US equity futures gain despite firmer energy benchmarks; Tesla, ServiceNow, IBM ahead - Newsquawk US Market Open

- US President Trump said the US have been asked to hold their attack on Iran until such time as its leaders and representatives can come up with a unified proposal.

- It was reported that Iran received 'some sign' the US is ready to break the blockade, spurring mild risk-on at the time.

- UKMTO reported two separate incidents near Oman and Iran, with the latter spurring upticks in the crude complex.

- European bourses opened higher but have since trundled lower, ASM International +8% after a strong Q1 and guidance; US equity futures gain.

- USD tracks oil prices, NZD repricing continues and Sterling unreactive to mostly in-line inflation data.

- Fixed income follows energy but is relatively contained thus far, Gilts marginally underperform.

- Looking ahead, highlights include EZ Consumer Confidence (Apr), CBRT Policy Announcement (Apr). Speakers include ECB’s Lagarde & Cipollone. Supply from US. Earnings from Vertiv, Boeing, GE Vernova, AT&T, Tesla, ServiceNow, IBM.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

IRAN CONFLICT

- UKMTO said it has received a report of an incident 8 nautical miles west of Iran; A master of an outbound cargo ship reported having been fired upon and is now stopped in the water, no reported damage.

- UKMTO said received information about an incident 15 nautical miles to the northeast of Oman in which a container vessel was approached by a single IRGC gunboat, while gunfire struck the vessel and severely damaged the bridge. said: There are no fires or environmental damage reported and the crew is safe.

- Pakistani Journalist Mallick posted "To my understanding, while there might be some roadblocks for the second round of US - Iran in person talks to go ahead, but Diplomacy is not dead and its currently at play.".

- US President Trump is reportedly willing to Iran give another three to five days of ceasefire, Axios reported citing sources; "It certainly looks like Trump doesn't want to use military force anymore and has made a decision to end the war,". US officials and Pakistani mediators are waiting for Khamenei to break his silence in the next day or two and give his negotiators a clear directive to return to the table. Ceasefire is not going to be open-ended, the source added.

- Iran received 'some sign' the US is ready to break the blockade, Tasnim reported.

- US President Trump posted "Iran is collapsing financially! They want the Strait of Hormuz opened immediately- Starving for cash! Losing 500 Million Dollars a day. Military and Police complaining that they are not getting paid. SOS!!!".

- Fox News cited sources that stated US President Trump's decision not to resume strikes on Iran for now is a last chance for peace that Trump is giving to the Iranian people, but added the ceasefire will be short-term unless an agreement is reached shortly.

- US President Trump posted "Iran doesn’t want the Strait of Hormuz closed, they want it open so they can make $500 Million Dollars a day (which is, therefore, what they are losing if it is closed!)". Full post "Iran doesn’t want the Strait of Hormuz closed, they want it open so they can make $500 Million Dollars a day (which is, therefore, what they are losing if it is closed!). They only say they want it closed because I have it totally BLOCKADED (CLOSED!), so they merely want to “save face.” People approached me four days ago, saying, “Sir, Iran wants to open up the Strait, immediately.” But if we do that, there can never be a Deal with Iran, unless we blow up the rest of their Country, their leaders included! President DONALD J. TRUMP".

- Iranian Parliament's National Security and Foreign Policy Commission member Khazarian said while Trump is announcing the end of the ceasefire unilaterally, at the same time he raised the maritime blockade, which is a ridiculous contradiction. said:. It means that both this is a military action and there is a silent war against Iran and expects that Iran will not respond and adhere to the ceasefire. This issue is not accepted by Iran.

- Iran top joint military command spokesperson said they are warning against repeated threats of the US President and army commanders, that their capable and the powerful forces have been 100% ready and on the trigger for a long time. said: In case of aggression and any action against Iran, they will immediately attack the predetermined targets and teach the aggressor, America and Israeli regime another lesson.

- Tasnim noted that continuation of naval blockade means continuation of hostilities, adds Iran will not reopen Strait of Hormuz until the maritime blockade continues and will break the blockade by force if necessary.

- Iranian TV states Iran will not recognize ceasefire announced by Trump and may not abide by it and will act in accordance with its national interests, according to Al Mayadeen.

- US blocks Iraq's dollar shipments to squeeze its Iran-backed militias and suspends security cooperation with Baghdad in an escalating pressure campaign, according to WSJ.

- Iran's Parliament Speaker Ghalibaf's Advisor said Trump's decision to extend the ceasefire makes no sense. The ceasefire extension is an attempt to buy time for a surprise attack. Iran currently holds the initiative.

- Pakistani PM is discussing with his ministers ways to persuade the Iranian side to return to the talks, Al Jazeera reported, citing sources.

- UK will host military planners from over 30 countries on Wednesday to develop a mission to reopen the Strait of Hormuz, according to The Times.

- US Secretary of State Rubio will join talks between Israel and Lebanon on Thursday.

EQUITIES

- European bourses opened with very mild gains, but have slowly trundled lower as the morning progressed, alongside a slight pick-up in the energy complex. From an index stand-point, the IBEX 35 (-0.4%) lags vs peers, whilst the AEX (+0.6%) outperforms, lifted by post-earnings strength in ASM International (+8.5%). In brief, the Co. reported strong Q1 results, driven by AI demand and resilient Chinese sales; the Co. also provided upbeat guidance.

- European sectors now display a mixed picture, after initially showing a positive bias. Unsurprisingly, Energy tops the pile given recent advances in the complex, followed closely by Basic Resources and Chemicals. Gains across underlying metals prices, alongside an upbeat update from Australia’s BHP has lifted sentiment across mining names – Fresnillo (+2%) also extends higher after a mixed production update. As for the Chemicals sector, Akzo Nobel (+5%) jumps after topping earnings forecasts, and lifting prices to counteract supply-side issues.

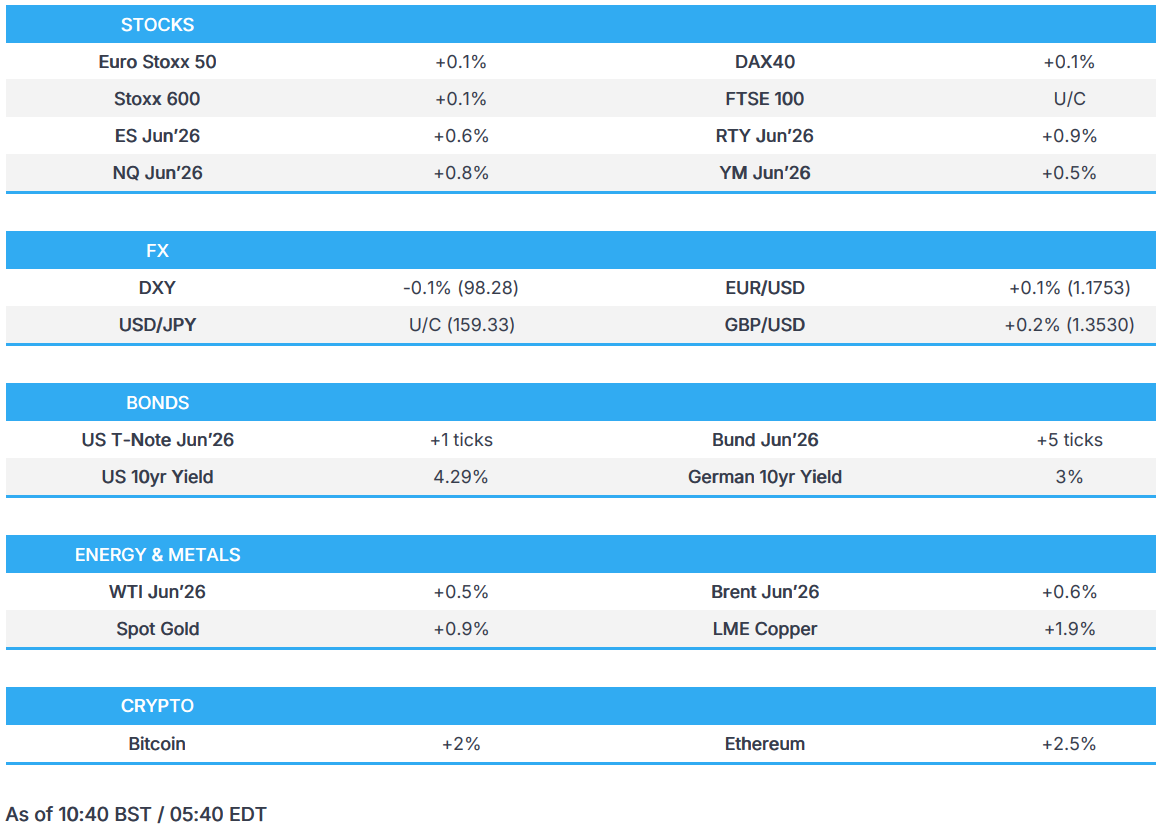

- US equity futures are broadly firmer across the board, in contrast to the bias seen in Europe; the RTY (+0.9%) mildly leads vs the NQ (+0.8%), ES (+0.6%). In terms of pre-market movers, Adobe (+2.5%) gains after announcing a USD 25bln stock buyback, whilst United Airlines (+1.8%) benefits post-earnings, where it Q1 results topped expectations, but cut guidance citing jet fuel price rises.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- FX trades mostly firmer vs the USD as oil prices chop either side of the unchanged mark following an extension of the US-Iran ceasefire.

- DXY trades lower by a tenth after being sold on a Bloomberg headline this morning, "Iran received 'some sign' the US is ready to break the blockade", desk looked into the headline and found it was likely in relation to comments made by the UN Ambassador Amir Saeid Iravani on Tuesday. It seems other desks were notified of this, which saw a modest and gradual reversal of the downward move. DXY lost steam at its 100 and 200 DMA (98.50) on Wednesday, and currently trades at 98.32.

- Kiwi outperforms once again amid continued rate repricing for the RBNZ. Markets are now expecting the OCR to be raised by 85bps by year-end, with the first cut fully priced for July, and around 50/50 for the May 27th meeting. AUD/NZD trickled lower overnight and into the European morning, currently -0.2% despite Aussie holding up well amid firmer gold prices. NOK is the only currency outperforming the bird today, helped by continued elevated oil prices, the scandi cross is higher by 0.7% and looks to 7th April highs of 0.9883.

- GBP modestly weakened on March inflation data, which was as expected at a headline level, while the core figures were cooler, but the all-important services lifted from the prior by more than expected. Overall, the BoE will likely be willing to wait and see for more data at this stage, as the lack of overt second-round effects means they have time to assess and weigh the growth vs inflation situation. GBP/USD is higher by a tenth of a percent and remains on a 1.35 handle. Overnight, Cable attempted a move below the aforementioned level but faltered at the 1.3503 mark. EUR/GBP trades a touch lower. At the time of writing, the cross attempts new lows near 0.8684.

FIXED INCOME

- A marginally bullish morning, at first at least, for fixed after relatively contained overnight trade. Modest upward impetus came after the Tasnim piece regarding the Hormuz blockade; though, it does appear to be a re-run of remarks from Tuesday.

- The complex has come under pressure after a UKMTO report around a cargo ship incident 8nm from Iran; reacting to the upside in energy. However, this pressure has since mostly pared, with the complex edging off worst levels and back towards the unchanged mark.

- USTs got to a 111-13 peak after that report, then gradually faded to unchanged and to a 111-07+ low thereafter, with losses of two ticks at most vs earlier gains of 4+. For the US, the main scheduled event is the 20yr auction. However, focus will undoubtedly be on any update to the geopolitical situation; see the morning's analysis piece for more.

- Gilts opened higher by 11 ticks, in line with the action in Bunds at the time. Thereafter, the benchmark climbed to a 88.08 peak with gains of 20 ticks at most. Upside also spurred in reaction to the morning's CPI series, with the headline as forecast and the core figure cooler-than-expected. However, the all-important services lifted by more than expected vs the prior; albeit, that itself is somewhat caveated by the early Easter, and may be partially unwound in April. Overall, for the BoE, they will likely be willing to wait and see for more data at this stage, as the lack of overt second-round effects means they have time to assess and weigh the growth vs inflation situation.

- Bunds in-fitting with the general move. Hit a 125.81 peak with gains of c. 15 ticks before moderating and fading alongside the latest energy uptick.

- Australia sold AUD 1bln 3.75% April 2037 bonds, b/c 3.63, avg. yield 4.9884%.

- Germany sold EUR 1.96bln vs exp. EUR 2bln 2.60% 2041 and 3.40% 2047 Bunds.

COMMODITIES

- In geopolitics, US President Trump said the US had been asked to hold its attack on Iran until Iranian leaders and representatives can come up with a unified proposal, and extended the ceasefire until such time as their proposal is submitted and discussions are concluded, one way or the other, while instructing the military to continue the blockade. Axios reported that Trump is willing to give Iran another three to five days of ceasefire, with one source saying it looks like Trump does not want to use military force anymore and has made a decision to end the war, while also stressing the ceasefire is not going to be open-ended. US-Iran talks remained in limbo, with VP Vance’s trip to Pakistan called off / postponed, Iran deciding not to attend Islamabad on Wednesday, and mediators still trying to get both sides back to the table. Iranian officials said the continuation of the naval blockade means continuation of hostilities, while warning that Tehran may not recognise or abide by the ceasefire under such conditions. In Hormuz, two separate reports were released by the UKMTO as Iran targets ships in the region.

- WTI and Brent futures are firmer as geopolitics remain the driving force, with uncertainty continuing to weigh on the supply side of the equation alongside reports of attacks on ships in the region. WTI resides towards the top end of a USD 87.64-91.41/bbl range, while its Brent counterpart trades in a USD 96.54-100.39/bbl parameter. Dutch TTF also trades modestly firmer north of EUR 42/MWh but well-off war-peaks.

- Precious metals are firmer as the DXY takes a breather from yesterday’s rise. Spot gold yesterday dipped under its 100 DMA (USD 4,730/oz) to a USD 4,668.62/oz low before trimming losses and rising back above the 100 DMA and to levels around USD 4,750/oz (USD 4,715-4,772/oz). Spot silver this morning found resistance at its 100 DMA (USD 78.68/oz), with the metal currently in a USD 76.70-78.68/oz band at the time of writing.

- Base metals are mostly firmer across the board to varying degrees, with a softer dollar underpinning price action for now, alongside some relief following Trump's ceasefire extension, despite the breakdown of talks. 3M LME copper resides in a USD 13,213.33-13,335.00/t range at the time of writing.

- US Private Energy Inventories (bbls): Crude -4.5mln (exp -1.8mln), Distillate -4.6mln (exp. -2.5mln), Gasoline -5.2mln (exp. -1.3mln), Cushing +0.7mln.

- Japan has reportedly agreed to import 1mln bbls of crude oil from Mexico, due to arrive in July, Nikkei reported. Comes as Japan seeks to reduce reliance on the Middle East after supply concerns linked to the de facto closure of the Strait of Hormuz. Japan and Mexico leaders also discussed broader energy and economic security cooperation, including critical minerals and supply chains.

- Fire reported at an oil refinery in Erbil, Iraq, Al Hadath reported.

- Slovak Economy Minister said Druzhba flows via Ukraine to Slovakia expected to restart on Thursday morning.

- Fujairah, UAE crude inventory at 7.45mln barrels, a five-year low.

- Hungary's MOL said it received notice from Ukrtransnafta of its readiness to resume oil deliveries via Druzhba, TASS reported.

- Hungarian officials have told Politico that a decision on the EU loan to Ukraine is dependent on actual flows through the Druzhba pipeline.

- Kazakhstan Energy Minister said that they do not intend to reduce oil output following the suspension of exports to Germany.

- European Commission will unveil a package of measures today aimed at offsetting surging energy prices, according to Reuters.

- US President Trump considers extending waivers to ease US oil shipments, according to Axios.

- Ukraine is to resume Druzhba oil supplies on Wednesday afternoon.

- US President Trump posted "My Administration just delivered a BIG WIN for the Great Commonwealth of Pennsylvania... Commerce Department worked with Governor Josh Shapiro, who has now agreed to keep open TWO BEAUTIFUL, CLEAN COAL PLANTS". Full post: "My Administration just delivered a BIG WIN for the Great Commonwealth of Pennsylvania, which I love, and WON by the largest margin in History. Based on this, the Commerce Department worked with Governor Josh Shapiro, who has now agreed to keep open TWO BEAUTIFUL, CLEAN COAL PLANTS in Indiana and Armstrong Counties. Radical Left Lunatics wanted to get rid of these wonderful Plants in favor of WIND FARMS, which kill the birds, and are both costly and ineffective. We will never allow that to happen! Thankfully, we struck a deal to guarantee these Plants will not be “retired.” I WILL ALWAYS FIGHT FOR THE FANTASTIC PEOPLE OF PENNSYLVANIA! President DONALD J. TRUMP".

TRADE/TARIFFS

- USTR Greer called for US allies to pay more for critical minerals and said a ‘security premium’ needed to counter reliance on Chinese supplies, according to FT.

NOTABLE EUROPEAN HEADLINES

- POLITICO said no resignation watch rumours are yet circulating in Westminster DMs, referring to UK PM Starmer. Chancellor Reeves publicly backed the PM at last night’s Good Growth Foundation reception, POLITICO reported.

- UK pension funds were warned they face large costs if they attempt to offload private market assets, following a warning by the industry regulator about some schemes’ high exposure to hard-to-sell investments, according to FT.

NOTABLE EUROPEAN DATA RECAP

- UK Inflation Rate YoY (Mar) Y/Y 3.3% vs. Exp. 3.3% (Prev. 3%, Low. 3.1%, High. 3.5%).

- UK Inflation Rate MoM (Mar) M/M 0.7% vs. Exp. 0.6% (Prev. 0.4%, Low. 0.5%, High. 0.8%).

- UK Core Inflation Rate MoM (Mar) M/M 0.4% vs. Exp. 0.5% (Prev. 0.6%, Low. 0.3%, High. 0.6%).

- UK Core Inflation Rate YoY (Mar) Y/Y 3.1% vs. Exp. 3.2% (Prev. 3.2%, Low. 2.9%, High. 3.3%).

- UK Services Inflation Y/Y (Mar) 4.5% vs. Exp. 4.40% (Prev. 4.30%).

- UK PPI Output YoY (Mar) Y/Y 2.6% (Prev. 1.7%).

- UK PPI Input MoM (Mar) M/M 4.4% (Prev. 0.8%).

- UK PPI Input YoY (Mar) Y/Y 5.4% (Prev. 0.5%).

- UK PPI Core Output YoY (Mar) Y/Y 2.0% (Prev. 1.9%).

- UK PPI Core Output MoM (Mar) M/M 0.2% (Prev. -0.8%).

- UK PPI Output MoM (Mar) M/M 0.9% (Prev. -0.5%).

- UK Retail Price Index YoY (Mar) Y/Y 4.1% vs. Exp. 3.9% (Prev. 3.6%).

- UK Retail Price Index MoM (Mar) M/M 0.8% vs. Exp. 0.7%.

- South African Core Inflation Rate YoY (Mar) Y/Y 3.2% (Prev. 3%).

- South African Core Inflation Rate MoM (Mar) M/M 0.8% (Prev. 0.7%).

- South African Inflation Rate MoM (Mar) M/M 0.6% (Prev. 0.4%).

- South African Inflation Rate YoY (Mar) Y/Y 3.1% (Prev. 3%).

CENTRAL BANKS

- ECB's Lane said countries could decide to finance investment in European-wide public goods through more common debt.

- ECB's Kazaks said the central bank has the “luxury” of not needing to rush to raise interest rates and he sees no rush to respond to higher energy prices driven by Iran war, according to FT.

- BoE's Breeden said private credit liquidity risk threatens stability.

NOTABLE US HEADLINES

- US Senate voted 52-46 to advance GOP budget bill for ICE and Border Patrol, according to NBC.

GEOPOLITICS

RUSSIA-UKRAINE

- Slovak Economy Minister said Druzhba flows via Ukraine to Slovakia expected to restart on Thursday morning.

- Ukraine's Foreign Minister said they want a meeting between President Zelensky and Russian President Putin, have made enquiries to see if Turkey could host this.

- Hungarian officials have told Politico that a decision on the EU loan to Ukraine is dependent on actual flows through the Druzhba pipeline.

- Ukraine is to resume Druzhba oil supplies on Wednesday afternoon.

CRYPTO

- Bitcoin is a little firmer and trades just above USD 78k, with Ethereum outperforming a touch and approaches USD 2.4k.

APAC TRADE

- APAC stocks traded mixed as participants reflected on the latest geopolitical developments, including the collapse of peace talks in Islamabad, while US President Trump announced an extension of the ceasefire until discussions conclude, but will maintain the naval blockade in Hormuz

- ASX 200 declined with the index dragged lower by underperformance in health care and the top-weighted financial industry, while the mining sector was rangebound despite gains in BHP following its quarterly production update.

- Nikkei 225 initially clawed back losses and printed a fresh record high with some encouragement from stronger-than-expected Exports and Imports data from Japan, while recent source reports continued to point to the central bank refraining from hiking rates next week.

- Hang Seng and Shanghai Comp were mixed with the Hong Kong benchmark the underperformer, as tech weakness clouded over the strength seen in the Chinese oil majors, while the mainland was kept afloat in rangebound trade with very few fresh China-specific catalysts.

NOTABLE APAC DATA RECAP

- Australian Westpac Leading Index MM (Mar) -0.1% (Prev. -0.1%).

- Japanese Imports YoY (Mar) Y/Y 10.9% vs. Exp. 7.1% (Prev. 10.2%, Low. 3.8%, High. 10.1%).

- Japanese Exports YoY (Mar) Y/Y 11.7% vs. Exp. 11% (Prev. 4.2%, Low. 6.4%, High. 14.2%).

- Japanese Balance of Trade (Mar) 667.0B vs. Exp. 1106B (Prev. 57.3B, Low. 700B, High. 5306B).

- Korea (Republic of) PPI MoM (Mar) M/M 1.6% (Prev. 0.6%).

Loading...