Fed Meddling Will Drive The Next Bubble

Welcome to MktContext! I am a professional money manager, trader, and investor who has been timing and beating the market for over a decade. We specialize in predicting market direction by studying the economy and market signals. Join 9,500 subscribers at MktContext.com in improving your portfolio returns — it’s free!

Fed In-Dependence

In the latest saga of the White House meddling in Fed affairs, Trump has fired Fed Governor Lisa Cook "for cause". The cause being alleged mortgage fraud when she applied for her home loans years ago. Trump is launching a full legal attack on Cook to remove her from office, and Cook has vowed to defend at any cost. Once Cook is replaced with Trump’s nominee, a majority of the Board will be in favor of rate cuts.

So why does Trump want to control the Fed if Powell has already agreed to cut rates? The Fed is one of the most powerful agencies for determining the trajectory of the US economy. Not only that, the Fed can print unlimited money (theoretically). That means the White House would also control budget and spending in the US, circumventing Congress. This is what Trump is really after.

There's a lot of debate amongst lawyers and economists on whether Trump has the legal authority to fire Cook. This is the wrong question to ask. The lawsuit from Trump sends a clear threat to Fed members to "fall in line or else". Even if Cook wins this fight, Fed voters will think twice about holding rates high, lest they jeopardize their careers or risk a protracted legal battle. Perhaps this is why Adriana Kugler resigned for no apparent reason.

So what are the market implications? Assuming Trump is able to wrest control of the Fed and enact aggressive rate cuts (we're talking 200bps or more), we could potentially get a huge injection of stimulative monetary policy. The economy would run hot, driven by easy financial conditions and money supply expansion. Leverage in the financial system would rise thanks to lower rates. We could also get a deregulation of bank balance sheets that leads to a credit and lending boom. It would drive an asset bubble of epic proportions.

Are we expecting this outcome? No. At least not yet. But it is crucial to remember that when the Fed eases into an already frothy environment, the result is usually bullish. Historically speaking, rate cuts outside of recessions tend to be very positive for risk assets. Therefore the bar is much higher to sell this market.

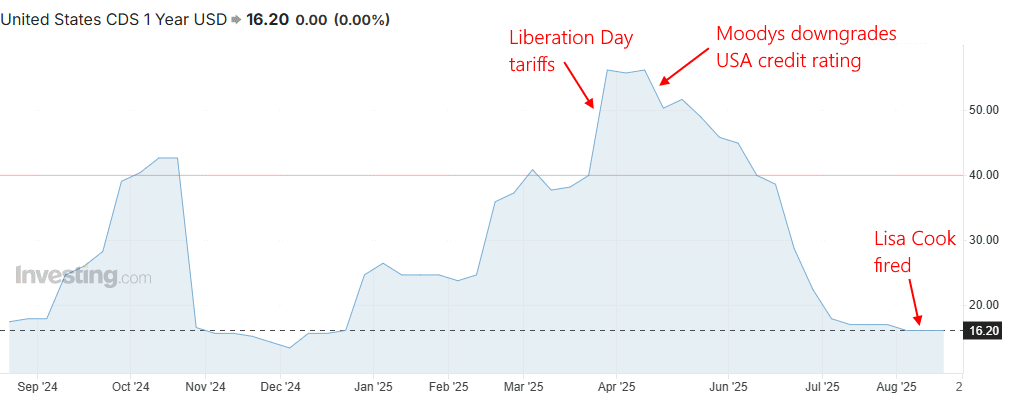

P.S.: For anyone who thinks the loss of Fed independence is an end-of-USA cataclysmic event, here is the credit default swap (CDS) pricing on the US government. CDS spreads measure creditworthiness and fear in the marketplace. It’s at the lowest levels it’s been all year, indicating no loss of confidence in the Fed.

To read the rest of this article, and to see our portfolios and get more market timing content, head over to MktContext.com and subscribe today!