Trump raises tariffs on South Korean sectors; Equities trade higher ahead of a busy week of earnings - Newsquawk EU Market Open

- APAC stocks were mostly higher following on from the rebound on Wall Street, but with some of the gains capped ahead of key events and big tech earnings stateside.

- KOSPI sold off at the open following US President Trump's announcement to raise tariffs on South Korean autos, lumber, pharma, and all other reciprocal tariffs to 25% from 15% due to its legislature not yet enacting the US-Korea trade deal.

- Spot gold rebounded from the prior session's trough with a brief pullback cushioned after finding support around the USD 5,000/oz level.

- US aircraft carrier and warships reached the Middle East, according to the Washington Post, while it was also reported that a US official said Washington is "open for business" if Iran wishes to contact them.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.4% after the cash market closed with gains of 0.2% on Monday.

- Looking ahead, highlights include US Richmond Fed (Jan), Consumer Confidence (Jan), ADP Employment Change Weekly, NBH Policy Announcement. Speakers include ECB President Lagarde & ECB’s Nagel, US President Trump. Supply from UK, Italy, Germany and US. Earnings from Texas Instruments, UnitedHealth, Boeing, UPS, General Motors, RTX, American Airlines, Logitech & LVMH.

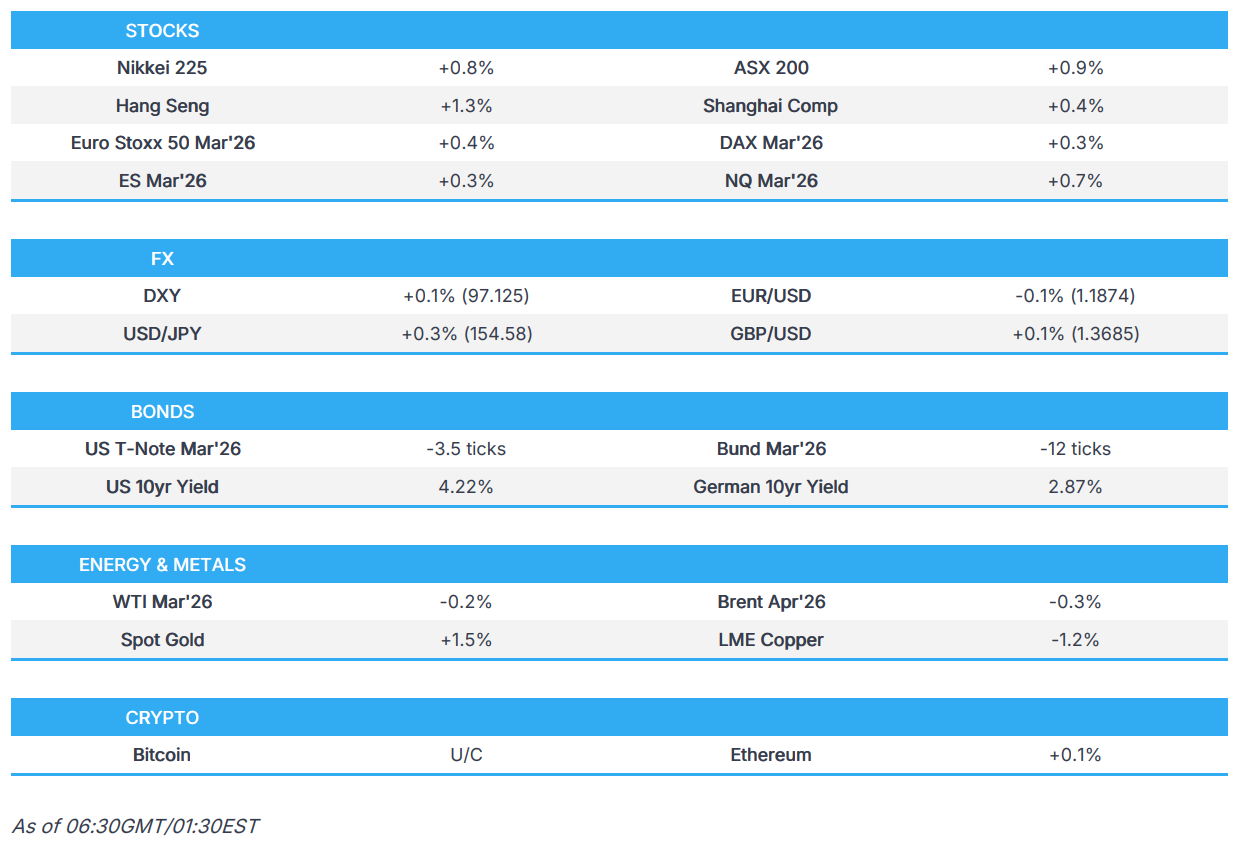

SNAPSHOT

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

US TRADE

EQUITIES

- US stocks closed higher on Monday as sentiment recovered ahead of a busy and important week of earnings (MSFT, META, TSLA, AAPL, ASML). Futures had initially dipped on Sunday, with downside sparked by Trump's threat of 100% tariffs on Canada over recent trade ties with China, as well as the potential for a partial government shutdown following disagreement over ICE funding after a Minneapolis shooting on the weekend, but then gradually recouped the losses throughout APAC and EU trade.

- Sector performance was led by Communications and Tech, but Consumer Discretionary lagged and was the sole sector in the red, while Microsoft gained after it announced the Maia 200 chip, in the latest challenge to NVIDIA, which resulted in modest losses in NVDA shares.

- SPX +0.5 at 6,950, NDX +0.4% at 25,713, DJIA +0.6% at 49,412, RUT -0.4% at 2,659.

- Click here for a detailed summary.

TARIFFS/TRADE

- US President Trump posted "Because the Korean Legislature hasn't enacted our Historic Trade Agreement, which is their prerogative, I am hereby increasing South Korean TARIFFS on Autos, Lumber, Pharma, and all other Reciprocal TARIFFS, from 15% to 25%".

- South Korean Industry Ministry said the Minister is to visit the US soon and meet with Commerce Secretary Lutnick. In relevant news, a South Korean ruling party official said bills to enact US investment have been introduced and will soon be reviewed, while the ruling party aims to pass a special act on the US trade deal by the end of February.

- European Parliament International Trade Committee Chair Lange said there is no decision on the US-EU trade agreement vote, and the decision on moving ahead with the US trade agreement is delayed until February 4th.

NOTABLE HEADLINES

- US President Trump posted that he "had a very good telephone conversation with Mayor Jacob Frey, of Minneapolis. Lots of progress is being made! Tom Homan will be meeting with him tomorrow in order to continue the discussion". It was also reported that top Border Patrol official Bovino was removed from his role as US Border Patrol commander at large.

- US President Trump's admin proposes keeping the rates that Medicare pays insurers steady, according to WSJ citing officials from the CMS and the White House. Under the proposal, payments to the plans would increase by an estimated .09% on average in 2027, and the CMS is also proposing to eliminate a lucrative industry billing practice that has raised concerns with government watchdogs and was among the tactics examined in reporting by WSJ on Medicare insurers.

APAC TRADE

EQUITIES

- APAC stocks were mostly higher following on from the rebound on Wall Street, but with some of the gains capped ahead of key events and big tech earnings stateside, while participants also digested Trump's latest tariff salvo against South Korea.

- ASX 200 rallied on return from the long weekend, with risk appetite also facilitated by M&A-related headlines and improved business sentiment.

- Nikkei 225 gained despite the initial indecision following recent currency moves and after Services PPI cooled but remained above the BoJ's price target.

- KOSPI sold off at the open following US President Trump's announcement to raise tariffs on South Korean autos, lumber, pharma, and all other reciprocal tariffs to 25% from 15% due to its legislature not yet enacting the US-Korea trade deal. However, the index then clawed back its losses and more, with the TACO trade likely in play and with South Korean officials attempting to appease Trump.

- Hang Seng and Shanghai Comp traded somewhat mixed with firm gains in Hong Kong led by Zijin Mining, which is to buy Canada's Allied Gold for USD 4bln, while the mainland index lagged despite an acceleration in Chinese Industrial Profits and the PBoC's liquidity efforts.

- US equity futures kept afloat following yesterday's rebound but with upside capped as markets await Mag 7 earnings and after Dow futures wobbled as UnitedHealth shares were pressured on news that the Trump administration proposes keeping the rates steady that Medicare pays insurers.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.4% after the cash market closed with gains of 0.2% on Monday.

FX

- DXY was rangebound after weakening yesterday as the continued trade conflict left the de-dollarisation trade intact after US President Trump threatened Canada with 100% tariffs and announced to raise tariffs on South Korean autos, lumber, pharma, and all other reciprocal tariffs to 25% from 15% due to its legislature not yet enacting the US-Korea trade deal. Nonetheless, price action is contained as participants await tomorrow's FOMC and with several data releases scheduled later today, including US Consumer Confidence, Richmond Fed and ADP Weekly Employment Change.

- EUR/USD briefly reapproached the 1.1900 handle before hitting resistance, while newsflow from the bloc was light, although ECB's Lagarde and Nagel are scheduled to speak later today.

- GBP/USD initially retested the 1.3700 level to the upside amid a softer dollar, and with the latest UK BRC Shop Price Index showing that major retailer prices rose at the fastest pace in almost two years, although later returned to flat territory.

- USD/JPY continued its rebound from the prior day's trough and the brief dip beneath the 154.00 level, amid the positive risk appetite and following the latest Services PPI data in Japan, which slightly softened from prior but remained above the central bank's price target.

- Antipodeans were little changed in the absence of tier-1 data releases and amid the somewhat cautious gains in stocks.

FIXED INCOME

- 10yr UST futures were contained heading closer to Wednesday's FOMC, and as markets continue to await President Trump's Fed Chair pick, while participants are also looking ahead to data releases and a 5-year note auction due later.

- Bund futures pulled back from yesterday's peak after hitting resistance around the 128.00 level, and with demand constrained as supply looms, including a EUR 6.0bln Schatz issuance due later, followed by a similar amount in tomorrow's Bund offering.

- 10yr JGB futures declined amid a resumption of the upside in JGB yields and with the curve steepening, following the latest Japanese Services PPI data, which slightly cooled from previous to 2.6% (Prev. 2.7%) but remained above the central bank's price target.

COMMODITIES

- Crude futures were lacklustre following the prior day's flimsy performance, with Kazakhstan set to resume production at its biggest oilfield, while a previous report also noted that OPEC+ is likely to maintain its supply pause in March.

- US President Trump is said to be mulling a cap on California state fuel tax and vowed to drive down the state's gas prices, according to the NY Post.

- Spot gold rebounded from the prior session's trough with a brief pullback cushioned after finding support around the USD 5,000/oz level.

- Copper futures continued to fade their recent gains after failing to sustain a brief return above the USD 6/lb level, and with demand not helped by the cautious mood in its largest buyer, China.

CRYPTO

- Bitcoin gradually climbed higher throughout the session amid the cautiously positive sentiment overnight, but remained beneath the USD 90k level.

NOTABLE ASIA-PAC HEADLINES

- China is to roll out a policy document on boosting jobs amid AI impact, while it will launch policies to support employment alongside the AI shift and will boost support for employment among key groups, according to Xinhua.

DATA RECAP

- Chinese Industrial Profits YY (Dec) 5.3% (Prev. -13.1%)

- Chinese Industrial Profits YTD YY (Dec) 0.6% (Prev. 0.1%)

- Japanese Services PPI (Dec) 2.6% vs Exp. 2.7% (Prev. 2.7%)

- Australian NAB Business Confidence (Dec) 3 (Prev. 1)

- Australian NAB Business Conditions (Dec) 9 (Prev. 7)

GEOPOLITICS

MIDDLE EAST

- Palestinian media reported Israeli artillery shelling targeting areas in Khan Yunis in the southern Gaza Strip, according to Sky News Arabia.

- US President Trump said Iran wants a deal as the US "armada" arrives and the situation with Iran is "in flux" because he sent a "big armada" to the region, although he thinks Tehran genuinely wants to cut a deal, according to Axios. Sources with knowledge of the situation said that Trump hasn't made a final decision and will likely hold more consultations this week and be presented with additional military options, while he said diplomacy remained an option and that Iran wants to make a deal and wants to talk, and has called on numerous occasions.

- US aircraft carrier and warships reached the Middle East, according to the Washington Post, while it was also reported that a US official said Washington is "open for business" if Iran wishes to contact them.

RUSSIA-UKRAINE

- Ukrainian President Zelensky said regarding talks with Russia that the primary discussions were about military issues. Zelensky also commented that the delegation discussed steps to end the war and its monitoring, while he added that a Ukraine-Russia meeting can happen on Sunday, but it would be good if it is sooner, and they need real results from diplomacy, not Russia once again postponing pressure.

- US President Trump's administration has signalled to Ukraine that US security guarantees are contingent on Kyiv first agreeing a peace deal that would likely involve ceding the Donbas region to Russia, according to sources cited by FT.

- White House said President Trump is not giving up on the Ukraine peace process, while it was separately reported that Germany said it cannot supply Ukraine with new Patriot systems.

OTHER

- US President Trump said he is pleased to report that Venezuela is releasing its political prisoners at a rapid rate, which will be increasing over the coming short period of time.

- Brazilian President Lula agreed to visit Washington soon in a call with US President Trump, while they discussed Venezuela and emphasised the importance of maintaining peace and stability in the region.

EU/UK

NOTABLE HEADLINES

- BoE Governor Bailey said in an article in The Banker that banks’ present stability is hard won and that banks are now better equipped to absorb losses in crises, while he added there is an urgent need to boost resilience in market-based finance.

DATA RECAP

- UK BRC Shop Price Inflation (Jan) 1.5% vs. Exp. 0.7% (Prev. 0.6%, Rev. From 0.7%)

Loading...