US Market Open: US equity futures are modestly lower, whilst DXY is flat as market awaits US CPI - Newsquawk US Opening News

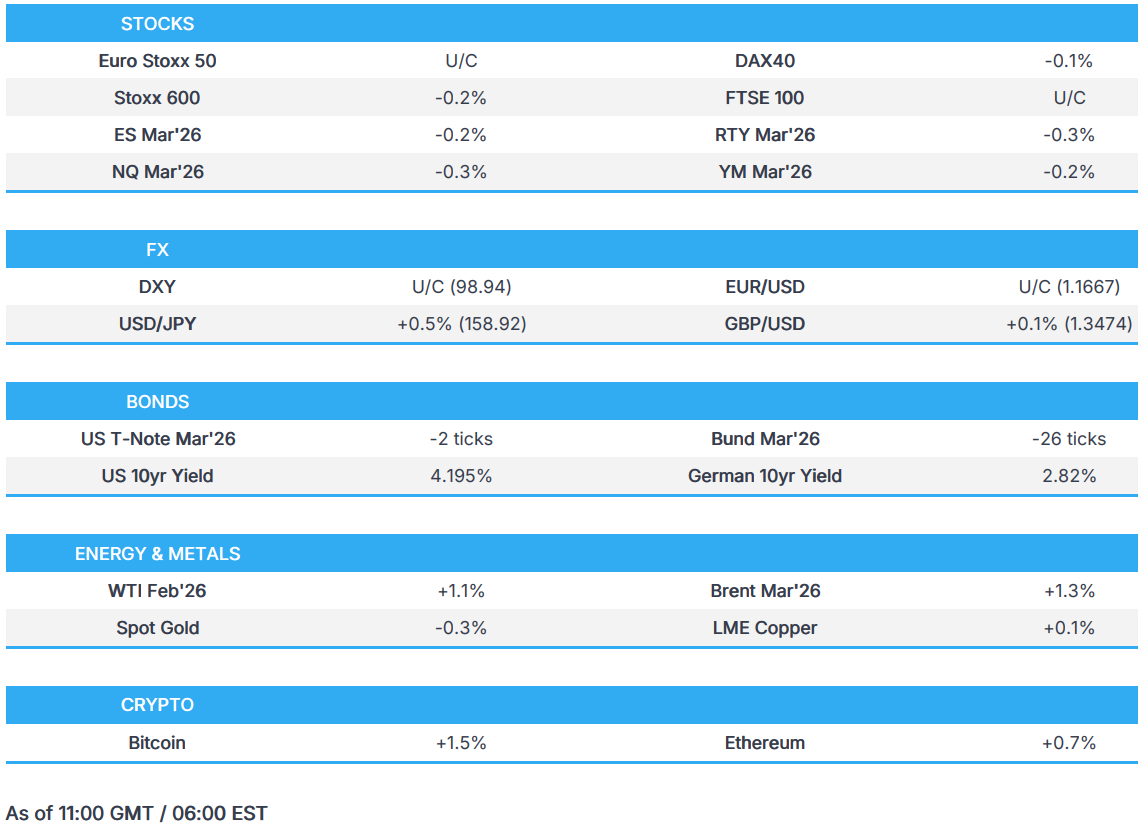

- European bourses are tentative whilst US equity futures are modestly lower as markets await US CPI.

- DXY is flat/incrementally firmer, USD/JPY briefly topped 159.00 as Takaichi eyes a snap election; some modest strength in JPY overnight, on Finance Minister Katayama who said US Treasury Secretary Bessent shares the concerns over the weak JPY.

- Bearish bias from APAC trade, driven by JGBs. Bunds mildly pressured on a weak Bobl outing.

- Spot gold is a little lower awaiting US CPI; Crude climbs amid a Black Sea tanker incident and ongoing Iranian focus.

- Looking ahead, highlights include US NFIB (Dec), US CPI (Dec), Average Weekly Prelim Estimate ADP, EIA STEO, Speakers include Fed’s Barkin and Musalem. Supply from the US.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European equities (STOXX 600 -0.2%) have traded tentatively throughout the morning, as markets await CPI. The AEX (+0.4%) is the key outperformer in the region amid gains in ASML (+1.2%) after Jefferies raised the Co.'s price target, thereby lifting the index.

- European sectors are trading mixed, with Energy (+0.9%), Technology (+0.6%) and Banks (+0.6%) leading. The former has gained amid stronger crude prices given the heightened geopolitical tension between US and Iran, whilst ASML helps boost Tech. On the downside, Autos (-0.7%), Utilities (-0.7%) and Construction & Materials (-2.6%) lag. The latter faced steep losses due to Sika (-7.0%) after the Co.'s FY25 sales fell by 4.8%, with the Chinese market a continued weakness for them.

- US equity futures (ES -0.2% NQ -0.3% RTY -0.3%) are broadly on the backfoot as markets await US CPI. Focus has been on Trump calling on Microsoft to make changes to reduce data center power costs for US citizens.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is flat and trades within a narrow 98.89 to 99.03 range; the high for the day is a couple of pips short of its 50 DMA, while a bout of pressure in the index could see a test of its 200 DMA at 98.80. Focus for the index today will be on US CPI; in brief, the consensus looks for headline CPI to rise by 0.3% M/M in December (prev. 0.3%), and the annual rate to remain unchanged at 2.7% Y/Y. GS expect the figures to exceed consensus, citing firmer food and energy prices.

- Away from the US, G10s are mixed with mild strength in the GBP whilst the JPY is the clear underperformer – other peers are near-enough flat vs the USD. Nothing really driving the strength in the GBP this morning, whilst the JPY has a lot to digest.

- A full JPY analysis piece can be found on the Newsquawk headline feed at 08:55 GMT, but in brief, USD/JPY eclipsed 159.00 for the first time since 11 July 2024. As a reminder, Japan intervened twice on July 11 and 12 to bring the USD/JPY below the 160.00 mark. The latest depreciation in the JPY has been spurred by continued reports of PM Takaichi's plans to call an election, where her aim is to secure a single-party government. This would, in theory, allow her to enact more expansionary fiscal policy.

- Click for Newsquawk JPY Analysis.

FIXED INCOME

- JGBs led the downside overnight as the "Takaichi trade" resumed. For more details, see the 08:55GMT Market Update.

- Amidst this, USTs and Bunds also found themselves lower. USTs by just a handful of ticks and holding above the 112-00 mark and by extension yesterday's trough, which was half a tick below that. Focus turns to US CPI later, where consensus looks for the headline M/M, and Y/Y prints to remain at 0.3% and 2.7% while both core figures are seen higher by a tenth at 0.3% and 2.7% respectively. Goldman Sachs looks for a hotter print driven by technical factors.

- Bunds in-fitting with the above, at a 127.84 low with downside of 28 ticks at most. Bunds made fresh lows following a soft Bobl outing, which had a weak b/c and lower than exp. amount sold. More generally, action for today will likely be dictated by US CPI. If the bearish bias extends, we look to support at 127.89, 127.82 and 127.70 from the last three sessions.

- Gilts gapped lower by 14 ticks at the open, acknowledging the bearish bias from APAC trade, before dipping further to a 92.30 base. Since, the benchmark has recovered to opening levels. No reaction to the passing of I/L supply while the interview with BoE's Bailey took place this morning, but the text won't be published until January 16th.

- Greece begins the sale of a new 10yr bond; guidance seen at +60-65bps to mid swaps.

- Italy sells EUR 4bln vs exp. EUR 3.5-4bln 2.40% 2029 BTP: avg. yield 2.48%, b/c 1.45x

- Germany sells EUR 4.597bln vs exp. EUR 6bln 2.50% 2031 Bobl: Avg yield: 2.47%, b/c 1.41x, retention 23.38%

COMMODITIES

- Crude firmer with geopolitics in focus. Overnight action was somewhat rangebound, as there was no significant escalation or development. However, we did get reports via CBS that President Trump was briefed on military and covert operations against Iran, but no decision has been made.

- Since, as participants digest this risk and reports via BBG that two tankers were attacked in proximity to the Black Sea loading terminal for the CPC, crude has climbed and posts upside in excess of USD 1.00/bbl. At highs of USD 60.82/bbl and USD 65.20/bbl for WTI and Brent, respectively.

- Spot gold is a little lower this morning, taking a breather following the strength seen in the prior session, where the yellow metal made fresh ATHs beyond the USD 4.6k/oz mark. Slight pressure today without a clear driver; potentially profit-taking ahead of US CPI. Price action in Europe has been sideways, and within a USD 4,573.87-4,608.13/oz range.

- A bit of divergence between gold and silver this morning, with the latter posting modest gains and currently holding at the upper end of the day's range, last at USD 85.76/oz.

- Base metals are mixed after choppy trade overnight. 3M LME Copper currently trades within a USD 13,034-13,232/t range. Desks have highlighted that there have been growing fears amongst traders that copper may sharply pull back if demand for the metal slows in 2026, particularly if China curbs spending.

- Citi said its 3-month price target for gold and silver is now USD 5000/oz and USD 100/oz respectively.

- Two oil tankers were attacked in proximity to the Black Sea loading terminal for the CPC, Bloomberg reports citing sources.-Two additional oil tankers have been hit near the Black Sea CPC terminal by drones, according to sources; taking the total on Tuesday to four tankers.

TRADE/TARIFFS

- China's Commerce Ministry outlines the final ruling on the imports of solar polysilicon from the US and South Korea, effective 14th January with tariffs of up to 113.8%. To continue to collect anti-dumping tariffs for another five years.

- China said it opposes unilateral sanctions and "long-arm jurisdiction", following the 25% tariff on US trade for countries doing business with Iran.

- Taiwan officials said 'some' consensus has been reached with the US on a trade deal.

- Japanese Finance Minister Katayama said there were some detailed proposals on rare earth supply chains during the meeting with the US. A potential price floor on rare earths were discussed.

- US President Trump said any countries doing business with Iran are to pay a 25% tariff on any or all business being done with the US.

NOTABLE EUROPEAN DATA RECAP

- French Budget Balance (Nov) -155.4B vs. Exp. -165.0B (Prev. -136.2B, Rev. -136.2B).

- UK BRC Retail Sales YY (Dec) 1.0% (Prev. 1.2%).

CENTRAL BANKS

- Fed's Williams (Voter, Neutral) said monetary policy well positioned amid a favourable outlook and that policy is now closer to neutral, well-positioned ahead of January rate decision; expect that we’ll see [the labor market] stabilize this year". MONETARY POLICY. “In considering the extent and timing of additional adjustments… the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks.”. “Monetary policy is now well positioned to support the stabilization of the labor market and the return of inflation to the FOMC’s longer-run goal of 2 percent.”. “The actions taken by the FOMC… have moved the modestly restrictive stance of monetary policy closer to neutral.”. INFLATION. “Underlying inflation trends have been pretty favorable.”. “Tariffs have been overwhelmingly borne by domestic businesses and consumers.”. “I expect inflation will be just under 2-1/2 percent for this year as a whole, before reaching… 2 percent in 2027.”. “I anticipate inflation will peak at around 2-3/4 to 3 percent sometime during the first half of this year.”. “Inflation appears likely to peak sometime in the first half of this year as the full effects of tariffs are felt.”. “Medium- and longer-term expectations remain well within their pre-Covid ranges.”. “Inflation expectations remain well anchored.”. GROWTH. “The economic outlook is favorable.”. “I expect the economy to grow above trend this year, with real GDP growth between 2-1/2 and 2-3/4 percent.”. “GDP growth looks to have been somewhat above 2 percent last year, and it will likely pick up some this year.”. LABOR MARKET. “This has been a gradual process, without signs of a sharp rise in layoffs.”. “Downside risks to employment have increased as the labor market cooled.”. “The unemployment rate moved up… and ended the year at 4.4 percent.”. “I expect that we’ll see [the labor market] stabilize this year and then strengthen somewhat thereafter.”

- Fed's Williams (Voter, Neutral) said the Fed is not under strong influence to change rates. Expects the next Fed chair to understand the gravity of the role. Strong productivity growth echoes past booms. Adds that the best way to instill confidence in the Fed is to do the job well. He expects improved labour market demand. Confident the Fed will return inflation to 2%. Jobs market is unusual with low hiring, low firing.

- Japan's government is reportedly likely to delay the nomination of a BoJ board member if PM Takaichi called an election, via Reuters citing sources.

- Global central banks are reportedly drafting a statement in support for Fed Chair Powell.

NOTABLE US HEADLINES

- US President Trump reportedly unhappy about AG Pam Bondi's performance and has repeatedly complained to aides, according to WSJ citing sources.

- US NFIB Business Optimism Index (Dec) 99.5 vs. Exp. 99.5 (Prev. 99.0)

NOTABLE US EQUITY HEADLINES

- Google (GOOGL) is reportedly set to develop and make high-end phones in Vietnam in 2026, as the Co. aims to move supply chains away from China, according to Nikkei Asia.

- Boeing (BA) said Aviation Capital Group has finalised a new order for 50 737 max jets.

- Microsoft (MSFT) President Smith warns that China is winning the AI race as China combines low-cost "open" models with hefty state subsidies.

- NVIDIA (NVDA) said we do not require upfront payment and would never require customers to pay for products they do not receive.

- US President Trump posted "I never want Americans to pay higher Electricity bills because of Data Centers", said Microsoft (MSFT) will make a major change this week to make sure Americans do not "pick up the tab" for their power consumption.

- AbbVie (ABBV) has signed an agreement with the Trump administration, securing a tariff exemption.

- Crown Castle (CCI) sues DISH Wireless over USD 3.5bln default.

- Wayfair (W) partners with Google (GOOGL) to advance AI-powered shopping for the home.

GEOPOLITICS

RUSSIA-UKRAINE

- A push by French President Macron and Italian PM Meloni to begin discussions with the Russian Kremlin is gaining traction in EU capitals and in Brussels itself, Politico reported citing sources. Primary goal to ensure EU red lines are not crossed. and to signal to the US that the EU has leverage. Elsewhere, creation of the role of EU special envoy to Ukraine hs support of the Council and leaders. Mario Draghi and Alexander Stubb have been touted. However, EU diplomat Kallas opposes the role.

- Kyiv Mayor said the Russians are attacking the capital with ballistic missiles and that explosions are being heard.

MIDDLE EAST

- US President Trump is leaning towards striking Iran to punish the regime for killing protesters, but hasn't made a final decision and is exploring Iranian proposals for negotiations, a White House official with direct knowledge told Axios.

- Iran's Foreign Minister said Tehran is ready for any action by the US, including military action.

- China said it opposes unilateral sanctions and "long-arm jurisdiction", following the 25% tariff on US trade for countries doing business with Iran.

- US President Trump has been briefed on a range of military and covert options against Iran, according to CBS News; however no final decision has been made and diplomatic channels remain open.

- "EU intends to impose new sanctions on Iran", Sky News Arabia reported.

- "Washington called on Dual U.S.-Iranian Citizens to Leave Iran", Al Arabiya reported.

- US President Trump said any countries doing business with Iran are to pay a 25% tariff on any or all business being done with the US.

- US President Trump is leaning towards striking Iran to punish the regime for killing protesters, but hasn't made a final decision and is exploring Iranian proposals for negotiations, a White House official with direct knowledge told Axios.

- Iranian authorities claim that the situation is 'under control'.

- "EU intends to impose new sanctions on Iran", Sky News Arabia reported.

- US President Trump has been briefed on a range of military and covert options against Iran, according to CBS News; however no final decision has been made and diplomatic channels remain open.

- "Washington called on Dual U.S.-Iranian Citizens to Leave Iran", Al Arabiya reported.

- At least two unsanctioned supertankers are departing Venezuelan waters carrying crude oil, according to reported citing TankerTrackers.

- US Treasury Secretary Bessent posted that he was pleased to hear a strong, shared desire to quickly address key vulnerabilities in critical minerals supply chains; "I am optimistic that nations will pursue prudent derisking over decoupling".

CRYPTO

- Bitcoin is on a slightly firmer footing this morning and trades around USD 92k whilst Ethereum posts gains to a slightly lesser magnitude.

- Punchbowl's Pederson writes that "we obtained the latest discussion draft of crypto market structure legislation", and the bill was reportedly sent to the Democrats on Monday. As it stands, the section related to stablecoin yields remains blank.

APAC TRADE

- Asia-Pac stocks followed on from Monday’s gains, with equities mostly in the green.

- ASX 200 started the session on the front foot, +0.4%, before extending gains and currently trading just shy of session highs at 8835. With spot XAU trading near ATHs, this has aided sectors such as metals and mining (2.0%) to continue Monday’s gains.

- Nikkei 225 returned from its long weekend with a gap higher, resulting in the index opening with gains as much as 3.7% and forming new ATHs. This comes amid a weaker JPY and growing speculation of PM Takaichi dissolving parliament. Japanese media noted that the LDP was looking to capitalise on Takaichi's high approval ratings.

- KOSPI opened Tuesday’s trade at ATHs and oscillated at highs before peaking at 4681 and slightly paring back, but remains comfortably in the green.

- Hang Seng and Shanghai Comp. opened in line with the broader sentiment, with the former surging higher, aided by gains in Gigadevice (3986 HK). The latter is the laggard across Asia-Pacific equities, trading with slight gains of 0.2%.

NOTABLE ASIA-PAC HEADLINES

- China examines foreign ETF trades after Jane Street India probe, Bloomberg reported.

- Japanese Finance Minister Katayama said she shared concerns with US Treasury Secretary Bessent over weak JPY.

NOTABLE APAC DATA RECAP

- Japanese Bank Lending YoY (Dec) Y/Y 4.4% vs. Exp. 4.1% (Prev. 4.2%).

- Japanese Current Account (Nov) 3.674tln vs Exp. 3.594tln (Prev. 2.834tln, Rev. 2.834tln).

- Australian Westpac Consumer Confidence Index (Jan) 92.9 vs. Exp. 97 (Prev. 94.5).

- Australian Westpac Consumer Confidence Change (Jan) -1.7% vs. Exp. 2.6% (Prev. -9.0%, Rev. -9%).

- New Zealand NZIER Capacity Utilization (Q4) 89.8% vs. Exp. 89.3% (Prev. 89.1%).

Japanese Defense Minister Koizumi said assessments are ongoing into the impact of China's decision to restrict exports to Japan of dual-use items for military purposes.

Loading...