US equity futures firm, USD attracts carry demand to the detriment of low-yielders - Newsquawk US Market Open

- Islamabad is the more likely option for the next round of US-Iran technical talks, with July 11th expected to be the date, Fox reported.

- OPEC+ agreed to raise output targets by an additional 188k bpd, in line with the group's plan to reverse output curbs.

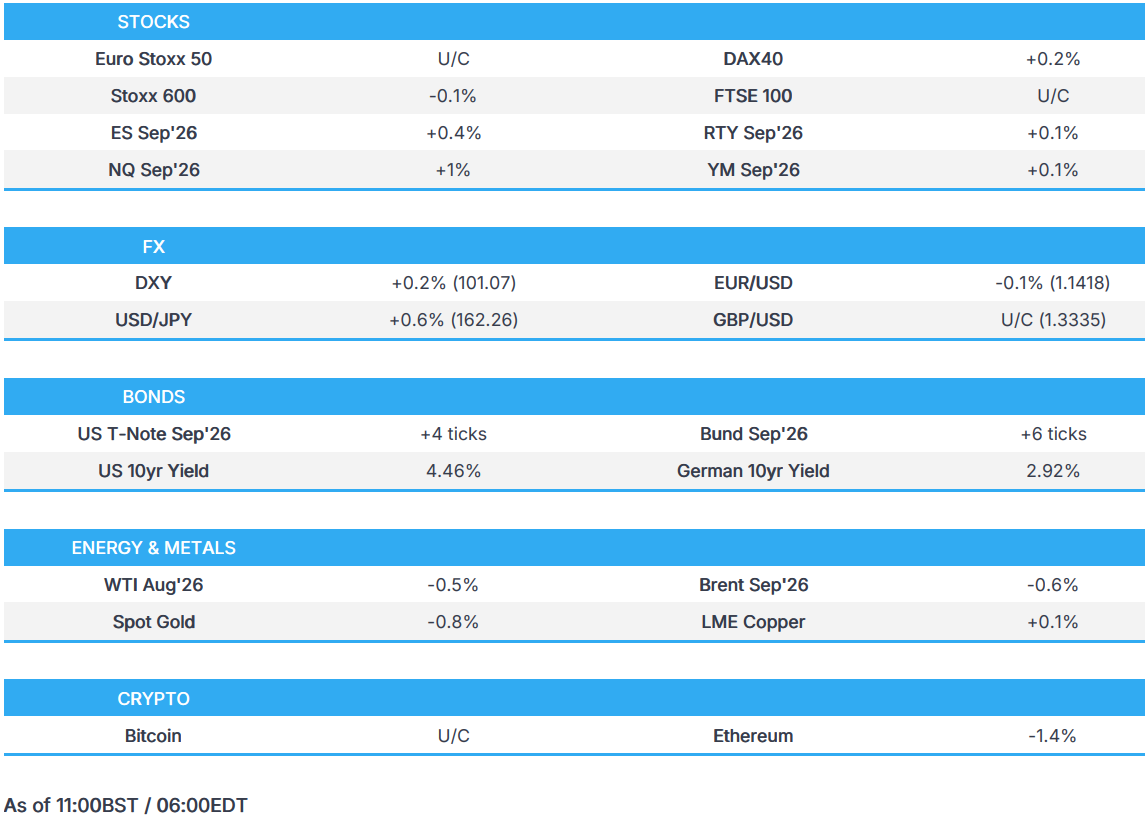

- European equity futures trade tentatively; US equity futures are indicative of a stronger open, NQ +1%.

- G10s are mostly lower against the USD. USD/JPY continues to rise, and sits back above the 162.30 mark.

- Fixed benchmarks trade with very mild gains, with USTs awaiting ISM Services.

- Looking ahead, highlights include US S&P Services/Composite PMI Final (Jun), and ISM Services PMI (Jun). Speakers include Fed's Waller, BoE's Mann, ECB's Schnabel, Lagarde and Lane.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.2%) have traded on either side of the unchanged mark throughout the morning, with a lack of pertinent catalysts driving the action.

- European sectors are mixed but with a positive bias. Leading the table is Media, helped by ITV (+1%), Travel and Leisure is helped by easyJet (+10%), while European tech underperforms after modest losses in APAC (ASML -1.5%, STMicroelectronics -1.5%). For easyJet, the co. agreed in principle to Castlelake’s fifth takeover bid, at GBP 6.90/shr in cash.

- Stateside, futures play catch-up after US stocks were closed on Friday for US Independence Day. NQ +1% outperforms after broad tech gains on Friday, ES +0.4%, and RTY +0.2% also green.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- Lack of macro catalysts with geopolitical news light as US-Iran negotiations pause for the former Supreme Leader’s funeral processions. The Buck today is seemingly attracting carry demand as we near summer trade, where ING notes G7 FX volatility is close to the lower end of long-term ranges. DXY currently trades near highs, within a 100.82 to 101.13 range.

- JPY is the clear underperformer, as it attempts to return to recent lows against most peers. Specifically, USD/JPY +0.5% on the day as the Buck outperforms against low yielders and after unconvincing potential intervention over the past week. USD/JPY sees its first resistance at 162.50 to the upside; thereafter, the next significant level is the 1st July high of 162.84.

- Antipodeans are mixed, Aussie outperforms as it attracts carry demand as mentioned above, while Kiwi is one of the G10 laggards as hawkish bets unwind ahead of the RBNZ policy announcement on Wednesday. Ahead of the meeting, the NZIER Shadow Board recommended that the RBNZ hold the OCR at 2.25%, against the market consensus of a 25bp hike to 2.50%. AUD/NZD +0.4% and approaches 1.2200.

- South Korean Finance Minister said the BoK is to closely monitor the impact and movements of KRW's 24-hour trade.

FIXED INCOME

- Global fixed benchmarks are mildly firmer this morning, taking leads from lower energy prices. Price action has been fairly lacklustre this morning, with the European session ultimately seeing sideways action.

- USTs (+4 ticks) are firmer this morning and hold within a 109-17 to 109-24 range; currently holding towards the upper end of the day’s range. US-specific newsflow has been lacking this morning, but will likely pick up in the form of US Final PMIs and then the more closely watched ISM Services thereafter. On that front, the headline is expected to pare to 54.0 (prev. 54.5), prices paid at 69.0 (prev. 71.3), and new orders at 57.0 (prev. 57.3).

- Bunds (+8 ticks) and Gilts (+5 ticks) both trade with mild gains, but with action ultimately non-committal. Both benchmarks are off their best levels and trading towards the mid-point of their respective 126.59-126.82 and 88.81-89.12 ranges.

- For Europe specifically, the EZ Sentix Investor Confidence topped expectations (-3.1 vs exp. -14.5), though not all too surprising given the recently signed US-Iran MoU. Sentix stated that “The slump in sentiment caused by the Iran conflict is slowly being overcome. The German government's latest reform efforts are having an impact”. On the data front, EZ PPI Y/Y printed a touch above the expected, as did Retail Sales – no move was seen on the data.

- BoJ announces its outright bond purchase operation in-line with its plan. Offers to buy JPY 100bln of <1yr JGBs. Offers to buy JPY 335bln of 5-10yr JGBs. Offers to buy JPY 100bln of 10-25yr JGBs.

COMMODITIES

- WTI Aug and Brent Sep futures are ultimately on a softer footing following choppy APAC and European morning trade. Macro catalysts remain quiet, further compounded by a temporary lull in geopolitical headlines, driving a steady unwinding of the war premium that supported prices throughout H1 2026. WTI resides towards the lower end of a USD 67.82-69.21/bbl range, while Brent sits at the bottom end of a USD 71.02-72.45/bbl parameter.

- Elsewhere, metals are mixed with precious metals softer after last week seeing its first weekly gain since May, supported by fading Fed rate hike expectations following the soft US jobs data, and lower energy prices. Meanwhile, overnight, it was reported that Hong Kong's pension fund will be able to invest in more gold ETFs as part of the government's push to make the city a gold trading hub, SCMP reports, citing sources. SCMP earlier reported that Hong Kong is to reportedly launch a gold clearing and settlement system.

- Price action this morning saw the yellow metal find resistance around the USD 4,200/oz mark, currently residing in a USD 4,144-4,202/oz range, with US traders set to return from their long weekend, and with ISM Services PMI ahead.

- In terms of base metals, copper futures are rising for a third consecutive session in a USD 13,361.53- 13,464.00/t range, whilst aluminium extends a rebound from a four-month low, supported by fading Fed rate hike bets after Fed Chair Warsh last week said price risks were easing.

- Goldman Sachs lowered its LME aluminium price forecast to USD 2,950/t for Q4 2026 and lowered its 2027 average forecast to USD 2,700/t. Goldman Sachs cuts its 2026 aluminium supply deficit forecast to 100k tonnes and raises its 2027 supply surplus forecast to about 1.5mln.

- Infrastructure has reportedly been damaged in the region of Russia's Ust-Luga and Vysotsk oil ports after a drone attack.

- UK ministers are reconsidering a ban on crop-based biofuels for aviation following a lobbying tour of the US Corn Belt by government officials, the FT reported.

- A power outage has been reported at Marathon Petroleum's (MPC) Detroit refinery, causing controlled gas burning, according to local media.

- Hong Kong's pension fund will be able to invest in more gold ETFs as part of the government's push to the city into a gold trading hub, SCMP reported citing sources.

- South Korean prosecutors say refiners colluded to hike prices despite ample oil reserves, Yonhap reported.

- A fleet of 10 Japan-related ships have reportedly left the Strait of Hormuz, shipping data shows.

- Israel's energy minister said Israel is launching a new competitive process to search for more natural gas in the country's economic waters.

NOTABLE EUROPEAN HEADLINES

- UK Defence Minister Jarvis told POLITICO he wants Burnham’s administration to lay out the full pathway to spending 3.5% of GDP on defense at the next spending review, due spring 2027.

NOTABLE EUROPEAN DATA RECAP

- EU PPI YoY (May) Y/Y 5.9% vs. Exp. 5.7% (Prev. 4.9%).

- EU Retail Sales MoM (May) M/M 0.2% vs. Exp. 0.2% (Prev. -0.4%).

- EU PPI MoM (May) M/M 0.2% vs. Exp. 0.2% (Prev. 0.6%).

- EU Retail Sales YoY (May) Y/Y 1.6% vs. Exp. 1.5% (Prev. 1%).

- EU S&P Global Construction PMI (Jun) 42.8 (Prev. 43.7).

- UK S&P Global Construction PMI (Jun) 38.4 vs. Exp. 40.1 (Prev. 38.2).

- UK New Car Sales YoY (Jun) Y/Y 11.4% (Prev. 7.1%).

- French S&P Global Construction PMI (Jun) 38.2 (Prev. 39.6).

- Italian S&P Global Construction PMI (Jun) 45.4 (Prev. 49.4).

- German S&P Global Construction PMI (Jun) 44.8 (Prev. 42.4).

- German Factory Orders MoM (May) M/M 1.9% vs. Exp. 1.2% (Prev. -3.8%).

NOTABLE EUROPEAN EQUITY HEADLINES

- France is said to have softened its stance of possible sale of SAMP/T air defence system (HO FP) to Turkey, according to sources.

- CVC's (CVC NA) sale of marina group D-Marin is said to be valued at EUR 1-1.5bln, FT reported, citing sources.

CENTRAL BANKS

- New Zealand NZIER Shadow Board recommends that the RBNZ holds the OCR at 2.25%.

- PBoC injected CNY 7bln via 7-day reverse repos with rate maintained at 1.40%.

- PBoC set USD/CNY mid-point at 6.8066 vs exp. 6.7850 (prev. 6.8047).

- Swiss Total Sight Deposits (w/e Jul 3) 479.2bln (prev. 474.4bln W/W), Domestic 440.9bln (prev. 440.6bln W/W).

NOTABLE US HEADLINES

- Goldman Sachs sees USD/JPY at 165.00 in a year's time, raising its forecast from 155.00, citing Japan's interest rate differentials with the US.

NOTABLE US EQUITY HEADLINES

- Honeywell (HON) spin-off Solstice Advanced Materials is said to be in talks to merge with Element Solutions which could create a USD 27bln chemicals giant, FT reported. Discussions are ongoing with a formal agreement not reached, but a deal could come together as soon as this week, sources told the FT.

GEOPOLITICS

RUSSIA-UKRAINE

- Ukraine's military said it has struck its oil refineries in Russia's Yaroslavl and Leningrad regions.

- EU's von der Leyen said EU is working to seal the 21st Russian sanctions package in the next days.

- Infrastructure has reportedly been damaged in the region of Russia's Ust-Luga and Vysotsk oil ports after a drone attack.

- Russian Defense Ministry said 519 Ukrainian drones were shot down over the regions overnight.

- A Ukrainian official said the death toll in Kyiv has risen to 9 after the recent Russian attacks.

- US President Trump is to meet with Ukrainian President Zelensky at the NATO summit in Ankara, Turkey.

- Kyiv Mayor said the city is under a Russian missile attack with one residence badly damaged.

- A Russian official said the Ukrainian attack cuts the electricity to Sevastopol in Crimea, AFP reported.

- Several Russian ballistic missiles have struck Kyiv, with explosions being heard, according to an FT reporter.

MIDDLE EAST

- Islamabad is the more likely option for the next round of US-Iran technical talks, with July 11th expected to be the date, sources tell Pakistani newspaper Dawn, according to Fox. Negotiations are expected to focus on Iran's nuclear programme, frozen Iranian assets, the Strait of Hormuz and the Lebanon ceasefire.

- Israeli Defence Minister Katz said any Iranian leader who tries again to promote plans to destroy Israel will be thwarted; Israel is prepared to defend itself again, with its own forces, at any time and against every threat.

- Iranian Parliament Speaker Ghalibaf said a ceasefire in Gaza will be part of the second phase of the agreement with the US.

- Iranian Parliamentary Speaker Ghalibaf said the US memorandum is 'difficult but possible' to enforce, Al Jazeera reported.

- The Israeli occupation army carries out a bombing operation in the town of Houla in southern Lebanon.

- Israeli Army Chief of Staff Zamir said that the Israeli army will continue its operations to eliminate threats from Lebanese soil.

- Israeli airstrikes hit multiple towns in southern Lebanon.

OTHERS

- UK's Burnham is said to back outgoing UK PM Starmer's Chagos island giveaway, Guido reported, citing sources.

- Japan's Chief Cabinet Secretary Kihara said there is no confirmation that a Chinese missile passed over Japan's EEZ, will respond calmly.

- Japanese Chief Cabinet Kihara said there are no reported of China's test-launched missile having caused damage to aircraft or ships.

- China's test-launched ballistic missiles outside Japan's EEZ, Kyodo reported citing sources.

- Chinese military conducts a test launch of submarine-launched missile.

- China is preparing to test fight a nuclear capable long range missile with a dummy warhead in South Pacific within the next 24 hours, according to Australian press.

CRYPTO

- Bitcoin is essentially flat and trades just shy of USD 63k, whilst Ethereum holds just short of USD 1.8k.

APAC TRADE

- Asia-Pac stocks initially started the session with broad gains but reversed as the session continued, with a busy week ahead, which includes Samsung Electronics' Q2 earnings and SK Hynix's US listing.

- ASX 200 managed to limit its downside, and only posted modest losses, as upside in Energy and Health Care broadly offset the downside seen in Consumer Staples and Mining names. Further on the mining topic, Genesis Minerals made a AUD 5.6bln bid for Vault Minerals, hijacking a deal previously made with Regis Resources.

- Nikkei 225 was softer as it continued to pull back from its ATH of 72,832. Kioxia was one of the big underperformers, after the Co. began shipping sample next-gen semiconductor products.

- KOSPI was under significant pressure, despite initially printing gains of as much as 2.9%, with Samsung set to report Q2 figures on Tuesday; operating profit expected to print at KRW 86tln. However, a miss would be detrimental to tech valuations, since doubts have crept in over the scale and durability of AI demand and capex.

- Shanghai Comp. traded either side of the unchanged mark while the Hang Seng posted decent gains. Alibaba found some comfort after a US federal judge ordered the Pentagon to give the Co. a reprieve from a lobbying ban tied to the Pentagon's curbs on Chinese companies.

NOTABLE ASIA-PAC HEADLINES

- Japanese PM Takaichi said domestic investment is lacking in economic growth and will achieve balance between the economy and sustainability.

- Japanese Chief Cabinet Secretary Kihara said they seek a strong economy for natural tax revenue growth.

- South Korean President Lee said administrative process must be sped up for chip clusters and power and water supply must be secured pre-emptively.

- China begins safety violation crackdown in key sectors including mining and chemicals, Xinhua reported.

- Anthropic is reportedly looking to acquire at least 1.4GW of capacity from data centres in Australia that will cost as much as USD 21.6bln, AFR reported.

NOTABLE APAC DATA RECAP

- Australian ANZ-Indeed Job Ads MoM (Jun) M/M -0.2% (Prev. 1.8%).

- Australian TD-MI Inflation Gauge MoM (Jun) M/M -0.4% (Prev. -0.3%); Y/Y 3.9% (Prev. 4.4%).

NOTABLE APAC EQUITY HEADLINES

- Apple (AAPL) supplier Luxshare (002475 CH) reportedly plans pricing its Hong Kong listing at the top end, Bloomberg reported.

- SK Hynix (000660 KS) is to raise KRW 43tln in ADR listing.

- Meituan's (3690 HK) LongCat-2.0 has been officially open-sourced, and domestic chip manufacturers are collectively adapting to it, Chinese press reported.

- Honda's (7267 JT) China unit reported June vehicles sales of 32.5k units, -44.5% Y/Y.

NOTABLE GLOBAL EQUITY HEADLINES

- United Microelectronics (UMC) (Jun) TWD: revenue 23.1bln (+22.9% Y/Y), YTD revenue 129.8bln (+11.3% Y/Y).

- Renault (RNO FP) CEO said Nissan (7201 JT) partnership is working "very well", open to partnerships with other European carmakers.

Loading...