US indices saw heavy losses on Monday on AI valuation concerns - Newsquawk Asia-Pac Market Open

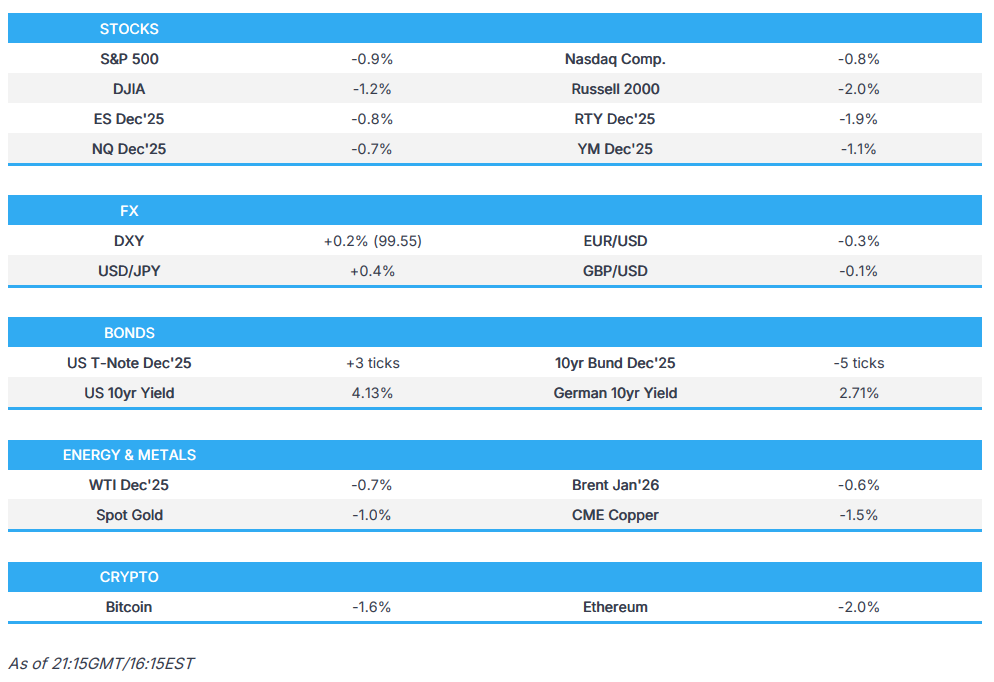

- US stocks saw heavy losses on Monday, with all sectors, aside from Communications and Utilities, in the red.

- Dollar was firmer, albeit in a day of thin trade as we await delayed US data and NVIDIA earnings later in the week.

- T-notes saw slight upside in risk-off trade but capped on Amazon's bond sale.

- Oil prices were choppy, but ultimately settled marginally lower in thin newsflow.

- Looking ahead, highlights include 2054 AGB Auction, RBA minutes.

More Newsquawk in 2 steps:

1. Subscribe to the free premarket movers reports

2. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

SNAPSHOT

US TRADE

- US stocks saw heavy losses on Monday, with all sectors, aside from Communications and Utilities, in the red. There was no one specific catalyst for the risk-off trade to start the week, just further concerns regarding elevated valuations in the AI space, while the SPX slipped below 6,700 and closed beneath its 50-dma of 6,707.

- SPX -0.91% at 6,672, NDX -0.83% at 24,800, DJI -1.18% at 46,590, RUT -1.96% at 2,341

- Click here for a detailed summary.

TARIFFS/TRADE

- The EU is set to warn US Commerce Secretary Lutnick against expanding the scope of US steel tariffs, with officials concerned that a US push to widen the list of EU products facing higher steel and aluminium levies may violate the trade agreement signed this summer; they are also worried that new, higher tariffs across additional industries would dilute the EU–US deal and undermine the agreed 15% ceiling, according to Bloomberg.

- US President Trump expects to issue dividends to Americans based on tariff revenues, probably in the middle of 2026.

NOTABLE US HEADLINES

- White House Economic Adviser Hassett said real wages have gone up and will continue to do so, adding that there are mixed signals in the job market but positive signals in the outlook; he said there could be a period of relative quiet in the labour market, via CNBC.

- Fed Governor Waller made the case for continuing interest rate cuts, supports 25bps rate cut in December. A cut in December would provide additional labour market insurance. Worries restrictive policy is weighing on the economy, says the labour market is weak and near stall speed. Underlying US inflation is close to 2% target.Inflation expectations are well anchored. Tariffs are a one-time price level shock. Does not see any factors that would cause an acceleration in inflation. US GDP growth slowed in H2 25. Dour consumer sentiment lines up with reports from firms of slackening demand. Affordability of housing and cars poses an ongoing challenge for consumers, weighing on spending growth. Unlikely that any data, including upcoming jobs report, would change view that another rate cut is in order.

- Fed Vice Chair Jefferson said the Fed needs to proceed slowly as monetary policy approaches the neutral rate and noted it is still unclear how much government data will be available for the next meeting. He said he supported last month’s quarter-point rate cut as employment downside risks had risen, added that the current policy rate remains somewhat restrictive, and said the balance of risks has shifted in recent months with greater potential downside for employment. He noted that upside risks to inflation have likely declined, with tariff effects seen as temporary, while inflation is running just below 3% and progress toward 2% has stalled. Jefferson said available information points to gradual cooling in both labour supply and demand, and that anecdotal reports on hiring are mixed — some firms slowing or cutting back, others adding workers and investing — and said he looks forward to reviewing the Beige Book, via the Federal Reserve. Jefferson said he is hearing from firm contacts that there is hesitancy to hire due to uncertainty about policy and the impact of AI, adding that once policy uncertainty eases firms may be more likely to pursue hiring plans; he said the current challenge is the tension between the mandates and finding the right way to satisfy both.

DATA RECAP

- US Construction Spending MM (Aug) 0.2% vs. Exp. -0.1% (Prev. -0.1%, Rev. 0.2%)

- NY Fed Manufacturing (Nov): Current business conditions +18.7 (exp. +5.8, prev. +10.7 in Oct).

- Canadian CPI Inflation YY (Oct) 2.2% vs. Exp. 2.1% (Prev. 2.4%)

- Canadian CPI BoC Core MM (Oct) 0.6% (Prev. 0.2%)

FX

- Dollar was firmer, albeit in a day of thin trade as we await delayed US data and NVIDIA earnings later in the week.

- G10 FX saw losses, albeit nothing too extensive and broadly fell foul to the climbing Greenback as opposed to much currency-specific newsflow.

- CAD saw slight two-way trade to the latest inflation metrics. Overall, it was mixed – headline inflation Y/Y eased but was slightly above Wall St. consensus.

- EMFX was largely at the whim of the Dollar amid a lack of newsflow. Out of LatAm, BCB sold USD 1.25bln in dollar auction with repurchase deal.

FIXED INCOME

- T-notes saw slight upside in risk-off trade but capped on Amazon's bond sale.

COMMODITIES

- Oil prices were choppy, but ultimately settled marginally lower in thin newsflow. The real market mover for benchmarks was in the European morning, which took the energy space into the green, amid reports Israeli warplanes have targeted areas in southern Lebanon.

GEOPOLITICAL

MIDDLE EAST

- Israeli warplanes have targeted areas in southern Lebanon, according to Iran International citing Al-Mayadeen Network.

RUSSIA-UKRAINE

- Ukrainian President Zelensky said Ukraine has ordered 100 Rafale fighter jets, according to Reuters.

OTHERS

- US President Trump, when asked if he would launch strikes against Mexico to stop drugs, says it is "okay with me"; says he is not happy with Mexico. Trump says, "Mexico knows where he stands."

- North Korea said South Korea's nuclear-propelled submarine will lead to North Korea arming itself with nuclear weapons, via KCNA; says it will respond to the confrontational stance of the US–South Korea joint factsheet.

ASIA-PAC

NOTABLE HEADLINES

- Japanese PM Takaichi to meet with BoJ Governor Ueda on Tuesday at 06:30GMT.

EU/UK

NOTABLE HEADLINES

- ECB’s Lane delivered remarks titled “The monetary policy of the European Central Bank”, according to Reuters.

- ECB’s Sleijpen said risks are balanced and policy is in a good place, adding that inflation risks for the Eurozone are balanced, according to Reuters.

- ECB’s Makhlouf said monetary policy is in a good place and acknowledged significant uncertainty that requires a meeting-by-meeting approach; he also expressed concern about the financial stability risks of stablecoins and said a regulatory framework is needed to manage those risks, according to Reuters.

- BoE’s Mann said the current environment is showing an upward CPI bias, according to Reuters.

- UK Chancellor Reeves reportedly mulling launching a last-minute raid on banking profits in the budget, according to The Telegraph

- European Commission Autumn 2025 Economic Forecast: "shows continued growth despite challenging environment". "Growth is supported by a resilient labour market, decreasing inflation and favourable financing conditions. In addition, policy support from the Recovery and Resilience Facility and other EU funding is cushioning the effect of tighter fiscal policy in several Member States". "Globally, the US tariffs are at their highest levels in nearly a century. The forecast assumes that all country- and sector-specific tariffs implemented or credibly announced by the US administration at the cut-off date will remain in place throughout the forecast horizon".

DATA RECAP

- Swiss GDP QQ (Q3) -0.5% (prev. 0.1%)

- Italian CPI (EU Norm) Final MM (Oct) -0.2% vs. Exp. -0.2% (Prev. -0.2%); YY (Oct) 1.2% vs. Exp. 1.2% (Prev. 1.2%)

Loading...