This is a follow up of my last article, Beijing's Green Light, which speculated that China would be forced into stimulating consumption in response to the drop-off in their export sector due to tariffs. The article looked at real comments made by Chinese authorities to ascertain what they were waiting for before deploying the long-awaited "stimulus bazooka." It argued that the beneficiaries of stimulus - Chinese consumer discretionary stocks - were grossly undervalued as a result of an unprecedented and persistent wall of Wall Street bearishness.

What the article didn't discuss was how China could stimulate, or what consumption stimulus would actually look like. The classic go-to example is welfare-like stimulus where people are literally handed money that can be used to consume, but with their fiscal deficit already at record levels, the tailwind from 'welfarism' is exhausted.

Stimulating consumption is a matter of increasing household wealth, and the low share of wealth retained by Chinese households is at least partly a result of the high share retained by the government (especially local governments). The best way for China to resolve its low domestic consumption would be to transfer wealth from local governments to the household sector - directly or indirectly.

One way this could be done indirectly is by transferring assets owned by local governments to public pensions. This would give pension funds an additional, stable dividend stream, allowing them to raise payouts and reduce the burden on contributors. Crucially, it hardwires state-owned capital into household income rather than rerouting it through discretionary government budgets. That difference is what makes it a true structural shift - it reallocates the returns from investment-oriented state spending to direct support for consumption, effectively transferring wealth from the public sector to the private sector without printing a single yuan.

Reconfiguring their economy this way won’t be easy, but it's China’s only path to sustainable growth. It will also be explosive: a robust Chinese household sector that retains a greater portion of total wealth and has a stronger consumption footprint is a completely new paradigm, one that Beijing is now exploring.

Rock-bottom yields on Chinese government bonds, which as Kyle Bass correctly notes are a reflection of a lackluster economy that has struggled to recover since Covid, give the PBOC little room for monetary easing like QE absent a massive 2020-like shock. The central bank has signaled support and made some tweaks since my last article but nothing significant.

On April 25th, the Chinese National Financial Regulatory Administration (NFRA, the preeminent oversight authority) published a notice allowing insurers to lower the guaranteed minimum interest rate during periods of falling market rates - breaking previous contractual guarantees of fixed returns. Life insurers are huge owners of sovereign bonds, so their payout is tied to bond yields. The move can be interpreted as the authorities expecting a continued decline in bond yields/returns, and hints at no large-scale monetary easing in the near term.

So big monetary easing can be ruled out. What about big fiscal easing?

Tax revenue as a share of GDP is already quite low in China (suspiciously low, in fact, but that's not relevant right now), so MOF officials necessarily run a fiscal deficit. Beijing doesn't like currency volatility, so there is a limit on how much money can be printed for additional stimulus in the near term. Like I noted in Beijing's Green Light, the Chinese fiscal deficit is already projected to reach a record high in 2025, and far more when accounting for local government deficits:

The concept of stimulating consumption is normally thought of as tax cuts, fiscal spending and "welfare," all of which increase the fiscal deficit. But a recent speech on the topic from Liu Shijin - an esteemed economist and former State Council authority who was cited in my last article - at the Parallel Forum of the 2025 CF40 Annual Conference, suggests another approach that bypasses these channels, could totally recalibrate the Chinese economy and would reshape its global footprint, something which Liu argues is the inevitable next step.

The speech's English translation is here. Liu begins by lamenting how China's consumption share of GDP is not only low, but unacceptably low:

"I want to emphasize a concept here: China's insufficient consumption is not an acceptable deviation from international average levels, but a significant gap of 20 percentage points, which can be described as a 'structural deviation.'"

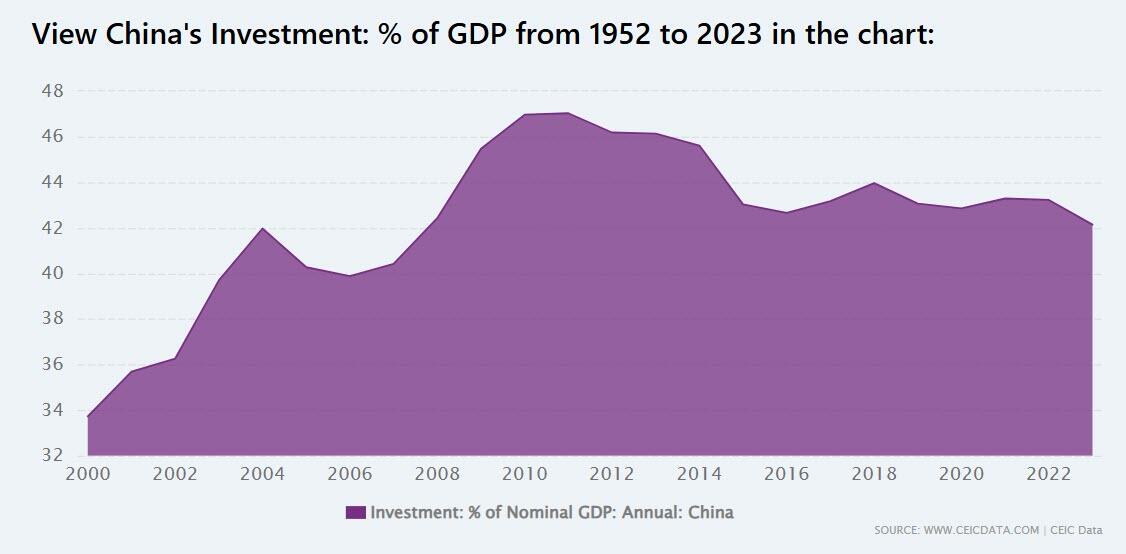

Consumption is important to Beijing, and thus to economists like Liu, because GDP growth in an economy is, very simply, a product of consumption + investment + fiscal spending + net exports, and China has set ambitious growth targets that officials are keen on maintaining (it's all they seem to talk about). Their exports may slow for obvious reasons, and their fiscal deficit is already the biggest on record. There are three areas of investment - property, infrastructure and manufacturing - that the authorities could stimulate but, as I explained last month, Beijing is reluctant to do this.

By process of elimination, that leaves a rise in consumption to make up for a slowdown in exports.

Liu addresses four things he sees as the root cause of China's "structurally" low consumption, like wealth inequality and poor public services. Of the four causes Liu names, the most compelling is the government’s oversized share of national wealth:

"...at the beginning of reform and opening up (December 1978), the government sector's wealth accounted for nearly 90% of society's total wealth. Although this has gradually decreased, in recent years it has stabilized at around 40%. In OECD (Western) countries, this proportion is usually lower, fluctuating around 5%...

This shouldn't come as a surprise in a system where the state still commands the heights of the economy through large state-owned enterprises (SOEs) in strategic sectors like banking & semiconductors, heavy direction of credit & investment, and a central role in land ownership, capital allocation and top-down economic planning. What's revealing is how Liu, and other speakers/economists, compare the Chinese system to OECD systems in the West when just a couple years ago those very systems were derided by the authorities as "lazy" and unproductive.

"...China's high savings rate and low consumption rate are related to the significantly high proportion of government net assets and state-owned equity capital in society's total net assets. This characteristic was advantageous when we were in the industrialization or investment-driven stage, but now that this stage has passed and the problem of insufficient consumption shows a structural deviation, we face a choice: should government net wealth and state-owned capital returns continue to be used for savings and investment, or should they be redirected to support consumption?

"Clearly, we need to achieve an important transformation, driving the economy from investment-driven to consumption-driven."

Acknowledging that China's industrialization stage has passed and implying that the next stage is an "important transition" towards a consumption economy is huge. Doing that by leveraging wealth held by the public sector isn't a brand new idea, however. Liu himself flagged this strategy in December:

"Liu proposed that institutional mechanisms could be introduced to channel State-owned capital into promoting consumption in areas such as education, healthcare, and social protection, while also addressing income inequality through redistribution measures.

"'Transitioning State-owned equity from primarily supporting investment to also supporting consumption would not only significantly boost consumption, but also showcase the country's capacity to mobilize resources for major initiatives,' Liu said."

But China's consumption has trailed the West's average for decades - even Liu refers to it as "structural" and thus a persistent quality. In 2010 it was closer to 30-40% lower than OECD averages. Meanwhile, their growth has obviously flourished over many of those years. In his presentation, Liu revisited why consumption is key:

"This involves the concept of 'terminal demand.' Terminal demand refers to the remaining portion of GDP after removing productive investment, including all consumption and non-productive investment. The latter mainly refers to real estate and infrastructure construction related to people's livelihoods, as well as some service investments..."

Liu continues:

"For quite a long time, real estate and infrastructure grew rapidly, showing a certain degree of advancement or overdraft in terms of per capita development level from an international comparison perspective. The rapid growth of real estate and infrastructure masked the structural deviation problem in consumption."

"However, in recent years, real estate has declined significantly, and infrastructure is also slowing down. The previously masked problem of consumption's structural deviation has been revealed, becoming the 'bottleneck' shortcoming in terminal demand. If this shortcoming is not addressed quickly, the contraction in terminal demand will lead to economic growth rate decline."

Liu is stressing that, hell or high water, consumption must be stimulated lest terminal demand, and growth, contract. You can't have "structurally" low consumption and expect to meet growth targets, he insists. Beijing is of course not oblivious to any of this - though it's not well-telegraphed, the entire sequence is very logical:

"Understanding of expanding consumption and improving people's livelihoods requires new connotations and perspectives. This not only involves social moral fairness or sympathy for the vulnerable but is also a more urgent question of whether necessary economic growth rates can be maintained.

"For a long time, we have been bold in promoting investment and launching projects, often involving hundreds of billions, thousands of billions, or tens of trillions. But the current reality is that for stabilizing growth, consumption is more important than investment. We need to use the same intensity and input previously applied to investment to now tackle consumption.

"Moving forward, correcting the structural deviation of insufficient consumption and raising consumption's proportion of GDP to a reasonable level should be a prerequisite or hard task for stabilizing growth."

"Reasonable level" is vague and subjective, but Liu compared China with OECD averages that lead by 20%. The World Bank shows consumption's share of GDP in China trails Germany by about that much. It's unlikely to catch up with consumer-oriented societies like the US, however:

Stimulating consumption is logical (and necessary according to Liu), but actually doing it is another thing. Indeed, Liu admits the problem "involves a theoretical issue worth in-depth study," but he does offer suggestions. Namely, he advocates deploying existing capital owned by the state to finance their pension system, which is typically funded with fiscal outlays. Some of you may recognize this as curiously similar to Scott Bessent's idea of "monetizing the asset side of the US balance sheet" (fund the Treasury with wealth that already exists):

"In OECD countries, there are considerable pension accumulations, while our pension accumulation scale is small, but we have such large state-owned assets. From historical evolution and theoretical analysis, a considerable portion of these state-owned assets should be pension fund accumulations for all people (including rural residents). Therefore, a significant adjustment is needed, considering transferring a large scale of state-owned capital, primarily state-owned financial capital, to urban-rural resident basic pension insurance.

"In 2023, China's total state-owned capital equity was 102 trillion yuan, and state-owned financial capital equity was 30.6 trillion yuan, totaling 132.6 trillion yuan. If 10 trillion yuan (33%) of state-owned financial capital were transferred to urban-rural resident basic pension insurance, the resulting income could increase pension levels by more than double.

"It's worth noting that this not only involves 170 million elderly people receiving pensions but also their children, with more than 300 million urban-rural resident pension insurance contributors. If future pension levels are low, precautionary savings will be high, and this group also has a higher marginal propensity to consume. Through such adjustments, a large amount of precautionary savings can be converted into real consumption capacity, directly increasing consumption demand."

Liu’s proposal works by transferring ownership of dividend-paying state-owned financial assets - such as stakes in banks or insurers - from the government to rural pensions like the National Social Security Fund. This gives the pension system a stable income stream, which can be used to raise payouts for rural and low-income payees. Higher, guaranteed pensions reduce the need for "precautionary" savings among hundreds of millions of contributors, effectively converting idle savings into real consumption. It’s a structural method to stimulate demand by turning state capital into household income - no money is printed and no debt is issued.

Of course, taking bank equity owned by the state and transferring the dividend streams to pensions is one, less aggressive example that the authorities can pilot. There are a ton of other state-owned assets that can be used - the wealth is effectively locked up for investment, but deploying it back to households would mechanically be a historic wealth transfer from the public sector & government to the private sector & households.

Whether Beijing formally adopts Liu’s blueprint remains to be seen, but the logic is clearly gaining traction at the highest levels. It will likely take years to play out completely, but the process would be recognizable from the outset - with Chinese stocks taking an explosive turn higher as they reprice doom peddled by Wall Street over the last decade. What won’t be as easy to recognize is a world where China is less defined by exports and more by consumption - and plenty of money will be caught flat-footed when it happens.

Contributor posts published on Zero Hedge do not necessarily represent the views and opinions of Zero Hedge, and are not selected, edited or screened by Zero Hedge editors.

{kind=link}