Economic Data Is Misleading

Welcome to MktContext! I am a professional money manager, trader, and investor who has been timing and beating the market for over a decade. We specialize in predicting market direction by studying the economy and market signals. Join 9,500 subscribers at MktContext.com in improving your portfolio returns — it’s free!

Financial news outlets are panicking about last Friday’s payrolls report that showed a shockingly weak gain of 73K jobs, along with massive downward revisions to prior months’ numbers. Along with this, the ISM manufacturing index showed fewer new orders, the ISM services index showed employment falling, and goods prices inflation seemed to be rising. Many quickly called this "stagflation", i.e. a situation where the economy slows while prices rise. But is that the full story?

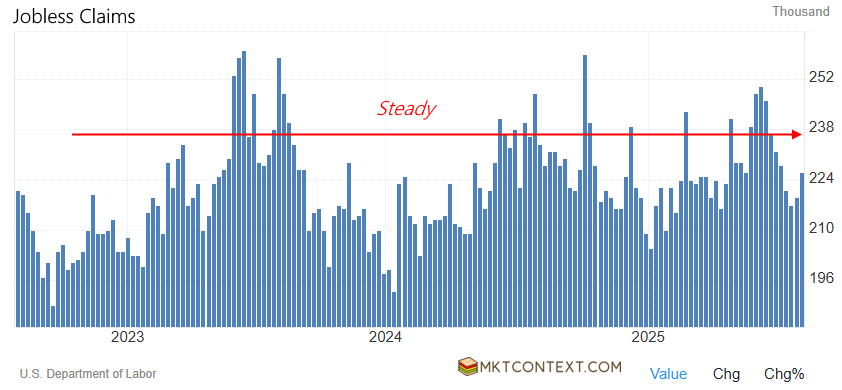

Economists are fitting the data to their prior beliefs of tariffs harming the economy. This is a red herring. The jobs data itself is not as bad as it looks; as we explained last week, the low payroll figure happened because the labor force is shrinking due to immigration restrictions. The restrictions are lowering the number of workers available. Despite this, the unemployment rate remains stable, and this week’s jobless claims data were steady, showing no rise in layoffs.

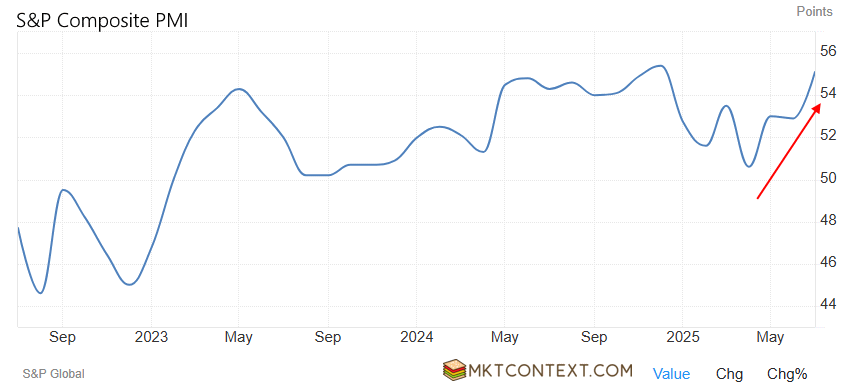

The PMI data has also been misleading. There are two main reporting bodies on PMI data: ISM and S&P Global. Lately, their signals have been diverging; ISM shows a drop, S&P shows improvement. This happens because ISM surveys larger companies that tend to worry more about trade issues, while S&P focuses more on smaller domestic companies that are doing well beneath the surface. Per the official FAQ:

ISM surveys are based on data compiled from purchasing and supply executives whereas S&P Global PMI data are based on a broader spectrum of job titles, meaning executives such as CEOs and CFOs participate in the surveys, which in practice facilitates a wider industry reach

-S&P Global explanation

S&P’s version of Composite PMI (manufacturing + services) has been in expansionary territory for well over a year. Since the April lows, it has actually been rising, showing economic strength not weakness. Does this look to you like an economy facing recession?

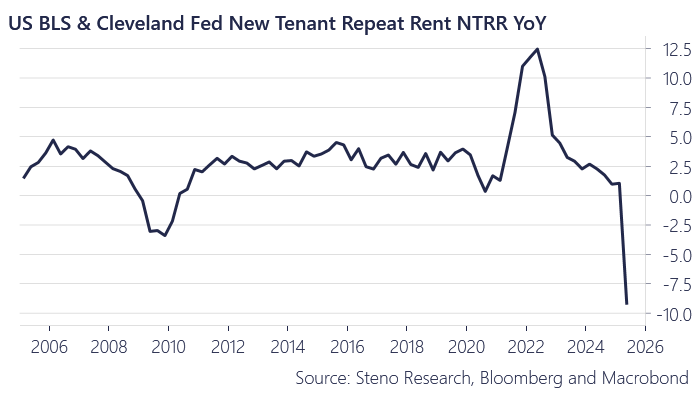

As for inflation, rent inflation is actually falling fast (chart below) along with other costs. Though goods prices are rising a bit, that is being balanced by falling services prices. Yes, tariffs have added a small inflation bump, but overall demand is dropping, which helps keep inflation from blowing out.

In short, the economic data right now can look scary if you only glance at parts of it. But a closer look shows a more nuanced picture. No recession, no inflation, and certainly no stagflation. The economy faces challenges, yes, but the story is more complex than headlines suggest.

And the million dollar question: How do we make money on this differentiated viewpoint? By remaining fully invested in growth stocks (as we are) and buying the dips when the rest of the market is panicking about weak jobs figures.

To read the rest of this article, and to see our portfolios and get more market timing content, head over to MktContext.com and subscribe today!