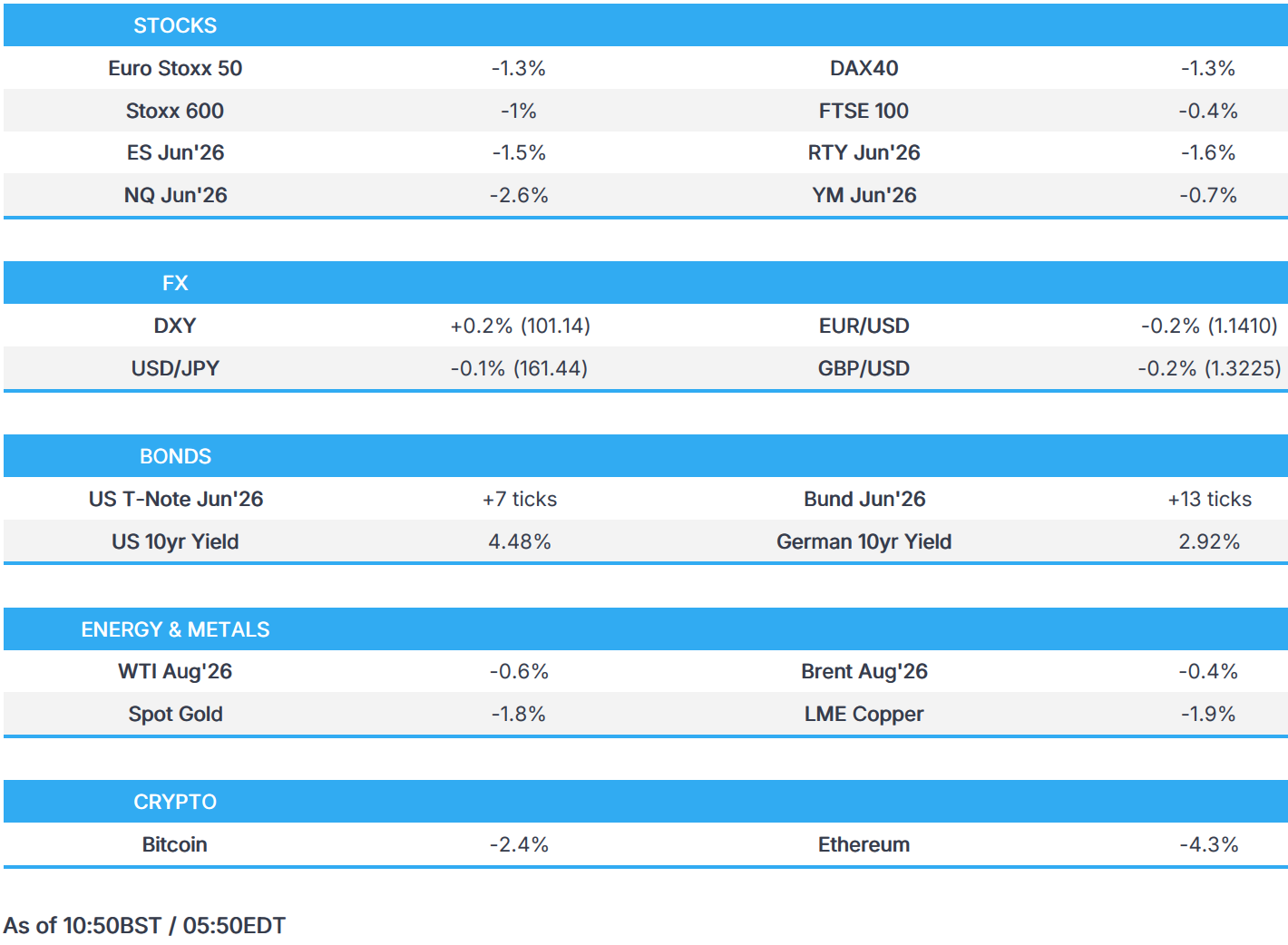

USD attracts haven demand after hefty KOSPI losses; NQ -2.5% - Newsquawk US Market Open

- Tech rout leads stocks lower; KOSPI declined c. 10%, which has weighed on the NQ -2.3%.

- Focus remains on the US-Iran situation; Brent Aug’26 -0.4%. The Lebanon-Israel situation appears to be flaring up, with recent fatalities reported in Lebanon by Israeli gunfire.

- USD attracts haven demand as tech sells off; Antipodeans underperform, GBP awaiting further Burnham/Chancellor updates.

- Fixed benefits from modest energy downside and traditional haven allure; PMI commentary points to a possible peak in price pressures.

- Looking ahead, highlights include Global Flash PMIs (Jun), US ADP Employment Change Weekly, Richmond Fed Index (Jun), BCB Minutes (Jun), NBH Policy Announcement, Speakers including ECB's Elderson & Vujcic, BoE's Taylor & Dhingra, Supply from the US, Earnings from FedEx. Note, Iranian President Pezeshkian is in Pakistan.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

Iranian Commentary:

- Iran's Foreign Ministry Spokesperson Baghaei said "if the other party does not fulfill its obligations, we should not be expected to unilaterally fulfill our obligations", Iran International reported.

- Iran's Foreign Ministry Spokesperson said defensive capabilities and missiles will never be a topic of discussion. US commitment regarding Lebanon is completely clear.

- Iran's Foreign Ministry Spokesperson said quadrilateral talks were stopped early in Switzerland due to the witnessing of US threats. Thereafter, exchanges were via a mediator, Mehr reported.

- Iran's Foreign Ministry Spokesperson said Iran has no plans to let IAEA inspectors visit nuclear sites targeted in the conflict.

- Iranian President, ahead of trip to Pakistan, said Iran is seeking the full implementation of the clauses that have been signed within the framework of international law, Nour News reported.

- Iranian Parliament Speaker Ghalibaf said the Strait of Hormuz will be administered by Iran according to international law.

- Iranian President Pezeshkian said in phone call to Turkish President Erdogan on Monday that Iran is ready to pursue diplomacy as per international law.

- Iran Central Bank Governor said Tehran is not obliged to purchase US agricultural goods under current agreements, and states that remaining frozen assets can be used to buy non-sanctioned goods beyond essential items, according to Tasnim.

- "Iranian Foreign Minister Abbas Araghchi will visit Baghdad next Sunday", Al Mayadeen reported citing sources; The meeting will include a briefing on the progress of the talks in Switzerland and the preparations.

- Iranian Foreign Ministry said "America has issued the necessary license for the sale of Iranian oil and petrochemical products", Al Jazeera reported.

- Iranian Ambassador to the UN said any further attacks on Lebanon would be a red line.

- Iranian Ambassador to the UN said Hormuz talks will be held with Oman.

- Iranian Ambassador to the UN said there has been good progress in negotiations with the US.

- "Sources indicate that the Iranian Foreign Minister [Araghchi] will hold separate talks with Pakistani officials", Al Hadath reported.

- Oman's Foreign Minister said Iranian negotiators reaffirmed their commitment to international law and to ensuring safe, toll-free passage through the Strait of Hormuz.

- Oman's Foreign Minister meets with Iranian Parliamentary Speaker Ghalibaf, with the officials discussing regional stability and Strait of Hormuz.

- Shipping data cited by Al-Arabia showed at least 20 ships have crossed the Strait of Hormuz in the past 24 hours.

Lebanon/Israel:

- One person reportedly killed by Israeli gunfire in a southern Lebanese town, according to Lebanese Civil Defense and a security source - timing unclear.

- Senior US official tells Al Jazeera that talks between Lebanon and Israel will continue to advance comprehensive peace and a security agreement between the two countries.

- Israeli National Security Minister Ben-Gvir said Israel must act alone against Iran's nuclear program and must maintain military freedom in Lebanon, hopes withdrawal from southern Lebanon will not happen and will do everything to convince PM Netanyahu.

- Israel military shells and fires at Khan Yunis in Gaza, according to Fars News Agency.

- Israel's PM, Defence Minister and Military Chief said Israeli military will continue to act to neutralise threats to soldiers and citizens, demolish terrorist infrastructure, and maintain security zone in southern Lebanon, according to a joint statement. Israel's leadership reaffirms that the security of Israeli citizens and IDF troops will remain its overriding priority, with no room for compromise.

- Israeli forces reportedly violate Syrian territory, conducting house searches in southern outskirts of Quneitra governorate.

US-Iran deal:

- US-Iran technical talks in Burgenstock had a "breakthrough", talks proceed seemingly in a positive direction, Journalist Mallick reported.

US Commentary:

- US President Trump, on Israel and Lebanon, said "we'll take a look at it"; said he gets problems solved fast, including with Israeli PM Netanyahu.

- US President Trump said if Iran doesn't stick to agreement, he will do what he has to do. As long as Iran respects us, we are not going to have any trouble. Could restart the blockade quickly if needed.

EUROPEAN TRADE

EQUITIES

- Large losses in Kospi (-9.9%) crept through to Europe (STOXX 600 -1%) with EU tech leading the losses. No specific headline driver for overnight losses in a typical non-conflict risk-off move (stocks/oil down, fixed/havens bid). As you would expect, South Korean heavyweights Samsung and SK Hynix (which account for over 50% of the index) led the declines, both falling 12%. Some analysts point out the mechanical rebalancing from leveraged ETFs exacerbated losses with a large share of the vehicle used to gain Kospi exposure coming as leveraged ETFs. Others point out positioning into Micron earnings due after the close on Wednesday.

- Given the above, Tech is the worst sectoral performer (bar Basic Resources), the sector posting losses in excess of 3%. The highest weighted chip constituents ASML -5% (Highest weighted in Europe+Tech Sector), Prosus -2.1% and STMicroelectronics -7.3%. For Basic resources, the sector has been dragged lower by declines in metals (Gold -2.5%, Silver -5.5%).

- US equity futures are also downbeat and conforming to losses seen across the pond. NQ leads declines given tech losses, ES and RTY post similar losses, faring better than the tech heavy index.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- G10s are entirely lower against the Buck (bar JPY), as USD attracts haven demand in a textbook risk-off market move (stocks/oil down, fixed/havens bid), signalling the market is gradually moving away from geopolitical trade. As you would expect, Antipodeans underperforms, Aussie fares the worst as metals suffer from the strong Buck, while JPY is the only currency stronger vs the USD after a sharp 30pip move lower as it sits towards 2024 highs.

- DXY firmer by 0.2% as it attracts haven demand amid tech weakness in Kospi/NQ (see equities at 09:25 BST for analysis). In terms of domestic newsflow, Fed's Goolsbee said services inflation was “a little disturbing”. The data docket is light but begins to pick up today (ADP weekly + PMIs due) heading into Thursday's GDP revisions and PCE data. DXY surpassed Friday’s high of 101.12, now looks to the May peak just below 102.

- JPY continues to whipsaw around multi-year lows against the Buck, with USD/JPY towards 161.50-162. Japanese officials continue attempts to bolster the Yen, but continue unsuccessful with the Greenback bid. Overnight, Japanese Finance Minister Katayama confirmed she spoke with US Treasury Secretary Bessent on Monday. Elsewhere, APAC trade saw stronger flash PMI data and mixed results of the latest 5yr JGB auction.

- GBP is weaker and tracks the firmer Buck with participants awaiting further updates from a likely incoming Burnham premiership. Despite Gilts continuing to outperform peers on optimistic Burnham reporting (Streeting added to Chancellor candidates/Burnham said to announce commitment to Fiscal rules), Miliband still in the picture for Chancellor is viewed by Sterling traders as an unwelcome option. As such, GBP awaits further press reporting and tracks the Buck with Cable remaining at 1.32, EUR/GBP unchanged. ING this morning writes “Regardless of politics, we keep favouring higher EUR/GBP on the back of a dovish view (no hikes) on the Bank of England”. EZ/UK PMIs were mixed (see fixed income for analysis), EUR saw fleeting strength on the French figure, which indicated a cooling of cost pressures; a move which proved fleeting as the German services and composite metric cooled (Some respondents' answers did not eclipse the signing of the US-Iran MoU).

FIXED INCOME

- A firmer start for fixed income as the complex benefits from the softer energy environment, though the influence of this has diminished amid recent updates from Iran, and the weak risk tone as the KOSPI closed lower by 9.9% and has weighed on European price action, with the European Tech sector lower by over 3%.

- USTs firmer by seven ticks in 109-06+ to 109-14+ confines, towards but just off highs as the mentioned energy move off lows has seemingly formed a ceiling in fixed or now at least. Ahead, we have the region’s Flash PMIs before 2yr supply. A tap that should benefit from a number of factors.

- Bunds firmer by just over 10 ticks and are just under that from the 126.74 high. Initially moving on the above, in-line with peers and with no real reaction to the latest pension reform commentary.

- The main updates, aside from the APAC moves, today have been Flash PMIs for June. Firstly, France’s figures sparked some modest EGB pressure as the components all came in firmer than expected. Internal commentary pointed to a possible peak in price pressures. Thereafter, Germany was below consensus but caveated by the majority of responses coming in before the MoU signing. Nonetheless, encouragingly, the series showed that inflationary pressures had started to ease off.

- Finally, the EZ figure was mixed and again most responses came before the MoU. But, it already showed that lower energy prices were filtering through to businesses with inputs cost rates and selling price inflation moving lower in June. Again, pointing to a potential price spike peak.

- Overall, the data chimes with those who believe that expectations for further ECB tightening are overdone. A point arguably added to by the pertinent commentary from President Lagarde on Monday. As such, upcoming hard and survey data will be scoured for confirmation that prices may have peaked which, alongside the stagnation in activity, may well see a dovish repricing in the period ahead.

- Gilts echoed the above, higher by 35 ticks at best and to a new WTD high of 89.19. Today’s strength also comes from reporting that Burnham will next week give a speech outlining his commitment to the fiscal rules; however, The Times briefing notes that Miliband remains in consideration to be Chancellor, a point that potentially caps any further upside.

- PMIs for the region were weak, though price commentary was also welcome and chimes with the view that the BoE is on hold for the foreseeable.

- The Netherlands sold EUR 1.98bln vs exp. EUR 1.5-2bln 3.50% 2056 DSL Bond: avg. yield 3.52% (prev. 3.51%).

- Japan sold JPY 1.9tln 5yr JGBs; b/c 3.11x (prev. 3.22x), average yield 1.905% (prev. 2.024%).

- Germany sells EUR 3.807bln vs exp. EUR 5bln 2.50% 2028 Schatz: b/c 1.90x (prev. 1.58x), average yield 2.57% (prev. 2.59%), retention 23.86% (prev. 22.80%)

COMMODITIES

- Geopolitical newsflow remains focused on the US-Iran talks, and the sometimes mixed commentary filtering out from the respective officials. As it stands, there does not appear to be any cause for concern, with President Trump and VP Vance both sounding positive about the initial talks; the Iranian side also said good progress has been made. However, looking between the lines reveals some contradictory remarks. On Monday, VP Vance said that Iran would allow the IAEA to inspect nuclear facilities. However, Iran’s Foreign Ministry Spokesperson stated that there are no plans to let inspectors visit nuclear sites targeted in the conflict; the nuance of “sites targeted in the conflict”, potentially offers some hints to the inner workings of the proceedings between the US and Iran. Do note that the Iranian President is visiting Pakistan today.

- The biggest risk to the talks is Israeli actions in Lebanon. Several high-ranking Israeli officials have suggested that Israel will continue its military operations in Lebanon. Comments which come ahead of the US-mediated Lebanon-Israel talks, which are set to begin today. A confab which spans over a couple of days, and focuses on finalising “pilot zones” within southern Lebanon and long-lasting peace.

- Crude benchmarks traded sideways for much of the APAC session, before then moving to lows heading into the European cash open. Since, WTI and Brent have bounced a touch off lows, to currently trade towards the mid-point of the days range. In more detail, WTI Aug’26 (-0.5%) sits within a USD 72.48-74.45/bbl range and Brent Aug’26 (-0.6%) holds within a 76.43-78.23/bbl range.

- Spot gold (-2%) extends lower amidst the continued hawkish mood in markets, which have kept the USD elevated. For gold specifically, a number of sell-side banks have cut their price forecasts for spot gold. On Monday, Goldman Sachs cut their year-end target to USD 4,900/oz (prev. USD 5,200/oz). Its model focused on the Fed, whereby every 50bps worth of easing adds c. USD 120/oz of support to spot gold. Most recently, Deutsche Bank cut its gold forecast by 22%. Today, the yellow metal holds at the bottom end of a USD 4,091 to 4,198/oz range; it may find support at a recent low of USD 4,023/oz, if the pressure continues.

- Base metals follow the downbeat risk tone seen across broader markets. 3M LME copper is lower by c. 1.8% and holds within a USD 13,396.35-13,671/t range.

- Rabobank lowers its Q3 Brent price forecast to USD 79/bbl (from USD 103/bbl), and Q4 to USD 78/bbl (from USD 93/bbl); sees Brent averaging USD 74.50/bbl in 2027, and USD 71/bbl in 2028.

- US Department of Agriculture reported a new case of screwworm in a Texas goat, taking total number of domestic detections to 16 cases.

- US strategic oil reserves fall by 9.1mln barrels to 331.2mln barrels and are at the lowest levels since 1983.

NOTABLE EUROPEAN HEADLINES

- German Chancellor Merz outlines his support for a capital-based pension system, saying it "strengthens the system".

- German Chancellor Merz confirms plan to push forward with all pension reform proposals.

- Britain’s biggest business lobby group, CBI, said UK firms are not seeking another Brexit referendum and have little interest in rejoining a customs union with the EU, according to FT.

- UK's Burnham will seek to soothe markets as he marches on number 10 and will use a speech next week to pledge to grow the economy and commit to Labour's fiscal rules, according to The Times. Burnham is considering Miliband, Streeting and Mahmood for Chancellor.

NOTABLE EUROPEAN DATA RECAP

- UK S&P Global Composite PMI Flash (Jun) 49.4 vs. Exp. 50.6 (Prev. 49.7).

- UK S&P Global Services PMI Flash (Jun) 48.7 vs. Exp. 50 (Prev. 49.3, Low. 49.0, High. 51.5).

- UK S&P Global Manufacturing PMI Flash (Jun) 53.1 vs. Exp. 53.6 (Prev. 53.9, Low. 52.0, High. 54.5).

- UK grocery inflation was 3% (prev. 3.1%) in the four weeks to June 14th.

- EU S&P Global Services PMI Flash (Jun) 48.9 vs. Exp. 48.1 (Prev. 47.7).

- EU S&P Global Manufacturing PMI Flash (Jun) 51.3 vs. Exp. 51.2 (Prev. 51.6).

- German S&P Global Manufacturing PMI Flash (Jun) 50.0 vs. Exp. 50 (Prev. 50.1).

- German S&P Global Services PMI Flash (Jun) 46.8 vs. Exp. 48.7 (Prev. 48.1).

- French S&P Global Manufacturing PMI Flash (Jun) 50.7 vs. Exp. 50.4 (Prev. 49.7).

- French S&P Global Services PMI Flash (Jun) 47.4 vs. Exp. 45.9 (Prev. 44.3).

- French S&P Global Composite PMI Flash (Jun) 47.6 vs exp. 46.0 (prev. 44.9).

- French Business Climate Indicator (Jun) 94 (Prev. 94).

- French Business Confidence (Jun) 100 (Prev. 102).

CENTRAL BANKS

- Fed's Goolsbee (2027 voter) said inflation is well above target and going the wrong way, adds need evidence this inflation is temporary and services inflation is a little disturbing. said:. We haven't had stagflation shock, and the job market has been stable. Fed Chair Warsh's approach is let's have less speculation about rates, less forward guidance, while Goolsbee said he is pretty sympathetic to that approach.

- ECB's Kazimir said they are data-dependent, but the direction for policy is clear.

- ECB's Lane said that inflation risks being above 2% for some time; increase in energy prices is expected to keep inflation well above target into H1'27. Remains attentive to both sides of the outlook. Energy shock is feeding through to broader inflation. labour market resilience, solid household balance sheets and public investment should support activity.

- ECB's Escriva said service-sector inflation is showing very strong persistence.

NOTABLE US HEADLINES

- US President Trump posted that they are preparing lawsuits against ABC for false reporting, citing the description of vandalism that took place at the Reflecting Pool in Washington, D.C. Full post: "In describing the Vandalism that took place at the Reflecting Pool in Washington, D.C., ABC FAKE NEWS, one of the worst in the business, even paying me $16,000,000 for past bad and inaccurate reporting, failed to report that their close “friends,” Dumocrats Obama and Biden, spent over 100 Million Dollars on the Reflecting Pool, and it never worked. In fact, it was rarely open do to leaks and “stench.” They wanted to spend 300 to 400 Million Dollars, but just let it ROT. I spent approximately 16 Million Dollars, and it came out great, except for the Vandalism, which we are now fixing. It was also a much bigger job than originally envisioned, including the outer areas and sidewalks. We are preparing lawsuits against ABC for false reporting. I like their money, which will be given to the U.S. Treasury! Thank you for your attention to this matter. President DJT".

- US Senate passes bipartisan affordable housing bill.

GEOPOLITICS

RUSSIA-UKRAINE

- Russia and Ukraine may swap Prisoners of War soon, TASS reported.

- Ukraine's capital Kyiv issues an air raid alerts and authorities ask people to seek shelter.

OTHERS

- North Korea leader Kim Jong-un said North Korea will further assert its status and role as a nuclear power, adds will accelerate broader plans, enhance nuclear arms technology and develop water deterrence capabilities. accused US and South Korea carrying out the most dangerous provocations through nuclear war machinery. To accelerate building of 10,000-ton strategic guided missile cruiser.

- China's Beihai Maritime Safety Administration announced that parts of the Beibu Gulf will be closed to navigation due to military training from 11:00-12:00 Beijing time on June 23rd.

CRYPTO

- Bitcoin is on the backfoot this morning, following the downbeat sentiment seen across global markets; BTC holds around USD 62k.

APAC TRADE

- APAC stocks were subdued with initial choppy price action following the mixed performance stateside, where participants reflected on the progress in US-Iran talks, but communication stocks and the Nasdaq Comp underperformed. KOSPI, -6.9%, led the sell off, moving to a test of 8.5k to the downside.

- ASX 200 traded little changed for most of the session amid a lack of major fresh catalysts overnight and as the strength in financials and defensives offset the losses in the tech and commodity-related sectors.

- Nikkei 225 swung between gains and losses with the index briefly climbing to a fresh record high before reversing course, and is on track to snap its 8-day win streak.

- Hang Seng and Shanghai Comp conformed to the lacklustre mood in the region and the absence of any major fresh catalysts, with the Hong Kong benchmark pressured by losses in miners, and digital platforms stocks amid a rotation out of hyperscalers into semiconductors.

NOTABLE ASIA-PAC HEADLINES

- China's MOFCOM announces measures to stimulate the auto after-sales market; to support the integration and upgrading of the car rental industry.

- Japanese Chief Cabinet Secretary Kihara said will take appropriate action against FX moves if needed.

- Canada awarded Australia a USD 1.75bln contract for its over-the-horizon radar system, boosting Arctic early warning capabilities, and which marks Australia's largest ever defence export.

- Japanese S&P Global Composite PMI Flash (Jun) 52.50.

- Japanese S&P Global Manufacturing PMI Flash (Jun) 54.9 vs. Exp. 54.5 (Prev. 54.5).

- Australian S&P Global Manufacturing PMI Flash (Jun) 51.2 (Prev. 50.7).

- Blackstone (BX) President and COO Gray told Nikkei that the firm plans to invest USD 30bln in Japanese data center development over the next three to five years.

NOTABLE APAC DATA RECAP

- Japanese BoJ Core CPI (May) 2.7% (Prev. 2.8%).

- Japanese S&P Global Services PMI Flash (Jun) 51.8.

- Indian HSBC Services PMI Flash (Jun) 57.3 (Prev. 59.8).

- Indian HSBC Composite PMI Flash (Jun) 57.4 (Prev. 59.3).

- Indian HSBC Manufacturing PMI Flash (Jun) 54.5 (Prev. 55.0).

- Australian S&P Global Services PMI Flash (Jun) 49.9 (Prev. 48.7).

- Australian S&P Global Composite PMI Flash (Jun) 49.8 (Prev. 48.7).

Loading...