economy and refrained from any major fresh policy announcements, while participants also look ahead to key earnings later from NVIDIA.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.2% after the cash market closed flat on Tuesday.

FX

- DXY mildly softened in rangebound trade with little reaction to US President Trump's State of the Union Address, where he talked up the US economy as he stated the nation is back, bigger, better and stronger than before, as well as noted that inflation is plummeting, salaries are rising, and the roaring economy is roaring like never before. There were also several Fed comments, but they did little to shift the dial as Goolsbee (2027 voter) reiterated that more progress is needed on inflation before resuming rate cuts, while Cook (voter) said the neutral rate could fall over time, and Collins (2028 voter) said they are quite likely to hold current rates for some time.

- EUR/USD eked mild gains and looks to retest the 1.1800 level amid a lacklustre dollar and after comments yesterday from EU's Sefcovic that US counterparts reassured the EU that they will stand by the trade deal.

- GBP/USD gradually rebounded after the prior day's fluctuations and deluge of BoE remarks, in which the main takeaway is that a cut in April/May remains an open question, with Governor Bailey stating that he will be going into the coming meetings asking if a cut is justified.

- USD/JPY mildly pulled back after surging yesterday on a report that Japanese PM Takaichi relayed to BoJ Governor Ueda reservations about further rate hikes, being stricter than their previous meeting, while Takaichi more recently commented that she is closely watching FX moves with a high sense of urgency.

- Antipodeans were firmer amid the positive risk appetite, and with AUD/USD leading the advances following firmer-than-expected monthly CPI data from Australia.

- PBoC set USD/CNY mid-point at 6.9341 vs exp. 6.8824 (Prev. 6.9414).

- SNB Chairman Schlegel said Swiss inflationary pressure has barely changed, and the central bank expects growth around 1% in 2026, while he believes inflation will rise in the next few months and stated it is possible there will be a few months with negative inflation, but added that it is not an alarm signal as they look at inflation over the mid-term.

FIXED INCOME

- 10yr UST futures were slightly lower after the choppy performance during US trade, where the curve flattened as some of the recent AI disruption fears were allayed after Anthropic announced a slew of new partnerships, while there was little reaction seen during Trump's State of the Union Address.

- Bund futures lacked direction following the prior day's indecision and with Bund issuances and GfK data scheduled today.

- 10yr JGB futures faded some of the prior day's gains that were facilitated by reports that Japanese PM Takaichi relayed to BoJ Governor Ueda her reservations about further rate hikes, while there were some headwinds seen following the latest enhanced-liquidity auction for long- to super-long JGBs.

COMMODITIES

- Crude futures were mildly positive but with gains capped after the prior day's choppy price performance in which pressure was seen after comments from Iran's Deputy Foreign Minister that Tehran is ready to take any necessary step to reach a deal with the US, and a strike on Iran is a real gamble, while there was some indecision seen amid US President Trump's comments on Iran in which he claimed that Iran is working on missiles that could hit the US, but also stated Iran wants a deal and his preference would be a solution through diplomacy.

- US Private inventory data (bbls): Crude +11.4mln (exp. +1.5mln), Distillate -2.8mln (exp. -1.6mln), Gasoline -1.5mln (exp. -0.6mln), Cushing +1.8mln.

- Spot gold gradually edged higher with upward momentum seen as Shanghai commodities trading got underway and amid a marginally softer dollar.

- Copper futures remained afloat around the USD 6.00/lb level after gaining yesterday amid the turnaround in risk sentiment.

CRYPTO

- Bitcoin rallied overnight and briefly returned to USD 66k territory amid the broad risk-on sentiment.

NOTABLE ASIA-PAC HEADLINES

- China aims to boost output of relatively advanced chips to 100k wafers in 1-2 years and has set a target of adding an additional 500k wafers of capacity by 2030, according to Nikkei.

- Key Chinese provinces are to raise technology spending in 2026 budget reports, including Guangdong, Zhejiang and Hainan, according to China Securities Journal.

- Hong Kong Financial Secretary Chan said in the Budget Address that 2025 GDP rose 3.5% and the domestic economic trend is to continue to be good in 2026, while the government sees 2026 GDP at 2.5%-3.5% and an average growth of 3.0% per year in real terms for 2027-2030. Furthermore, the city will deepen integration in line with China's 5-year plan and will unveil its first dedicated five-year development plan.

- Japanese PM Takaichi said they are closely watching FX moves with a high sense of urgency.

- Japanese Deputy Chief Cabinet Secretary Sato said he is aware of a report that PM Takaichi voiced apprehension about additional BoJ rate hikes, while he stated Takaichi did not have a specific request and there is 'nothing more or less than that'.

- Japan's government nominated academics Toichiro Asada and Ayano Sato to replace outgoing BoJ board members Asahi Noguchi and Junko Nakagawa.

DATA RECAP

- Australian Inflation Rate YY (Jan) 3.8% vs. Exp. 3.7% (Prev. 3.8%, Low. 3.4%, High. 4%)

- Australian RBA Trimmed Mean CPI YY (Jan) 3.4% vs. Exp. 3.3% (Prev. 3.3%, Low. 3.2%, High. 3.3%)

GEOPOLITICS

MIDDLE EAST

- US Senator Cruz said we are likely to see limited strikes on Iran in a matter of days and will not see ground forces on the ground, according to Asharq News.

- Iranian Foreign Minister Araghchi said Tehran will resume talks with the US in Geneva with a determination to achieve a 'fair and equitable deal in the shortest possible time', while he added that Iran will under no circumstances ever develop a nuclear weapon, nor will it ever forgo the right to harness the dividends of peaceful nuclear technology for its people. Araghchi also said they have a historic opportunity to strike an unprecedented agreement and that a deal is within reach, but only if diplomacy is given priority.

RUSSIA-UKRAINE

- Washington warned Ukraine not to strike targets within Russia that could hit US economic interests, according to FT citing Kyiv’s ambassador to Washington.

OTHER

- US imposed cyber-related sanctions on Russian and UAE individuals and entities.

EU/UK

NOTABLE HEADLINES

- UK Chancellor Reeves is facing renewed calls to cut the bank tax as UK competitiveness lags, according to CityAM.

Loading...