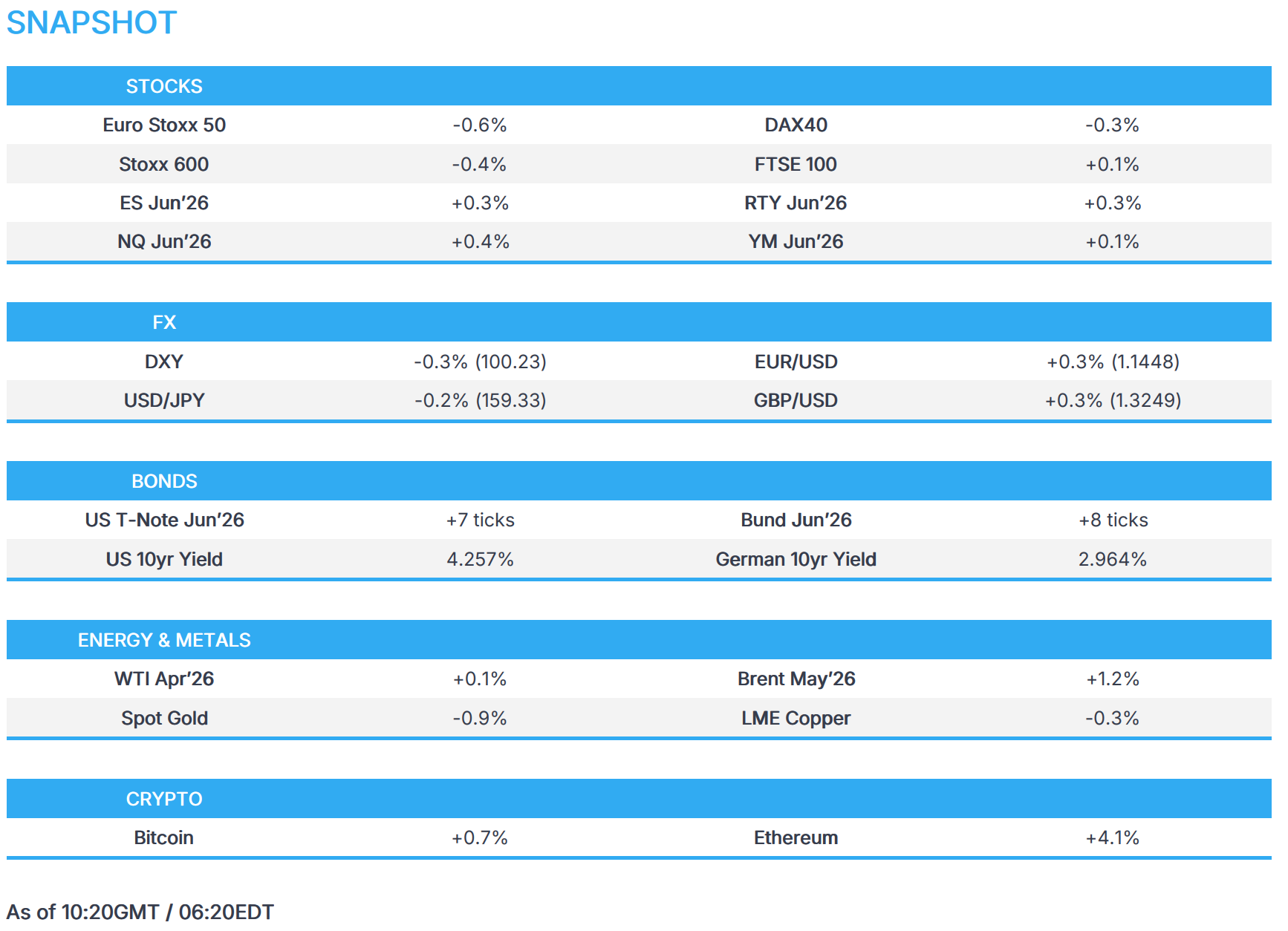

WTI underperforms as US urges faster output; US equities gain while DXY pulls back - Newsquawk US Market Open

- US President Trump said he ordered a strike that wiped out every military target on Kharg Island, where Iran exports nearly all of its oil, but left the oil infrastructure intact; Crude holds around USD 100/bbl.

- US President Trump’s administration plans as soon as this week to announce a coalition to escort ships through the Strait of Hormuz, although they are still discussing if such operations would begin before or after hostilities have ended, WSJ reported.

- Trump also said he was expecting China to help unblock the Strait of Hormuz before he travels to Beijing, while he stated that he may delay the trip but didn't say for how long, according to FT.

- European equities mixed, CBK GY gains following UCG IM takeover bid; US equity futures rebound.

- DXY subdued, G10s tilt higher, Antipodeans outperform ahead of expected RBA hike.

- Fixed income muted ahead of a busy week of central bank announcements.

- Looking ahead, highlights include Canadian CPI (Feb), US Industrial/Manufacturing Output (Feb), and comments from NVIDIA (NVDA) CEO Huang.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses are mixed to start the week as the Middle East conflict remains the dominant macro theme. The FTSE 100 outperforms as oil majors gain with crude above USD 100/bbl, while the FTSE MIB lags after Amplifon declines on news it will acquire GN Store Nord’s hearing unit for DKK 17bln.

- European Sectors are also mixed. Energy leads as Brent holds above USD 100/bbl, with Real Estate also firmer as Segro gains following a broker upgrade and UK Rightmove house prices rise M/M. Basic Resources initially underperformed as spot gold dips below USD 5,000/oz, while Banks remain pressured.

- US equity futures trade firmer (ES/NQ/RTY +0.3-0.4%) as a softer dollar lifts risk sentiment despite elevated crude prices, with the DXY easing from YTD highs, although traders look ahead to the FOMC on Wednesday.

- UniCredit (UCG IM) has launched a voluntary exchange offer for Commerzbank (CBK GY) but does not expect to achieve control. Offer looks to exceed the 30% stake. Offer represents a EUR 30.80/shr price, a 4% premium.

- AMD (AMD) and Samsung (005930 KS) are reportedly in negotiations on a contract for AMD to allocate volume to Samsung's leading-edge foundry process, edaily reported citing sources. "Industry sources indicate that the visit will cover discussions on long-term supply agreements spanning commodity DRAM and NAND flash in addition to broader memory categories".

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is marginally softer as the index takes a breather after reclaiming the 100.00 level, while traders brace for a heavy central bank week and monitor Middle East tensions. US President Trump is reportedly seeking a coalition to reopen the Strait of Hormuz and weighing the seizure of Iran’s Kharg Island, while also warning NATO and calling on China to help secure the waterway. DXY trades in a narrow 100.18–100.48 range after Friday’s 99.59–100.54 band. The FOMC is widely expected to leave rates unchanged at 3.50–3.75% on Wednesday, with markets not pricing a cut until Q4 2026.

- EUR/USD rebounds from around a seven-month low amid the softer dollar but remains below 1.1500 (1.1414–1.1456 range) amid quiet Eurozone newsflow and geopolitical uncertainty. The pair remains within Friday’s 1.1411–1.1530 range. The ECB is expected to keep rates unchanged at 2.0% on Thursday, though higher energy prices have pushed market pricing slightly more hawkish, with a 25bp hike now fully priced by year-end.

- GBP/USD edges higher alongside the weaker dollar after recently hitting a year-to-date low. UK ministers are set to announce a GBP 50mln support package for households facing the energy shock from the Iran conflict, while the UK is also exploring an EU tuition fee cut to reset post-Brexit relations. The BoE is expected to keep the Bank Rate at 3.75% on Thursday, though energy-driven inflation risks have prompted a more hawkish repricing.

- USD/JPY is choppy in the absence of Japanese data, with comments from Japanese Finance Minister Katayama stating authorities are ready to take decisive FX steps if needed. The pair trades within 159.17–159.75, inside Friday’s 159.01–159.76 range. The BoJ this week is expected to keep rates unchanged at 0.75%, although markets still price a possible hike by June.

- Antipodeans outperform. NZD/USD leads gains despite mixed domestic data, while AUD/USD reclaims the 0.7000 level ahead of the RBA decision tomorrow, where the central bank is widely expected to deliver another rate hike.

FIXED INCOME

- USTs are slightly firmer as Treasuries digest the weekend’s modest geopolitical escalation and higher energy prices. Futures trade in a narrow 111-12+ to 111-21+ range, but remain near recent lows at the bottom of March’s 111-11 to 114-06 band and close to the January and February troughs of 111-06+ and 111-08+ as markets await a busy central bank week.

- Bunds edge higher in quiet trade, with gains of around nine ticks in narrow sub-20 tick ranges. Focus in Europe centres on energy-related meetings this week, including a press conference later today that could discuss EU-wide measures to stabilise energy markets and updates on proposals for a “coalition of the willing” to reopen the Strait of Hormuz.

- Gilts outperform after gapping higher by 26 ticks and extending gains to an 88.84 peak, leaving futures up just over 30 ticks at best. The move reflects partial recovery after Gilts had previously underperformed peers during the Middle East-driven energy shock.

COMMODITIES

- Crude Futures extend gains as markets digest weekend escalation in the Iran conflict and fresh risks to regional energy infrastructure. WTI trades above USD 100/bbl within a USD 96.74–102.44/bbl range, while Brent hovers around USD 105/bbl (USD 102.04–106.50/bbl), however WTI narrowly underperforms Brent futures on news US called for oil producers to increase output to combat surging global energy prices. The US conducted strikes on military targets on Iran’s Kharg Island, from where most Iranian oil exports originate, though oil infrastructure was left intact. Prices also rise after reports the UAE’s Fujairah port was struck with loadings suspended, while Saudi Crown MBS reportedly urged Washington to maintain military pressure on Iran. Meanwhile, Trump says China should help reopen the Strait of Hormuz ahead of a planned Beijing visit.

- Nat Gas is firmer alongside the broader energy complex as geopolitical risks underpin prices, with front-month Dutch TTF near EUR 52/MWh.

- Spot Gold is flat in choppy trade within a USD 4,967.77–5,036.01/oz range as the metal tracks USD movements while traders monitor oil-driven inflation risks ahead of a heavy central bank week.

- Base Metals are softer across the board. Copper recovers from Friday’s lows but upside is capped by cautious risk sentiment. Meanwhile, Aluminium Bahrain begins a phased shutdown of Reduction Lines 1–3 (around 19% of its 1.62mln-tonne annual capacity) in response to the effective closure of the Strait of Hormuz.

- Senior US administration official acknowledges that prices will continue to rise but admits there is little the government can currently do at the moment, according to a CNN reporter.

- Oil executives warned the Trump administration the energy crisis will likely worsen and that the closure of the Strait of Hormuz might push up oil prices further, according to WSJ.

- Morgan Stanley lifts its Brent price forecasts as far out as H2-2027. USD/bbl. Q2-2026 110.00 (prev. 80.00). Q3-2026 90.00 (prev. 70.00). Q4-2026 80.00 (prev. 65.00). H1-2027 70.00 (prev. 65.00). H2-2027 70.00 (prev. 65.00).

TRADE/TARIFFS

- US and Chinese officials held candid and constructive talks in Paris on Sunday and agreed to enhance stability in the trade relationship, according to sources familiar with the talks, while the sides met for six hours and will resume talks on Monday. US Treasury Secretary Bessent and USTR Greer raised the need for China to buy more Boeing aircraft, US coal, oil and gas, while US and Chinese officials discussed solutions to difficulties faced by some American firms in obtaining rare earths. Talks will continue on a technical level on Monday.

- China responded to US allegations of forced labor in the Section 301 probe and has lodged a formal representation with the US over the investigation.

- Indian Trade Secretary said the US-India trade deal will be signed when the US re-establishes global tariff rates. The US is working on recreating global tariff architecture.

- Indian Trade Secretary said exports to West Asia have been impacted by the Middle East situation; India is considering measures to support exports to the Middle East.

NOTABLE EUROPEAN DATA RECAP

- Swiss Sight Deposits (w/e 13th Mar), CHF: Domestic 433.5bln (prev. 428.8bln), Total 454.4bln (prev. 454.07bln).

- UK Rightmove House Prices YY (Mar) -0.2% (Prev. 0.0%).

- UK Rightmove House Prices MM (Mar) 0.8% (Prev. 0.0%).

CENTRAL BANKS

- Fed Chair nominee Warsh does not have a confirmed hearing scheduled in the Senate Banking Committee, Semafor reported citing sources.

GEOPOLITICS

MIDDLE EAST

- US President Trump said he ordered a strike that wiped out every military target on Kharg Island, which is where Iran exports nearly all of its oil from, but left the oil infrastructure intact which he would reconsider if Iran interferes with the safe passage of ships in the Strait of Hormuz.

- US President Trump said he is hearing that Iran’s new Supreme Leader Khamenei may be dead, and that it is not clear if Iran has laid mines in the Strait of Hormuz, while he also stated that he is not ready to make a deal with Iran because the terms aren’t good enough yet. Furthermore, Trump said recent strikes on Kharg Island demolished most of the island and commented that they “may hit it a few more times just for fun”.

- US President Trump posted that they have destroyed 100% of Iran’s military capability and that many countries will send warships to help keep the Strait of Hormuz open and safe.

- US President Trump said they have had strong results in Iran and he does not believe Iran is ready to negotiate, but will be ready to negotiate at some point. Trump also said the US is talking to other countries about policing the Strait of Hormuz and cannot say which countries will help yet, while a few countries would rather not get involved. Furthermore, he called on NATO to help and thinks China should come in to help on the Strait of Hormuz.

- US President Trump seeks a Hormuz coalition and is weighing seizing Iran's critical oil depot on Kharg Island — a move that would require US boots on the ground — if tankers remain bottled up in the Persian Gulf, according to US officials cited by Axios.

- US President Trump warned that NATO faces a very bad future if US allies fail to assist in opening up the Strait of Hormuz, according to FT.

- US lawmakers have begun talking about a supplemental funding bill for the Iran war, Punchbowl reports; package could have a USD 100bln or greater price tag, according to sources.

- Israel's IDF has launched a focused ground operation in southern Lebanon, including a build-up of forces in order to capture more forward lines, N12 reported.

- Israeli Home Front notifies of a missile attack from Iran targeting areas in central Israel.

- Iran's Foreign Minister Araqchi says no messages have been exchanged with the US and that Tehran has not asked for a ceasefire as the "war needs to end in a way that ensures it does not happen again".

- Iran's Foreign Ministry Spokesperson Baghaei says parties not involved in the war have had vessels pass through Hormuz with coordination and permission from Iran's military. The Strait of Hormuz is only closed to the enemies of Iran.

- The Iranian Army Spokesperson said the support centre of the USS Ford in the Red Sea are considered as targets, Al Arabiya reported.

- Iran's media operations centre warns residents in specific areas of Dubai and Doha of possible attacks in the coming hours, while it stated that US military personnel are hiding in locations in Doha and Dubai and urges residents to evacuate immediately.

- Oil loading at UAE's Fujairah suspended after the port was hit, Bloomberg sources report.

- UAE's Fujairah port was hit and the damage is being assessed, Bloomberg reported citing sources.

- Multiple locals are said to confirm smoke rising in the vicinity of Dubai International Airport, but it is unclear what has been targeted, according to Faytuks News.

- Explosions heard in Bahrain's skies as air defences intercept an Iranian attack, according to Sky News Arabia.

- Missile bombardment targets US military base for logistical support at Baghdad airport, according to Al-Haddath.

- The meeting of European foreign ministers will discuss the protection of sea lanes and the Strait of Hormuz, Al Jazeera sources report.

RUSSIA-UKRAINE

- Russia's Kremlin says we are open to continuing Ukraine negotiations and that US President Trump has not lost interest, instead he recommended Ukrainian President Zelensky make a deal

CRYPTO

- Bitcoin briefly extends above USD 74k but has since come off best levels.

APAC TRADE

- APAC stocks mostly declined amid cautiousness at the start of a busy week of central bank activity and following the continued conflict after the US struck military targets in Iran's Kharg Island oil export hub, but left oil infrastructure intact.

- ASX 200 was led lower by mining, materials, resources and tech, while the RBA kicked off its two-day policy meeting, where the central bank is widely expected to hike rates for the second consecutive meeting amid inflationary pressures.

- Nikkei 225 retreated amid losses in utilities and electric names due to the ongoing energy-related uncertainty, despite Japan beginning its emergency oil release, while the Japanese data calendar is quiet to start the week, but begins to pick up on Tuesday, and the BoJ are also set to conduct a policy meeting later in the week.

- Hang Seng and Shanghai Comp were mixed as participants digested stronger-than-expected activity data for China, and with US-China trade talks in Paris on Sunday said to be constructive and will resume today. However, there were also comments from US President Trump, who called for China to help open the Strait of Hormuz and suggested a potential delay to the Trump-Xi summit scheduled later this month.

NOTABLE ASIA-PAC HEADLINES

- China's stats bureau's spokesperson expects consumption to rise steadily this year as policy measures gain traction, but noted that more support is needed.

- Japanese Finance Minister Katayama said prepared to take decisive steps on FX.

NOTABLE APAC DATA RECAP

- Indian WPI Inflation YoY (Feb) Y/Y 2.13% (Prev. 1.81%).

- Chinese Retail Sales YoY (Jan-Feb) Y/Y 2.8% vs Exp. 2.6% (Prev. 0.9%).

- Chinese Industrial Production YoY (Jan-Feb) Y/Y 6.3% vs Exp. 5.3% (Prev. 5.2%).

- Chinese Fixed Asset Investment (YTD) YoY (Jan-Feb) Y/Y 1.8% vs Exp. -5.0% (Prev. -3.8%).

- Chinese Unemployment Rate (Feb) 5.3% (Prev. 5.1%).

- Chinese House Price Index MM (Feb) -0.3% (Prev. -0.4%).

- Chinese House Price Index YoY (Feb) Y/Y -3.2% (Prev. -3.1%).

- New Zealand Composite NZ PCI (Feb) 50.5 (Prev. 52.5).

- New Zealand Services NZ PSI (Feb) 48.0 (Prev. 50.9, Rev. From 50.7).

Loading...