US equity futures gain, DXY flat whilst the AUD lags post-RBA; US ISM Services ahead - Newsquawk US Market Open

- US President Trump said the war could go on for another two to three weeks; time is not of the essence.

- US officials say the military is closer to resuming combat operations than 24 hours ago, Fox reported.

- Iranian Foreign Minister Araghchi posted, "As talks are making progress with Pakistan's gracious effort, the US should be wary of being dragged back into a quagmire by ill-wishers. So should the UAE."

- European and US equity futures are broadly firmer; Palantir -2% as commercial revenue fell short of expectations.

- DXY is flat, JPY experiences volatile two-way action, AUD pressured post-RBA, where it hiked by 25bps, statement was net-hawkish, but Governor Bullock suggests there is room now to wait and see.

- Gilts gap lower on return from a Bank Holiday, USTs and Bunds relatively contained.

- Crude pares Monday's gains, to the benefit of XAU.

- Looking ahead, highlights include US Building Permits Final (Mar), Canadian Balance of Trade (Mar), Canadian PMI (Apr), US PMI Final (Apr), US ISM Services (Apr), US JOLTS (Mar), US New Home Sales (Mar), US RCM/TIPP Economic Optimism (May), New Zealand Unemployment Rate (Q1). Speakers include ECB’s Lagarde, Lane, Fed's Bowman, Barr. Supply from Germany. Earnings from AMD, AMC, Strategy, Tempus AI, Shopify, PayPal, Pfizer.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRANIAN CONFLICT

US

- US President Trump said Iran war could go on for another two to three weeks; time is not of the essence.

- US intelligence suggests strikes from the start of the war led to limited new damage to Iran's nuclear programme, Reuters sources say.

- US State Department official to Al Jazeera said the President is clear that direct communication between Israel and Lebanon is the best path toward peace; We are working to prepare the necessary conditions and political momentum to move forward with this

- Two US Navy destroyers transited the Strait of Hormuz and entered the Persian Gulf after navigating an Iranian barrage, according to defense officials who spoke to CBS News; "Iran launched small boats, missiles and drones against them".

- Maersk (MAERSKB DC) said its subsidiary's US-flagged vehicle carrier, Alliance Fairfax, exited the Gulf via Strait of Hormuz on May 4th.

- US Treasury Secretary Bessent had a "fierce row" with UK Chancellor Reeves last month over her outspoken criticism of the Iranian war, FT sources say.

- US CENTCOM posted "US warships and aircraft deployed to the Middle East are enforcing the naval blockade against Iran while executing Project Freedom to support the free flow of commerce through the Strait of Hormuz.".

- US officials say military closer to resuming combat operations than 24 hours ago, Fox reported.

- US President Trump reiterates he feels Europe has been "very disappointing".

IRAN

- Iranian Foreign Minister Araghchi posted "As talks are making progress with Pakistan's gracious effort, the US should be wary of being dragged back into quagmire by ill-wishers. So should the UAE.". Full post:"Events in Hormuz make clear that there's no military solution to a political crisis. As talks are making progress with Pakistan's gracious effort, the U.S. should be wary of being dragged back into quagmire by ill-wishers. So should the UAE.Project Freedom is Project Deadlock.".

- IRGC military source told Tasnim that the US shot two small boats carrying civilians instead of shooting IRGC speedboats.

- "Iranian Defense Council member Ali Akbar Ahmadian: Our security does not accept negotiations, and Washington obstructed global navigation and energy security", Al Jazeera reported.

- Iranian President Pezeshkian has requested an immediate and emergency meeting with Supreme Leader Khamenei to ask him to stop IRGC attacks on Persian Gulf nations and prevent a recurrence, Iran International reported. Pezeshkian reportedly outlined that the IRGC attack on the UAE occurred without the knowledge of the government.

- Mehr News Agency said a fire broke out in two commercial ships and spread to two others in Dayyer port south of Iran; cause not clear.

- "Explosions were heard tonight in the port of Bandar Abbas (Iran) and on Qassem Island (Iran) in the Persian Gulf", N12 journalist reported citing sources in Iran.

- IRGC political deputy said traffic in the Strait of Hormuz will only be done with Iran's permission, ISNA reported; "Any kind of traffic in the Strait of Hormuz, if it is from the enemy, will be met with a decisive and crushing response".

- Iranian Parliamentary Speaker Ghalibaf said the new equation of the Strait of Hormuz is being solidified. Actions of the US and allies have threatened the security of shipping and energy.

- UNSC resolution prepared by the US, Saudi Arabia, Bahrain, Qatar, the UAE, and Kuwait opens the door for potential enforcement measures, AsharqNews reported citing the resolution "to be distributed tomorrow".

EUROPEAN TRADE

EQUITIES

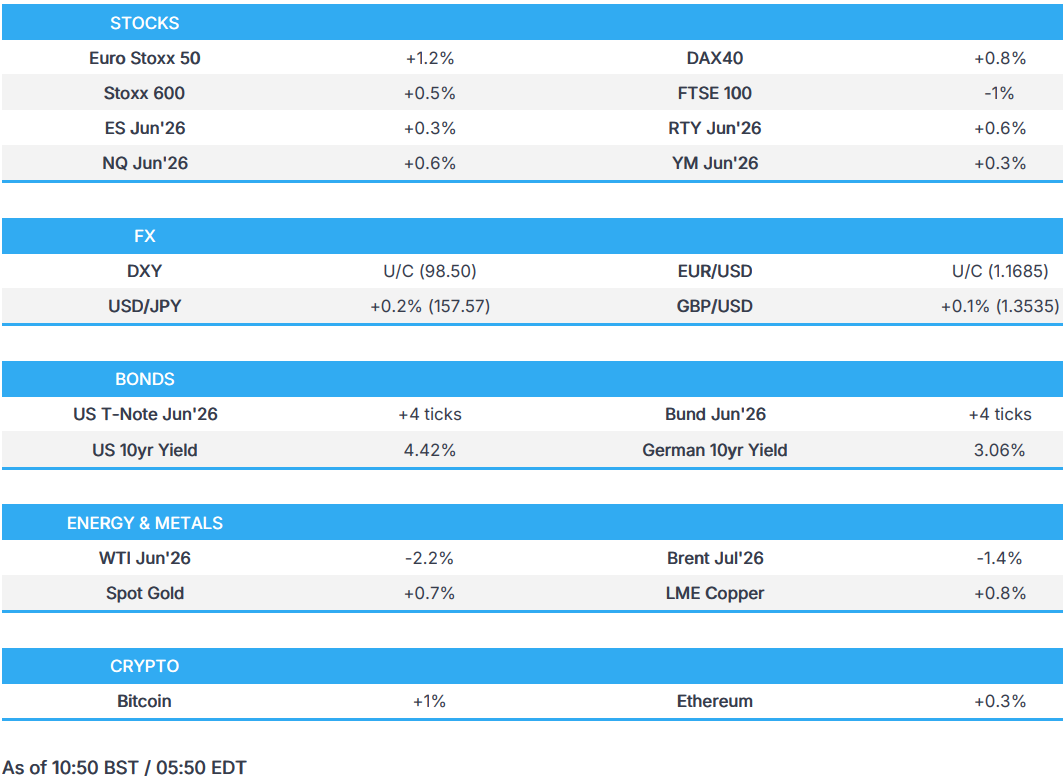

- European bourses opened mixed, but now display a clear positive bias alongside a move lower in crude prices this morning. The Euro Stoxx 50 (+0.9%) is the top performing index, whilst the FTSE 100 (-1%) is the clear laggard, as it returns from holiday and digests the recent US-Iran escalation.

- European sectors hold a positive bias this morning. Construction tops the pile, buoyed by post-earning strength in Geberit (+1.7%, robust results and sees strong demand across several markets). Chemicals and Financial Services complete the top three. To the downside reside Basic Resources and then Banks. The latter has been dragged down by losses in HSBC (-5%), after the Co. reported a Q1 profit miss and estimates higher than expected credit losses. Gains in UniCredit (+3%) are failing to lift the sector, with the Italian bank reporting strong profit and robust investment income.

- US equity futures are in the green this morning, and attempting to pare back some of the modest weakness seen in the prior session. Fed speak today includes Barr and Bowman. As for key movers today, Palantir (-2%, stronger results and lifted guidance, but US commercial revenue fell short of expectations). Elsewhere, ON Semiconductor (-4.7%, strong results, though missed on lofty expectations).

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is steady and trades within a narrow 98.40 to 98.57 range, with geopolitical newsflow overnight relatively light and as markets await the US data docket later. The index currently trades in close proximity to its 21-DMA (98.50), 100-DMA (98.46) and 200-DMA (98.55). No doubt attention ahead will be on any geopolitical developments, but domestically, traders will also eye US ISM Services, PMI Finals, JOLTS and a couple of Fed speakers.

- Antipodeans are diverging this morning, with the Kiwi marginally topping the G10 pile whilst the Aussie lags. This is largely a function of a weaker AUD, after the RBA’s decision to hike its policy rate by 25bps (as expected). The accompanying statement was also net-hawkish, having suggested that second-round effects are beginning to emerge. In an immediate reaction, AUD/USD jumped higher to make a session peak at 0.7171 (vs trough 0.7135), before then gradually trundling lower soon after. The move lower is potentially a function of traders now taking out bets of future tightening, after three consecutive hikes. Particularly as in the presser, the Governor outlined they now have the policy space to wait and see. Markets currently do not assign much probability to a hike in June, before fully pricing in a hike by September.

- JPY was flat for much of the European morning, but is now a touch lower after a recent spike higher in USD/JPY - a move which lacked a fundamental driver. The pair jumped to form a session high at 157.88 (from 157.28), before then immediately paring back towards 157.47. Most recently, a knee jerk lower was seen in the pair, with an aggressive move lower from 157.56 to 157.12, before once again moving back towards 157.50.

- CHF is near enough unchanged vs the USD, and incrementally firmer against the EUR; EUR/CHF currently hovers just above its 50-DMA at 0.91554. Some modest pressure was seen in the Swiss Franc after the region’s April inflation report, whereby the M/M metric increased by less than expected, though the Y/Y figure doubled amidst the Iranian war.

FIXED INCOME

- A contained morning for USTs and Bunds given ongoing APAC holidays and after the significant bearish action seen on Monday amid energy upside of as much as USD 6/bbl in Brent.

- Gilts, unsurprisingly, lag with downside of 84 ticks at most to an 86.19 base, taking out the 86.36 low from Friday and now looking to the figure and then the 85.90 contract trough. Underperformance is a function of Gilts playing catch-up after Monday's holiday, similar action seen in the FTSE 100. Otherwise, the UK docket is light, and the benchmark will likely conform directionally to peers, and as such may well retrace some of the discussed downside, in a similar fashion to peers late-Monday.

- For the UK, we continue to count down to Thursday's local elections, the results of which could be the tipping point against PM Starmer, particularly if his own council (Camden) shifts against Labour as the latest polls indicate it might, in a pivot to The Greens. On the leadership, The Times reports that Labour MPs are discussing plans to demand Starmer set a resignation date, in a move akin to that taken by allies of Brown against Blair.

- USTs are currently a few ticks firmer in 110-05+ to 110-12 parameters, at the lower end of Monday's 110-00+ to 110-26+ band. Ahead, a number of data points of note alongside remarks from Fed's Bowman and Barr. However, there is every chance that action is once again dominated by geopolitics.

- Bunds are a few ticks lower in a narrow 124.85 to 125.03 band, similarly at the lower end of Monday's 124.68 to 125.51 confines. Specifics for the bloc light thus far, though we do look to a text release from ECB's Lane; however, the topic is focused on the climate, rather than monetary policy.

- Alphabet (GOOGL) commences a six-part EUR-denominated bond offer.

- Germany sells EUR 0.993bln vs exp. EUR 1.0bln 2.10% 2029 and EUR 0.483bln vs exp. EUR 0.5bln 2.50% 2035 Green Bunds.

COMMODITIES

- Crude in the red, as energy generally eases off the highs printed on Monday, where Brent briefly posted gains in excess of USD 6/bbl at a USD 115.30/bbl peak, a conflict high for the July contract. As it stands, Brent is below USD 113.00/bbl, but remains markedly clear of the week's USD 106.60/bbl open.

- Overnight, specifics were bullish for energy, but the magnitude of Monday's move meant the space failed to benefit. In brief, US President Trump said the conflict could continue for another three weeks, and time is not of the essence. Furthermore, a Fox report suggests the US is closer to resuming combat activity vs 24hrs prior. From the Iranian side, reports around recent strikes and who knew in advance point to ongoing or even further fractures within the leadership.

- Dutch TTF in-fitting, lower and holding around EUR 47.70/MWh vs a EUR 49.23/MWh peak on Monday; however, this left it markedly shy of recent levels, which run as high as EUR 73.41/MWh

- Spot gold firmer, benefitting from lower energy prices and the respite it has provided to the USD. XAU peaked at USD 4558/oz just after the European cash equity open and remains in proximity to its best levels. Ahead, Fed speak, and US data dominate from a scheduled perspective.

- Base metals firmer on the return of LME, following the broader risk tone, though with mainland China still away, the magnitude is limited thus far. 3M LME Copper firmer and back above USD 13k.

- Glencore (GLEN LN) confirms that an incident occurred earlier today at the zinc smelting unit of the Ust-Kamenogorsk Metallurgical Complex.

- Iraq is offering term buyers discounts of USD 33.40/bbl on Basrah Medium for May loading, Bloomberg reported citing a 3rd of May notice.

TRADE/TARIFFS

- EU sounds out industry over new trade weapon against China’s overcapacity, SCMP reported.

- US President Trump said he has a very good relationship with Chinese President Xi.

- US President Trump said hate to have to pay tariffs back.

NOTABLE EUROPEAN DATA RECAP

- Swiss Inflation Rate YoY (Apr) Y/Y 0.6% vs. Exp. 0.6% (Prev. 0.3%, Low. 0.2%, High. 0.4%).

- Swiss Inflation Rate MoM (Apr) M/M 0.3% vs. Exp. 0.4% (Prev. 0.2%, Low. 0.2%, High. 0.7%).

- Spanish Unemployment Change (Apr) -62.7K vs. Exp. -18.6K (Prev. -22.9K).

CENTRAL BANKS

- RBA hikes its Cash Rate by 25bps as expected to 4.35%; via 8-1 vote (one voted to maintain rate at 4.10%); said inflation likely to remain above the target and risks remain tilted to the upside. DECISION. Board assessed that inflation is likely to remain above target for some time and that the risks remain tilted to the upside, including to inflation expectations. It was therefore judged appropriate to increase the cash rate target. The Board will be attentive to the data and the evolving assessment of the outlook and risks to guide its decisions. Having raised the cash rate three times, monetary policy is well placed to respond to developments. It will do what it considers necessary to achieve that outcome. INFLATION. Inflation picked up materially in the second half of 2025, and information since the beginning of this year confirms that some of this increase reflected greater capacity pressures. There are early signs that many firms experiencing cost pressures are looking to increase prices of their goods and services. Short-term measures of inflation expectations have also risen. There are plausible scenarios where inflation is higher and activity lower than envisaged under the baseline forecast. MIDDLE EAST. A longer or more severe conflict could put further upward pressure on global energy prices; this would push up near-term inflation and could also increase inflation further out as these costs are passed through and if price rises get built into longer term inflation expectations.

- RBA Governor said if second round effects move through to expectations it could result in a need for higher rates. Current cash rate is a "bit" restrictive, provides some space to see how the Middle East situation develops. Have the policy space to wait and see. Extensive debate about the decision to hike.

CRYPTO

- Bitcoin is a little firmer this morning and trades around USD 80k, whilst Ethereum holds steady around the USD 2.4k mark.

APAC TRADE

- APAC stocks traded lower following a weak Wall Street lead, with liquidity thin amid widespread market holidays across Japan, South Korea, and Mainland China.

- ASX 200 was pressured by weakness in the metals sector, while Westpac declined after a miss in H1 net income. Focus also turned to the RBA, which delivered its third consecutive 25bps rate hike as expected.

- Hang Seng followed the negative tone, led lower by tech, while mainland markets remained shut, and Stock Connect flows were absent.

NOTABLE APAC DATA RECAP

- Australian Household Spending YoY (Mar) Y/Y 6.3% (Prev. 4.6%).

- Australian Household Spending MoM (Mar) M/M 1.6% (Prev. 0.3%).

- Australian S&P Global Composite PMI Final (Apr) 50.40 vs. Exp. 50.10 (Prev. 46.6).

- Australian S&P Global Services PMI Final (Apr) 50.7 vs. Exp. 50.3 (Prev. 46.3).

NOTABLE APAC EQUITY HEADLINES

- Foxconn (2317 TW) April (TWD): Revenue 832bln, +29.7% Y/Y. Q2 is expected to show both Q/Q and Y/Y growth.

Loading...