US stocks boosted, JPY strengthened on jawboning and potential intervention - Newsquawk Daily Asia-Pac Opening News

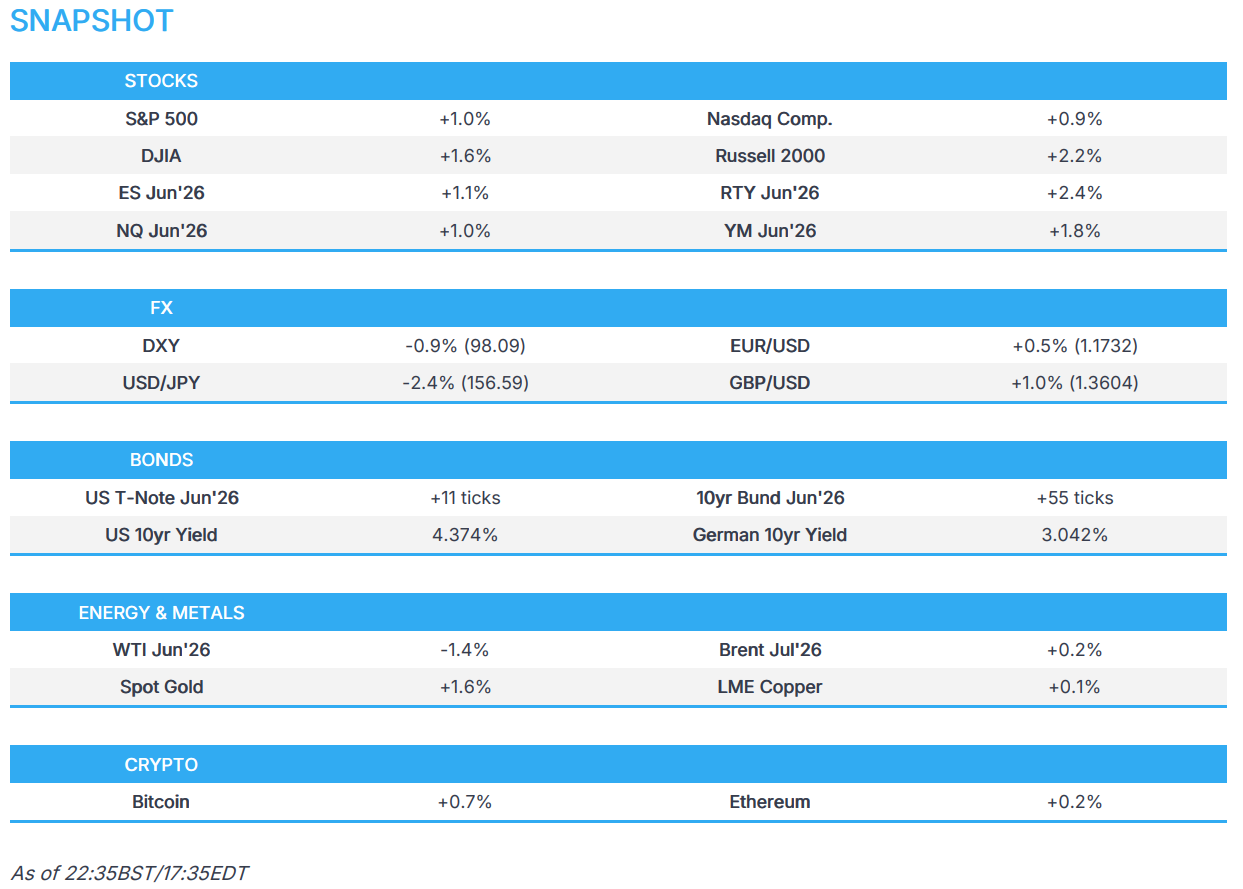

- US stocks rallied as markets leaned risk-on despite ongoing geopolitical uncertainty around US/Iran developments. Sentiment was boosted by strong earnings. Alphabet and Amazon impressed with robust growth and strong cloud demand, while Qualcomm reversed earlier losses on upbeat commentary about China phone shipments. However, mega-cap tech saw some divergence, with Microsoft and Meta pressured by concerns over elevated AI-related capex. Elsewhere, cyclicals and defensives broadly gained, with Communication Services leading sectors while Technology lagged.

- JPY outperformed its G10 peers, USD/JPY plummeted, earlier initiated by jawboning and then further driven by a report by the Nikkei, confirming that the MoF had intervened from an official.

- Looking ahead, highlights include Japanese Tokyo CPI (Apr), S&P Manufacturing PMI (Apr), South Korean Trade Balance (Apr), Australian S&P Manufacturing PMI (Apr), PPI (Q1), Supply from Australia, Holidays in India, Singapore, China & Taiwan.

More Newsquawk in 2 steps:

1. Subscribe to the free premarket movers reports

2. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- US President Trump said Iran dying to make a deal and stated that Iran cannot be nuclear. He added that he doesn't know if the ceasefire with Iran needs to be broken, but we may do. Furthermore, he commented that Iran's drone and missile factories are significantly down and that Iran is in very bad shape. On a deal, he said he doesn't know if we need a deal with Iran but however backtracked and said a deal might be needed. Later, he stated that he would not have approved enriched Uranium for Iran and needs guarantees Iran will not have a nuclear weapon ever.

- US President Trump is reportedly considering significant new combat operations in Iran to resolve a deadlock, Semafor reported. This echoed the Axios report overnight that US CENTCOM is to brief US President Trump on new plans for potential military action in Iran.

- US President Trump floats a new plan to reopen the Strait of Hormuz; US would continue its blockade on Iranian ports, while coordinating with allies to impose higher costs on Iran’s attempts to subvert the free flow of energy, according to AP citing official. This echoed the WSJ report overnight regarding the “Maritime Freedom Construct” coalition.

- Two Pakistani officials in Islamabad with direct knowledge of the talks between the U.S. and Iran told MS NOW they expect a revised Iranian proposal to end the war by the end of the week.

- Pakistan's Foreign Ministry said channels of dialogue with officials in Washington and Tehran remain open.

- Iranian Parliament Speaker Ghalibaf said Iran, by exercising control over the Strait of Hormuz, will ensure that it and its neighbours enjoy the precious blessing of a future free from the presence and interference of the US.

- Iran President Pezeshkian and Ghalibaf, are dissatisfied with the way Foreign Minister Araghchi is advancing diplomacy,especially the nuclear negotiations, and are calling for his dismissal, according to Iran International citing sources.

- IRGC Aerospace Force Command wrote in response to CENTCOM "we have seen the end of your bases in the region, and we will also see your ships", SNN reported.

- Iranian Foreign Ministry Spokesperson said that it is not responsible to expect a quick conclusion of the negotiations and that the other party has not used the opportunity provided by Iran's proposal. Iran must be ready for any eventuality.

- Iranian Supreme Leader said a new chapter for the Gulf and Strait of Hormuz is taking shape,and that Iran will guard its missile and nuclear technology as it guards its borders.

- Iranian lawmaker Mottaki said a naval blockade would amount to a declaration of war, and that fighters could decide as soon as tomorrow or next week to remove such obstacles via military action.

- Iranian lawmaker said there is "no point" in negotiating over zero enrichment, Al Jazeera reported, and is not objected to going to the negotiating table, but we should have looked more closely at how to proceed.

- Israel prepares to announce the failure of negotiations with Iran, via Channel 12 cited by Al Arabiya, with Iran International stating that Israeli officials consider the collapse of negotiations between Washington and Tehran likely as early as next week.

- The US may allow Israel to target Iran's energy facilities if negotiations fail, according to Channel 12 cited by Al Arabiya.

- Israeli Defence Minister said they may soon be asked to move again to ensure the achievement of goals in Iran.

- Air defence sounds were heard in some areas of Tehran, due to countering micro-birds and reconnaissance drones, according to Tasnim.

- Japanese PM Takaichi said that she has worked to ensure passage of Japanese-related vessel through the Strait, following a call with the Iranian President.

- UAE bans travel by citizens to Iran, Lebanon, and Iraq.

US TRADE

- US stocks rallied as markets leaned risk-on despite ongoing geopolitical uncertainty around US/Iran developments. Sentiment was boosted by strong earnings. Alphabet and Amazon impressed with robust growth and strong cloud demand, while Qualcomm reversed earlier losses on upbeat commentary about China phone shipments. However, mega-cap tech saw some divergence, with Microsoft and Meta pressured by concerns over elevated AI-related capex. Elsewhere, cyclicals and defensives broadly gained, with Communication Services leading sectors while Technology lagged.

- Apple (AAPL) Q2 2026 (USD): EPS 2.01 (exp. 1.95), Revenue 111.2bln (exp. 109.45bln). Raised its dividend by 4% to USD 0.27/shr. Beat revenue metrics except for iPhone net sales. Authorised additional program to repurchase up to USD 100bln.

- SPX +1.02% at 2,709, NDX +0.98% at 27,452, DJI +1.62% at 49,652, RUT +2.21% at 2,800.

- Click here for a detailed summary.

TARIFFS/TRADE

- US President Trump said the US will be removing the tariffs and restrictions on Whiskey having to do with Scotland's ability work with the Commonwealth of Kentucky on whisky and bourbon, and in honour of the King and Queen in the UK.

- Chinese VP He Lifeng held a call with USTR Greer with both agreeing to manage differences and boost cooperation. China raised concerns about recent restrictive measures from the US.

- EU Trade Commissioner Sefcovic said the bloc will stand its ground, following on from China threatening retaliatory measures over industrial policy plans.

- USTR Greer said the US will extend preferential treatment to other UK goods.

CENTRAL BANKS

- The ECB left rates unchanged at 2.0%, as expected; says it is well positioned to navigate the current uncertainty.Maintained its data-dependent and meeting-by-meeting guidance. while upside inflation risks have intensified and short-horizon expectations have "significantly" increased, longer-term expectations remain anchored.

- In the post-meeting statement, President Lagarde says incoming information broadly consistent with previous view of inflation outlook, upside risks to inflation and downside risks to growth have intensified. On policy, she said the ECB is well-positioned to navigate uncertainty. Long-term inflation expectations well-anchored, short-term expectations have moved up.

- On the Q&A, Lagarde said the decision was unanimous, but policymakers debated a rate hike today. When asked about the potential for a June rate hike, she could not confirm whether we are close to Baseline Scenario 1 or 2; but we are certainly are moving away from the baseline. Does not think stagflation applies to the current situation. She stated that directionally, she knows where the ECB is heading, but again notes the uncertainty, and says it remains to be seen.

- ECB policymakers see a June hike as very likely, Reuters reported citing sources; some advocated a move in April, could were ok with waiting until June. Further reporting by Bloomberg stated that ECB officials see June hike if energy prices do not ease first.

- The BoE maintains Bank Rate at 3.75%, as expected, in 8-1 vote (exp. 9-0); Pill votes to raise Bank Rate by 25bps to 4%. The language from most policymakers outlined that a hold is the most appropriate course of action at this time, while they wait for information on the size and duration of the shock, alongside the potential second-round effects. Pertinently, and lending a hawkish skew to things, Bailey notes that he currently places weight on Scenario B, but with slightly reduced second-round effects, and some weight on Scenario C, which would require a stronger monetary policy response.

- In the post-meeting statement, Governor Bailey stated that the conflict in the Middle East is having a significant economic impact. He stated that rates were held due to 1) weakness in activity, likely to reduce second round effects; and 2) uncertainty about strength of second-round effects. On inflation, he sees inflation at above 3.5% by year-end, due to Middle East conflict but noted uncertainties surrounding forecasts.

- In the Q&A, Bailey said different policy rules give different answers; there is a good deal of space available to accommodate inflation pressures by not cutting rates. On the possibility of a 50bps hike ahead, he noted that the volatility makes it hard to put probabilities on the scenarios outlined. It would be a mistake to wait for second-round effects before acting and the MPC will need to look at a broad-range of evidence. He said he will be looking for first-round effects (energy prices), indirect effects that impact costs of production, then second-round effects. Asked if the message is to 'get ready for rate hikes', he said no and that today is an active hold.

- In a interview post-policy announcement, BoE Governor Bailey said he wouldn't say the rate decision was dovish and that energy shock is playing out against a soft backdrop.

NOTABLE HEADLINES

- White House Official said US President Trump is expected to sign the DHS funding Bill on Thursday.

- Fitch said large US deficits to keep debt above "AA" peers and cuts 2026 US tariff revenue estimate by USD 150bln.

DATA RECAP

- US PCE Price Index YoY (Mar) Y/Y 3.5% (Prev. 2.8%).

- US PCE Price Index MoM (Mar) M/M 0.7% (Prev. 0.4%).

- US Core PCE Price Index MoM (Mar) M/M 0.3% vs. Exp. 0.3% (Prev. 0.4%).

- US Core PCE Price Index YoY (Mar) Y/Y 3.2% (Prev. 3%).

- US GDP Price Index QoQ Adv (Q1) Q/Q 4.5% vs. Exp. 3.9% (Prev. 3.7%).

- US GDP Growth Rate QoQ Adv (Q1) Q/Q 2.0% vs. Exp. 2.1% (Prev. 0.5%).

- US Personal Spending MoM (Mar) M/M 0.9% vs. Exp. 0.9% (Prev. 0.4%).

- US Personal Income MoM (Mar) M/M 0.6% vs. Exp. 0.3% (Prev. -0.1%).

- US Initial Jobless Claims (Apr/25) 189k vs. Exp. 215k (Prev. 214k, Low. 199k, High. 225k).

- US Continuing Jobless Claims (Apr/18) 1785k.

- Atlanta Fed GDPNow (Q2 initial): 3.7%.

- Canadian GDP MoM Prel (Mar) M/M 0.4.

- Canadian GDP MoM (Feb) M/M 0.2 vs. Exp. 0.2 (Prev. 0.1).

- Canadian Average Weekly Earnings YoY (Feb) Y/Y 3.4% (Prev. 2.0%).

FX

- DXY was broadly weaker against peers as risk-on sentiment across equities fed into FX markets. A muted USD reaction was seen to GDP growth of 2.0% (exp. 2.1%), in-line March PCE readings and initial claims hitting their lowest level since 1969. Geopolitical developments continued to point to an impasse in US-Iran talks, with Axios reporting that CENTCOM was due to brief Trump on new plans for potential military action in Iran on Thursday.

- EUR saw smaller gains than its peers after a broadly expected ECB announcement, with rates maintained and commentary acknowledging the increasingly stagflationary environment that is emerging. The ECB stuck to the script on data-dependent and meeting-by-meeting guidance. ECB sources via Reuters noted that policymakers see a June hike as very likely; some advocated a move in April but were okay with waiting until June.

- GBP was helped by the hawkish tilt in the BoE decision to hold, with Pill voting for a 25bps hike. BoE Governor Bailey said he would not describe the rate decision as dovish and that the market reaction to the BoE rate decision had been very sensible. Cable hit a new April high of 1.3612

- JPY outperformed its G10 peers, USD/JPY plummeted, earlier initiated by jawboning and then further driven by a report by the Nikkei, confirming that the MoF had intervened from an official. Jawboning started with FinMin Katayama, stating that timing to take decisive action is near and that "we are getting closer to taking decisive steps in FX". Following Katayama's comments, Top Currency Diplomat Mimura said this is the final warning before action is taken, speculative moves in FX are mounting and are getting closer to taking decisive steps. USD/JPY returned back below the 157 handle, after starting the day beyond 160.00.

FIXED INCOME

- T-notes rose across the curve on Thursday, with yields declining as T-notes gradually pared some of the recent sell-off. Price action remained driven by moves in crude and geopolitics, despite mixed headlines, with softer oil prices helping yields retrace some of the recent upside.

COMMODITIES

- Oil prices were lower on Thursday. WTI and Brent saw strength overnight and hit highs of USD 103.78/bbl and 114.70/bbl respectively, as the US blockade remained central, with Washington also weighing fresh military options including strikes, Hormuz intervention, and uranium seizure operations. Downside in the oil complex coincided with dollar weakness (following Japanese jawboning) and comments by Japanese PM Takaichi stating that she has worked to ensure passage of Japanese-related vessel through the Strait, following a call with the Iranian President. Benchmarks once again tested the earlier lows amid reports the US DoE solicits exchange of up to 92.5mln bbls of oil from the SPR. On the geopolitical footing, Israeli Defence Minister said they may soon be asked to move again to ensure the achievement of goals in Iran while two Pakistani officials in Islamabad with direct knowledge of the talks between the U.S. and Iran told MS NOW they expect a revised Iranian proposal to end the war by the end of the week.

- US DoE solicits exchange of up to 92.5mln bbls of oil from SPR.

- China reportedly to allow state refiners to export some fuels to Asia buyers.

- Russia's Deputy PM Novak said UAE's exit does not mean a price war and reiterated there are no plans to leave OPEC+. On the May 3rd OPEC+ meeting, Novak said the group will evaluate possibilities to supply global oil market.

- US NEC Director Hassett said they are in constant communication with oil firms to see how to increase production "soon".

- US EIA Natural Gas Stocks Change (Apr/24) 79.

- Regional Governor said the fire at Russia's Tuapse oil refinery has been extinguished.

- PBoC and China customs are easing gold and gold product import/export permit rules by simplifying procedures and facilitating trade.

- BofA pulls forward its USD 4k/T price forecast for aluminium from Q2 '27 to Q4 '26. On copper, the bank said mine supply remains tight and continue to anticipate deficit this year and next, and see copper prices gradually rising above USD 15k/T.

ASIA-PAC

NOTABLE HEADLINES

- Japan said to have intervened in FX, a government official confirmed to the Nikkei.

- Japanese Finance Minister Katayama said timing to take decisive action is near and that "we are getting closer to taking decisive steps in FX". We have long mentioned possible bold action on FX and are monitoring FX while on holiday.

- Japanese Top Currency Diplomat Mimura said this is the final warning before action is taken. Speculative moves in FX are mounting and are getting closer to taking decisive steps. Looking at markets on all fronts.

EU/UK

NOTABLE HEADLINES

- The Finance & Leasing Association abandoned plans to challenge the City watchdog’s GBP 9.1bln motor finance mis-selling compensation scheme after a direct intervention from the Financial Conduct Authority’s chief executive, according to Sky News.

DATA RECAP

- EU Inflation Rate YoY Flash (Apr) Y/Y 3.0% vs. Exp. 2.9% (Prev. 2.6%); Services 3.0% (prev. 3.2%).

- EU Inflation Rate MoM Flash (Apr) M/M 1% (Prev. 1.3%).

- EU Super Core Inflation Rate YoY Flash (Apr) Y/Y 2.2% vs. Exp. 2.1% (Prev. 2.3%); Core 2.1% vs exp. 2.3% (prev. 2.2%).

- French prelim. HICP (Apr): 2.5% Y/Y vs exp. 2.3% (prev. 2.0%); 1.2% M/M vs exp. 0.9% (prev. 1.1%).

- French Inflation Rate MoM Prel (Apr) M/M 1% vs. Exp. 1% (Prev. 1%).

- French Inflation Rate YoY Prel (Apr) Y/Y 2.2% (Prev. 1.7%).

- Italian Inflation Rate MoM Prel (Apr) M/M 1.2% vs. Exp. 0.6% (Prev. 0.5%).

- Italian Inflation Rate YoY Prel (Apr) Y/Y 2.8% (Prev. 1.7%).

- EU GDP Growth Rate QoQ Flash (Q1) Q/Q 0.1% vs. Exp. 0.2% (Prev. 0.2%).

- EU GDP Growth Rate YoY Flash (Q1) Y/Y 0.8% vs. Exp. 0.8% (Prev. 1.2%).

- Spanish GDP Growth Rate YoY Flash (Q1) Y/Y 2.7% (Prev. 2.7%).

- Spanish GDP Growth Rate QoQ Flash (Q1) Q/Q 0.6% vs. Exp. 0.5% (Prev. 0.8%).

- Italian GDP Growth Rate YoY Adv (Q1) Y/Y 0.8% (Prev. 0.8%).

- Italian GDP Growth Rate QoQ Adv (Q1) Q/Q 0.2% vs. Exp. 0.1% (Prev. 0.3%).

- German GDP Growth Rate QoQ Flash (Q1) Q/Q 0.3% vs. Exp. 0.2% (Prev. 0.3%).

- German GDP Growth Rate YoY Flash (Q1) Y/Y 0.3% (Prev. 0.4%).

- German Unemployment Rate (Apr) 6.4% vs. Exp. 6.3% (Prev. 6.3%).

- German Retail Sales MoM (Mar) M/M -2.0% vs. Exp. -0.6% (Prev. -0.6%).

- German Retail Sales YoY (Mar) Y/Y -2.0% (Prev. 0.7%).

- German Import Prices YoY (Mar) Y/Y 2.3% (Prev. -2.3%).

- German Import Prices MoM (Mar) M/M 3.6% vs. Exp. 3.3% (Prev. 0.3%).

Loading...