US equity futures little moved despite lack of US-Iran progress - Newsquawk Daily US Opening News

- US President Trump rejected Iran's response to the peace plan, which he called totally unacceptable.

- Iran's proposal was said to have stressed the need for the US to pay compensation for war damages and emphasised Iran’s sovereignty over the Strait of Hormuz.

- Brent initially climbed above USD 105/bbl but has waned off highs on potential diplomacy.

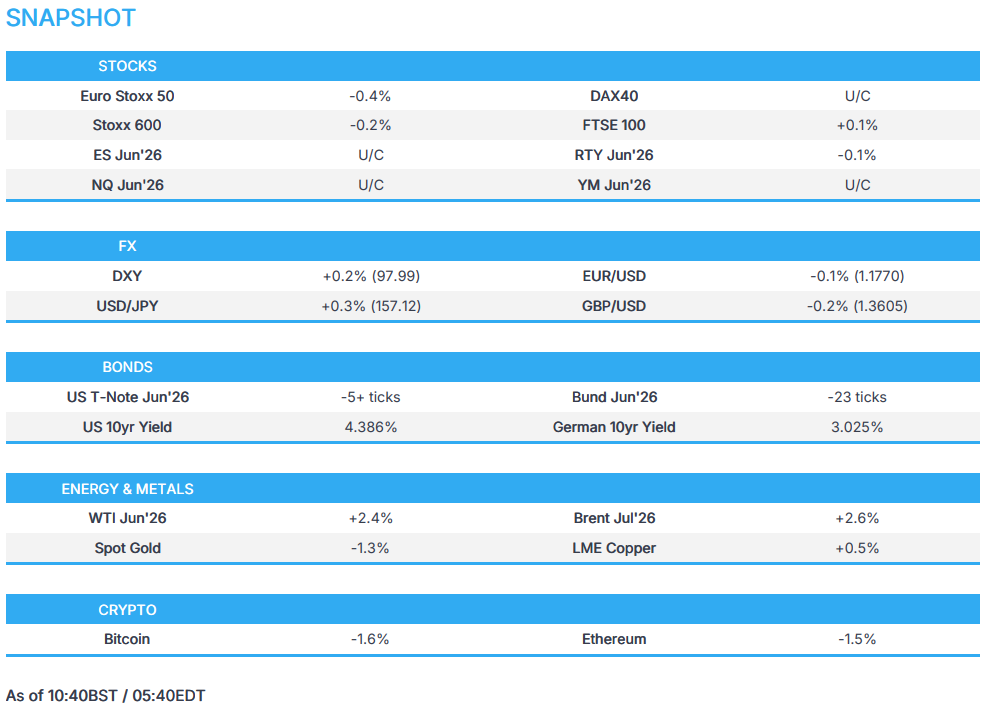

- European bourses traded mixed, Compass raised its FY guidance; US equity futures muted.

- DXY benefited from higher energy prices, CHF underperforms while GBP is cautious as PM Starmer addresses the nation.

- USTs and Bunds off worst levels as energy benchmarks dip from overnight highs.

- Looking ahead, highlights include US Existing Home Sales, BoC Market Participants Survey. Supply from the US. Earnings from Hims & Hers, Constellation Energy & Circle Internet.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 day

IRAN CONFLICT

- US President Trump posted, “I have just read the response from Iran’s so-called “Representatives.” I don’t like it — TOTALLY UNACCEPTABLE!”

- Iran submitted its response to the latest proposal by the US to end the war, according to the Islamic Republic News Agency, while Tehran hasn’t provided any public indication yet on whether it will accept US President Trump’s proposal for Iran to permit passage through the Strait of Hormuz and for the US to end its blockade on Iranian ports in the next month. Iranian state media later reported that the US proposal amounted to Iran surrendering to Trump’s excessive demands, while Iran’s proposal stressed the need for the US to pay compensation for war damages and emphasised Iran’s sovereignty over the Strait of Hormuz.

- Iran reportedly was offering a shorter uranium enrichment suspension than the 20-year US proposal and rejected dismantling its nuclear facilities in any future talks with the US, according to WSJ.

- US lawmakers are considering a potential congressional authorisation for military action if the US-Iran ceasefire ends, according to Semafor.

- "Diplomacy and back channel talks and contacts between Iran and US to work out a draft agreement continues to be in the works -- Diplomacy is not dead", Journalist Mallick posted.

- US officials cited by Iran International said Iran's response to the US proposal has blocked the path to a diplomatic solution with Tehran; "The next steps by Trump after receiving Iran's negative response are still unclear".

- Iran’s Foreign Ministry spokesperson Baghaei said Iran’s proposal to the US “was not excessive,” and that the US continues to have “unreasonable demands.”. He further stated that "currently, we are focusing our discussions on ending the war and the uranium issue, which we will discuss later."

- Tehran reiterates "its main condition for the ceasefire is the cessation of conflicts on all fronts, from Gaza and Lebanon to Yemen", Mehr reported.

- Iranian source told Tasnim "We saw the reaction of the US president to the Iranian answer. It is of no importance. No one in Iran drafts proposals to please Trump. The negotiating team writes proposals only for the rights of the Iranian people...".

- Iranian media reported overnight that air defence systems in the southwest of the country shot down an enemy reconnaissance drone, Israeli N12 reported.

- Israeli PM Netanyahu said removal of Iranian nuclear material remains a war priority and that US President Trump told him 'I want to go in' regarding Iranian nuclear sites.

- Israeli PM Netanyahu is holding security consultations following Iran’s response to the US proposal.

- Two interceptors were launched from Kiryat Shmona area to southern Lebanon following the identification of a suspicious aerial target, according to N12.

- Hezbollah said it targeted Israeli force stationed inside a house in Baidar al-Faqaani in the town of Taybeh for the second time. Israeli media said officers in Northern Command reveal an increase in Hezbollah attacks without the public being informed about them.

- WSJ writes that as US President Trump prepares to meet with Chinese President Xi Jinping in Beijing this week, the ongoing US-Israel war against Iran and the closure of the Strait of Hormuz is expected to dominate discussions.

- UK and France will host a meeting on Tuesday with the presence of defence ministers of dozens of countries to discuss the situation in the Strait of Hormuz.

- Three tankers carrying 6mln barrels of oil exited the Strait of Hormuz, Sky News reported citing new data.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.2%) trade mixed to start the week, despite the surge in energy prices. Over the weekend, US President Trump rejected Iran’s response to the peace plan and called it totally unacceptable. The FTSE 100 outperforms its peers while the CAC 40 lags.

- Sectors point to a mixed picture. Telecoms top the sector pile, followed by Banks amid the higher yield environment. Consumer Products & Services underperforms, with luxury names such as LVMH, Hermes and Kering falling by various degrees (0.8-2.5%).

- US equity futures are indicative of a flat open. For the tech-heavy NQ, it trades with modest losses on the day and YTD gains of 14%. Despite the impressive gains, it pales in comparison to the YTD KOSPI strength of over 80%.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- Snapshot: G10s are mostly lower against the USD, with action dictated by the strength seen across the energy complex; the CHF and JPY lag whilst the Loonie holds afloat. The NOK is a touch stronger this morning, following an uptick in the region’s core inflation.

- DXY is slightly firmer this morning, and trades towards the lower end of a 97.96-98.15 range. The index has been lifted by renewed geopolitical risk, after President Trump called Iran’s latest peace offer as “totally unacceptable” – as such, the crude complex is bid this morning. Domestically, tier 1 data is lacking this morning, but attention will turn to US CPI on Tuesday. Fed speak today includes Kashkari and Hammack (both dissenters at the April confab). ING opines that continued geopolitical unrest this week could see the index traverse back above the 98.00 mark, and trade within a 98.00-98.50 range.

- JPY and CHF are underperforming this morning, driven lower by their net-importer of energy statuses. For the USD/JPY specifically, it trades back towards the 157.00 mark, within a 156.55-157.17 range; further upside could see the pair head back towards its 100-DMA at 157.38. Domestic updates have been lacking for the JPY, but focus will be on US Treasury Secretary Bessent’s meeting with Japanese officials early this week.

- GBP is currently incrementally lower. PM Starmer remains on the wires at the time of publication; comments thus far remains very much as expected, where he reiterated that he will not step down. Markets await commentary from Catherine West, who has threatened a leadership challenge against Starmer, if she was left unsatisfied by his remarks. MUFG writes, “we continue to believe that a shift to the left for the Labour party would trigger at least a temporary period of pound selling”. Cable currently trades just above the 1.3600 mark, within a 1.3557-1.3614 range.

- Antipodeans are currently diverging, with the Aussie holding afloat against the Dollar, whilst the Kiwi moves a touch lower. Overnight, both were pressured by the downbeat risk tone, but the Aussie has managed to clamber higher thereafter. Some of the strength may be facilitated by the outperformance in the Yuan, after Chinese trade and inflation data topped forecasts.

FIXED INCOME

- Fixed benchmarks are generally on the backfoot as energy benchmarks opened higher and extended at the start of the week as the negotiating process made no progress on the weekend, with the US and Iran essentially rejecting each other's positions. We now await any revised proposal(s) before looking to the meeting between Chinese President Xi and US President Trump, from Wednesday.

- USTs hit a 110-15 low, with downside of just under 10 ticks, early doors. Since, as the energy space wanes from highs, fixed income has lifted off worst. USTs are now lower by around five ticks and to a 110-23 peak. If the upside continues, we look to resistance at 110-28 and 111-03+ from Thursday and Friday, respectively.

- Gilts underperform vs peer, as markets await a potential leadership challenge against PM Starmer. He remains on the wires at the time of publication, where his comments thus far have largely been as expected; he reiterated that he does not intend to step down. Markets will await updates from Catherine West, who could launch a leadership challenge against the PM if she is not satisfied by his remarks. Gilts are off by around 45 ticks, within a 87.10 to 87.45 range.

- Bunds in-fitting with USTs. Lower by 35 ticks to a 125.35 base early doors. Since, as energy eases, Bunds have trimmed much of the initial pressure and hold off a 125.56 peak, lower by c. 10 ticks.

COMMODITIES

- Geopolitics continues to be the underlying driving force of price action. In short, Iran submitted its response to the latest US proposal to end the war, with Trump calling it “TOTALLY UNACCEPTABLE”. Iranian state media said the US proposal amounted to Tehran surrendering to Trump’s excessive demands. Iran’s counter-position stressed US compensation for war damages, recognition of Iranian sovereignty over the Strait of Hormuz, sanctions relief and release of blocked assets. In terms of diplomacy, Pakistani journalist Mallick posted, "To my understanding, Contrary to publicly put out positions and statements, diplomacy and back channel talks and contacts between Iran and US to work out a draft agreement continues to be in the works -- Diplomacy is not dead”.

- WTI and Brent futures are firmer but off best levels following the initial pop higher on the rejection, with the prospect of ongoing efforts to negotiate taking some sting out of the punchy rhetoric from the US and Iran. WTI Jun hit a high of USD 100.37/bbl (vs low 96.92/bbl) before waning levels under USD 97.70/bbl at the time of writing, though still +2% intraday. Brent July has dipped back under USD 104/bbl from an earlier USD 105.99/bbl peak. Dutch TTF also rose in early trade before waning from a high near EUR 45.50/MWh to a low just under EUR 44.50/MWh.

- Spot gold is modestly softer as the firmer crude prices keep the USD underpinned, though the bullion resides in a narrow USD 4,648.09-4,705.56/oz range at the time of writing, remaining under its 100 DMA (USD 4,781/oz). Spot silver, however, is choppy on either side of the USD 80/oz mark after briefly topping Friday’s USD 81.57/oz peak, with the 100 DMA at USD 80.60/oz.

- Base metals are mixed with sentiment cautiously positive in recent trade as energy prices came off best levels and provided a slight boost to the risk tone. 3M LME copper remains north of USD 13.5k/t in a USD 13,515.70-13,650.20/t range.

- Saudi crude oil supply to China is set to fall to a record low of about 10mln barrels in June, sources say.

- Japan's Industry Ministry said the first Central Asian crude tanker since Iran war has set sail for Japan.

TRADE/TARIFFS

- Indian official said Indian official said the US trade team will reach India soon for discussions; there is no plan to hike duties on gold and silver imports.

NOTABLE EUROPEAN HEADLINES

- UK PM Starmer said the local election results were "very tough" and reiterated he takes responsibility for election loss and will not step down. On the UK-EU relationship, he said Brexit has made the UK weaker and migration higher and vowed to rebuild the EU relationship.

- Talk of UK Cabinet resignations today. However, Mail on Sunday's Hodges expects such interventions to start later in the week, would be surprised to see any today.

- UK Manchester Mayor Burnham said to have identified a specific MP who is on board with a plan to stand down and let him run, POLITICO reported, citing sources.

- UK Labour Backbencher Catherine West told POLITICO she wants to “give a deadline” of Tuesday morning for the required 81 MPs to back her and force a leadership contest. West told POLITICO on Sunday that she still intends to watch Starmer this morning and make up her mind about whether to launch a leadership challenge. “If it’s an amazing speech, then I will think twice about asking the Parliamentary Labour Party for their support,” she told the Telegraph.

NOTABLE EUROPEAN DATA RECAP

- Norwegian Inflation Rate MoM (Apr) M/M 0.4% (Prev. 0.2%).

- Norwegian Inflation Rate YoY (Apr) Y/Y 3.4% (Prev. 3.6%).

- Norwegian Core Inflation Rate MoM (Apr) M/M 0.7% (Prev. 0.1%).

- Norwegian Core Inflation Rate YoY (Apr) Y/Y 3.2% (Prev. 3%).

CENTRAL BANKS

- ECB's Kocher said the risk of stagflationary trend cannot be ruled out.

- ECB's de Guindos said "I think that we have to wait before deciding on the next interest rate move. We need more clarity about the conflict in Iran. We will have new projections in June. Let’s see the data", when asked about a June rate hike.

- BoE's Greene said it is worth waiting a little while to see what happens with the Middle Eastern war and how it will propagate through the economy, speaking to Bloomberg's Odd Lots podcast.

- Bank of Japan appoints Kenji Fujita as new Executive Director, according to Nikkei.

- BoJ appoints Masaki as Executive Director for International Affairs, overseeing BoJ Global Research and G7/G20 liaison.

NOTABLE US HEADLINES

- US housing lenders and state agencies are raising concerns that the Trump administration could wind down a financing programme, according to Semafor. The FY27 budget projects no new commitments for the programme.

- China confirms US President Trump's visit to China on May 13th-15th.

GEOPOLITICS

RUSSIA-UKRAINE

- EU sees the opportunity to prepare another round of sanctions against Russia, with Putin's shadow fleet facing fresh EU sanctions blitz, while banks, military companies and firms selling stolen Ukrainian grain also face penalties, according to POLITICO.

CRYPTO

- Bitcoin reversed just shy of the 200-SMA, returned back below the USD 81k handle.

APAC TRADE

- APAC stocks traded mixed as the region reflected on last Friday's tech rally and NFP beat, as well as firmer-than-expected Chinese data, and geopolitical developments with US President Trump rejecting Iran's response to the peace proposal.

- ASX 200 was dragged lower by heavy losses in the health care sector as CSL shares slumped by around 19% after it flagged a USD 5bln impairment, while sentiment was also not helped by a report that Australia’s government is to scrap the 50% capital gains tax discount by July 2027.

- Nikkei 225 initially climbed to a fresh record high north of the 63,000 level but then wiped out its gains amid headwinds from higher oil prices and weak earnings outlooks for the likes of Nintendo and Honda.

- Hang Seng and Shanghai Comp were varied amid the mixed fortunes among the tech names in Hong Kong, and with the mainland boosted after Chinese trade and inflation data topped forecasts.

NOTABLE ASIA-PAC HEADLINES

- South Korea Finance Minister said economic growth is to exceed 2% this year.

NOTABLE APAC DATA RECAP

- Chinese Inflation Rate MoM (Apr) M/M 0.3% vs. Exp. -0.1% (Prev. -0.7%).

- Chinese Inflation Rate YoY (Apr) Y/Y 1.2% vs. Exp. 0.8% (Prev. 1%).

- Chinese Imports YoY (Apr) Y/Y 25.3% (Prev. 27.8%).

- Chinese Exports YoY (Apr) Y/Y 14.1% (Prev. 2.5%).

- Chinese Balance of Trade (Apr) 84.8B vs. Exp. 82.4B (Prev. 51.13B).

- Chinese PPI YoY (Apr) Y/Y 2.8% vs. Exp. 1.5% (Prev. 0.5%).

Loading...