US stocks higher ahead of Samsung Q2 figures - Newsquawk Daily Asia-Pac Market Open

- US stocks closed higher on Monday following the long Independence Day weekend, with the Nasdaq outperforming as Technology led the advance. Semiconductor stocks were among the strongest performers (SOXX +3%), while memory names rallied around 7% ahead of Samsung's preliminary earnings release overnight. Alongside Technology, Communication Services, and Consumer Discretionary outperformed, while the traditional defensive sectors of Health Care, Consumer Staples and Real Estate lagged.

- Crude futures were rangebound as US President Trump gets ready to travel to the NATO Summit in Turkey.

- Looking ahead, highlights include Japanese Household Spending (May), Leading Index (May), and Supply from Japan.

- Click for the Newsquawk Week Ahead.

More Newsquawk in 2 steps:

1. Subscribe to the free premarket movers reports

2. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

US TRADE

- US stocks closed higher on Monday following the long Independence Day weekend, with the Nasdaq outperforming as Technology led the advance. Semiconductor stocks were among the strongest performers (SOXX +3%), while memory names rallied around 7% ahead of Samsung's preliminary earnings release overnight. Alongside Technology, Communication Services, and Consumer Discretionary outperformed, while the traditional defensive sectors of Health Care, Consumer Staples and Real Estate lagged.

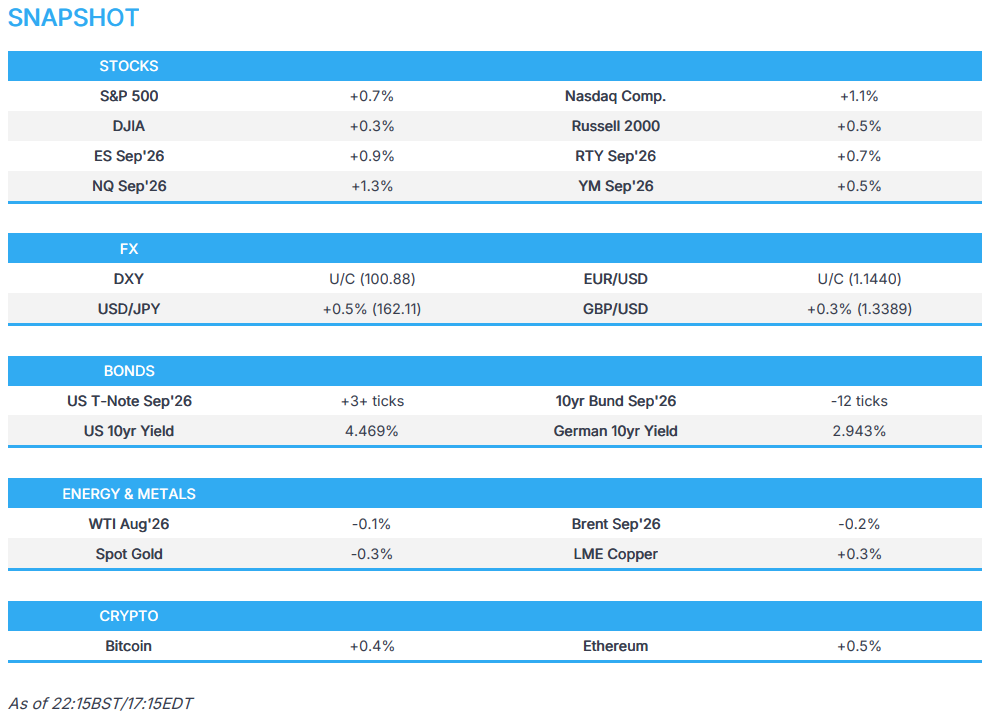

- SPX +0.72% at 7,537, NDX +1.26% at 29,698, DJI +0.29% at 53,061, RUT +0.45% at 3,009

- Click here for a detailed summary.

CENTRAL BANKS

- Fed's Waller (voter, hawk) said forward guidance can speed the impact of monetary policy and it can be a 'valuable tool'. However, it can be a hindrance if it is ‘too strong or rigid’ and also ‘problematic’ when policymakers confront different economic outcomes all with a significant probability of occurring. In separate remarks, Waller said the risks have flipped around, the labour market seems stabilised, and inflation has been taking off, which changes how you think about policy.

- ECB's Schnabel said we are not in a pre-war situation even after the fall in oil prices and cannot simply look through the shock.

- ECB's Wunsch said it seems the Iran shock has disappeared and have not seen much second round effects. Maybe we have to do more, but the situation does not ask for a significant tightening. However, Wunsch is not excluding another move, but let's not wait too long.

- BoC survey: Q2 balance of opinion on indicators of future sales is +15 (prev. +24 in Q1). The Consumer Survey showed inflation expectations declined after the Iran ceasefire was signed in mid-June and the survey of consumers for next 12 months showed 54.6% of Canadians expect a recession (prev. 55.7% in Q1).

NOTABLE HEADLINES

- US President Trump said Chinese President Xi is coming here this September and may be September 24th.

- US President Trump praised Dell (DELL), saying to "go out and buy a Dell computer". Additionally, he thanks Micron (MU) for contributions to Trump Accounts.

DATA RECAP

- US ISM Services PMI (Jun) 54.0 vs. Exp. 54.2 (Prev. 54.5).

- US ISM Services Prices (Jun) 67.7 (Prev. 71.3).

- US ISM Services Employment (Jun) 51.2 (Prev. 47.9).

- US ISM Services New Orders (Jun) 55.1 (Prev. 57.3).

- US ISM Services Business Activity (Jun) 55.4 (Prev. 57.7).

- US S&P Global Composite PMI Final (Jun) 51.9 vs. Exp. 52.2 (Prev. 51.5).

- US S&P Global Services PMI Final (Jun) 51.2 vs. Exp. 51.3 (Prev. 50.7).

- Canadian S&P Global Composite PMI (Jun) 47.9 (Prev. 50.8).

- Canadian S&P Global Services PMI (Jun) 47.1 (Prev. 50.6).

FX

- DXY started Monday on the front foot and traded to a peak of 101.15 before gradually reversing in the US session, despite a clear driver. The reversal came following ISM Services PMI and comments by Fed's Waller. The former missed estimates slightly, while the breakdown also ticked lower from their priors (outside of employment). Comments by Fed's Waller were on the hawkish side, stating that risks have flipped around, with the labour market seemingly stabilised and inflation taking off. The downside in DXY came despite the hawkish rhetoric by Waller.

- EUR found a trough at 1.1409 before reversing to 1.1440, helped by the softening dollar. Further contrasting ECB commentary throughout the day, with Schnabel stating that we cannot simply look through the shock as oil prices fall, while Wunsch said he has not seen much second round effects. On the data front, EZ PPI and Retail Sales printed broadly in line with expectations while German Factory Orders beat estimates by a big margin; however EUR/USD was unreactive.

- GBP was the outperformer, finding support at the 1.3330 handle before extending higher to a peak of 1.3397. No real driver for the GBP outperformance, with a lack of political updates or data released.

- JPY remained on intervention watch, but with US participants returning from their extended weekend, the conditions are not favoured for Japanese officials. USD/JPY regained the 162.00 handle and rose to a peak of 162.42.

FIXED INCOME

- T-notes were little changed on return from Independence Day weekend ahead of supply and FOMC minutes. There was little in the way of fresh macro catalysts, although crude prices edged lower after OPEC+ agreed over the weekend to increase oil production, in line with expectations. Additional downside pressure came after Saudi Aramco cut its official selling price for Arab Light crude to Asia by USD 11.00/bbl, marking the largest reduction in 26 years.

COMMODITIES

- Oil prices was marginally lower to start the week, albeit in very thin newsflow, as traders returned from the holiday weekend. Benchmarks were rangebound throughout the duration of the session amid a lack of headline-driven trade, which saw WTI trade between USD 67.82-69.21/bbl and Brent USD 71.02-72.61/bbl. Little new was said on geopolitics but reports suggest talks could resume from Saturday. Elsewhere, OPEC+ met over the weekend where they agreed to lift production by 188k BPD from August, in fitting with reports last week. Meanwhile, Saudi Arabia’s August’s OSPs were released; Arab Light crude oil to Asia set at USD -1.50/bbl to ICE Brent settlement, an USD 11/bbl reduction, the largest cut to its main oil price since at least 2000; NW Europe OSP was set at USD +0.85/bbl to Ice Brent settlement and USD +3.60/bbl vs ASCI to US. The calendar ahead is quiet, although US players will await the World Cup knockout soccer match versus Belgium, where star striker Balogun has controversially been allowed to play.

- Saudi Arabia August OSPs: Arab Light crude oil to Asia set at USD -1.50/bbl to ICE Brent settlement, to NW Europe at USD +0.85/bbl to ICE Brent settlement, to USA at USD +3.60/bbl vs ASCI, according to a pricing document.

- UAE crude production jumps above 3.8mln BPD in June, according to source reports.

- Israel's energy minister said Israel is launching a new competitive process to search for more natural gas in the country's economic waters.

- Goldman Sachs lowered its LME aluminium price forecast to USD 2,950/t for Q4 2026 and lowered its 2027 average forecast to USD 2,700/t

GEOPOLITICAL

MIDDLE EAST

- US President Trump said they have gotten concessions regarding Iran and regime change is not being pursued. Would rather make a deal with Iran, though he added that "we have not given Iran any money".

- Iranian Parliamentary Speaker Ghalibaf said the US memorandum is 'difficult but possible' to enforce, Al Jazeera reported.

- Israeli warplanes attacked Nabatiyeh in southern Lebanon, Nour News reported citing Lebanese press.

- Reported ceasefire violation in Lebanon again, according to Fars News citing sources. Lebanese sources reported an artillery attack by the Israeli occupying army on the town of "Qabreikha" in the Marjayoun region in southern Lebanon.

- Lebanese sources said there is no date for Israel's withdrawal from the experimental areas, Al Hadath reported.

- A fleet of 10 Japan-related ships have reportedly left the Strait of Hormuz, according to shipping data.

RUSSIA-UKRAINE

- US President Trump said Russia is feeling the pressure regarding Ukraine. Talks are underway in an effort to end the war. Had a good call with Russian President Putin over the weekend.

- NATO could pledge at least EUR 140bln in financial support for Ukraine over the next two years, Handelsblatt reported citing German government sources.

- EU's von der Leyen said the EU is working to seal the 21st Russian sanctions package in the next days.

- Russian Defence Ministry said Ukraine made an attempt to damage civil fuel and energy infrastructure in Russian regions.

- Ukraine's military said it has struck its oil refineries in Russia's Yaroslavl and Leningrad regions. Additionally, Ukraine's Top Drone Commander said it struck two Russian shadow fleet tankers in the Azov Sea. Furthermore, Ukraine confirmed that it struck an oil refinery in Russia's Omsk area.

- Ukraine's Naftogaz said a Russian attack struck its gas production facility in the Kharkiv region.

OTHER

- A Russian Diplomat said the US opted for an arms race by refusing to voluntarily comply with the START treaty, Tass reported.

- Japan Government said it has lifted Chinese missile-related Notam and navigation warnings after Chinese authorities said "planned space activity" has finished.

- Taiwan Government's China policy-making department said China's missile launch into pacific heightens tensions in region.

EU/UK

NOTABLE HEADLINES

- UK Defence Minister Jarvis told POLITICO he wants Burnham’s administration to lay out the full pathway to spending 3.5% of GDP on defense at the next spending review, due spring 2027.

DATA RECAP

- EU Retail Sales MoM (May) M/M 0.2% vs. Exp. 0.2% (Prev. -0.4%).

- EU Retail Sales YoY (May) Y/Y 1.6% vs. Exp. 1.5% (Prev. 1%).

- EU PPI MoM (May) M/M 0.2% vs. Exp. 0.2% (Prev. 0.6%).

- EU PPI YoY (May) Y/Y 5.9% vs. Exp. 5.7% (Prev. 4.9%).

- EU S&P Global Construction PMI (Jun) 42.8 (Prev. 43.7).

- German S&P Global Construction PMI (Jun) 44.8 (Prev. 42.4).

- German Factory Orders MoM (May) M/M 1.9% vs. Exp. 1.2% (Prev. -3.8%).

Loading...