Oil Is Well

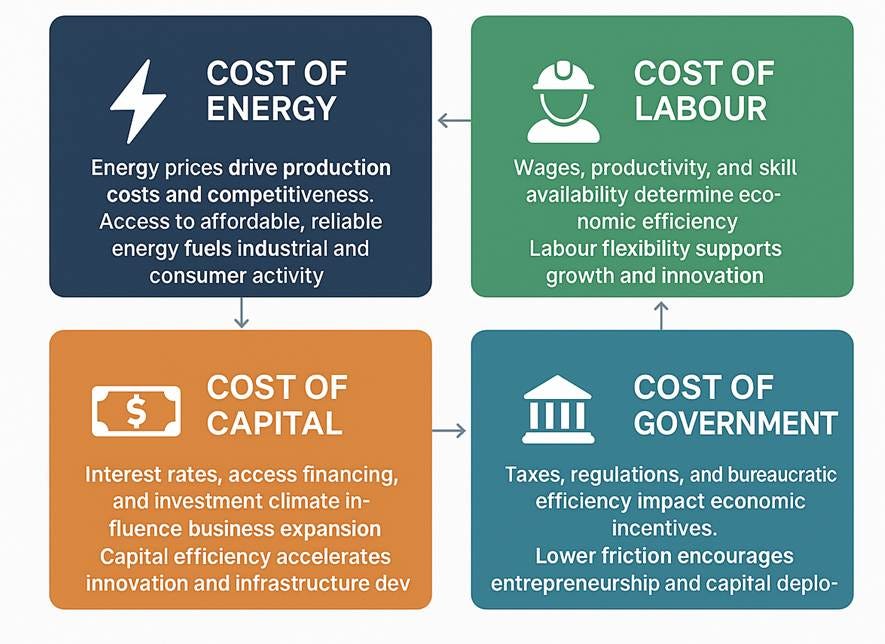

Anyone who’s spent more time studying economics than doom-scrolling on TikTok knows that every economy stands on four pillars: energy, labour, capital, and government. Energy is the fuel of all activity — affordable, reliable power keeps industries alive and consumers spending. Labour determines efficiency and innovation; pay people too much for too little and growth stalls, but balance wages and productivity, and the economy hums. Capital sets the rhythm — low rates and access to financing accelerate investment, while tight money puts it in slow motion. And finally, government — the fourth pillar and often the heaviest — taxes, regulations, and bureaucracy can either grease the gears of enterprise or grind them to a halt.

Anyone who’s dug deeper than a YouTube crash course knows that every economy is just energy in disguise. Money, debt, and production are side effects — the real game is transforming energy into stuff we can use. From baking bread to manufacturing Labubus, it’s all about how efficiently we convert raw energy into value. Human labour, capital, and technology are just middlemen in this grand conversion scheme. When energy is cheap and abundant, economies boom; when it’s scarce or pricey, productivity tanks and living standards follow. History, in short, is one long race to find better energy sources.

And let’s be honest: official economic data is about as trustworthy as a weather forecast from a fortune cookie. If you really want to read the economy, forget the “CP-Lie” and watch market data instead. Stocks versus oil tell you if productive energy is winning — when equities outrun oil, growth’s alive; when oil takes the lead, brace for slowdown. For currency sanity, check gold versus bonds: the gold-to-bond ratio shows if your money’s holding value or being quietly toasted by inflation. Over the long haul, plot equities against oil and gold against bonds with their 7-year averages — above the line means prosperity and efficiency; below it means energy waste and monetary decay. Simple, elegant, and far more honest than whatever the stats office cooked up last quarter.

https://ai.studio/apps/drive/1k2vVhi7jE_NJ3QhNv_ZzovVHfPipazEA

Investors hypnotized by the AI growth fairytale often forget to ask a simple question: what’s powering all those data centers and machines? It’s not fairy dust, it’s oil. Despite decades of green promises and shiny new tech, crude still rules the energy kingdom. It fuels over 90% of global transport, drives industry, and hides in everything from fertilizers to smartphones. Renewables may be growing, but they’re still playing catch-up to oil’s scale, density, and global reach. The harsh truth is that our modern economy still runs on hydrocarbons — every ship, plane, and factory needs them. Oil isn’t just an energy source; it’s the bloodstream of globalization, and its price still sets the pulse for growth, inflation, and geopolitics.

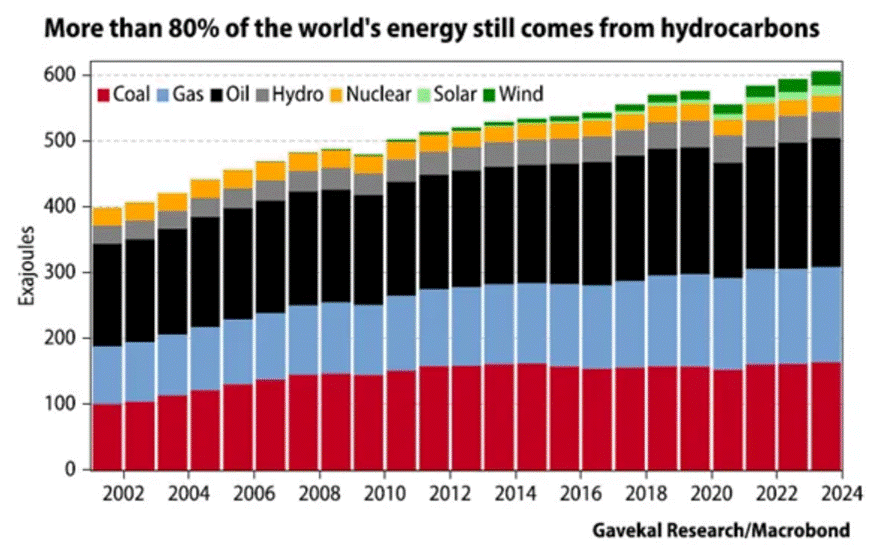

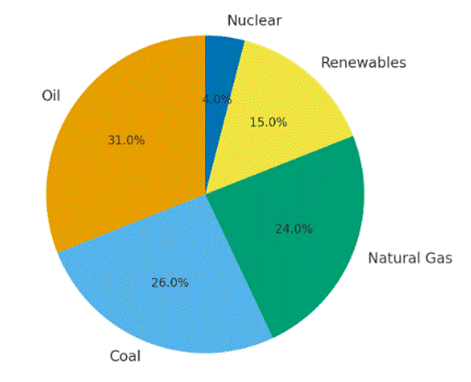

The global energy mix is still anything but “green.” Fossil fuels dominate the scene, supplying about 81% of the world’s energy. Oil takes the crown at roughly 31%, keeping transport, industry, and trade alive. Coal holds a smoky second place with around 26%, mostly for power and steel, while natural gas chips in about 24%, sold as the “cleaner” bridge fuel. Renewables—solar, wind, hydro, and bioenergy—have climbed to around 15%, but they’re still the understudies, not the stars. Nuclear quietly contributes about 4%, humming away as a reliable low-carbon base. In short, despite the renewable hype, the global economy still runs on hydrocarbons — proof that the so-called energy “transition” is more of a long, cautious shuffle than a revolution.

Global Primary Energy Mix 2024

At the end of the day, oil prices obey the oldest law in economics: supply and demand. When demand runs hotter than supply, prices climb as buyers fight over scarce barrels; when there’s too much oil sloshing around, prices sink as sellers scramble to move inventory. It’s the purest expression of market logic — scarcity creates value.

In energy markets, geopolitics, production cuts, or roaring economies can squeeze supply or stoke demand, pushing prices up. On the flip side, new technology, efficiency gains, or sluggish growth can pull them down. In short, supply and demand are the invisible hands keeping oil prices dancing to the rhythm of real-world events.

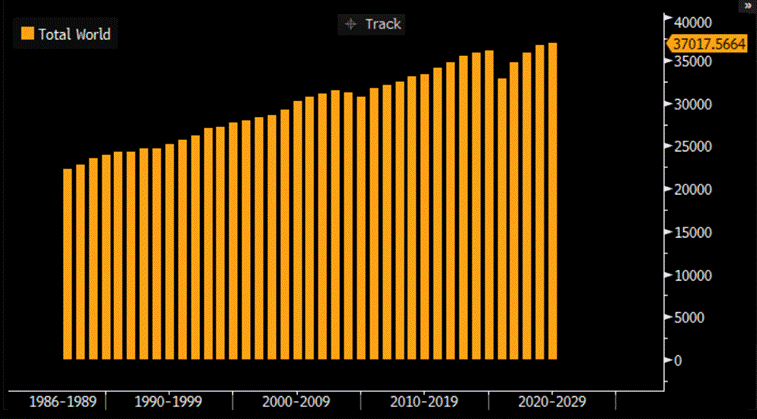

On the demand side, oil consumption has been climbing — yes, we’ve even surpassed the pre-Covid ‘plandemic’ highs — but let’s not get too excited. Growth has been as energetic as a sloth on a Sunday. Between political polarization, economic fatigue, and endless “green transitions” regulations, global demand has managed to rise, but only just. It’s the kind of progress that makes you wonder whether the world’s running on oil… or on wishful thinking.

Total World Oil Demand.

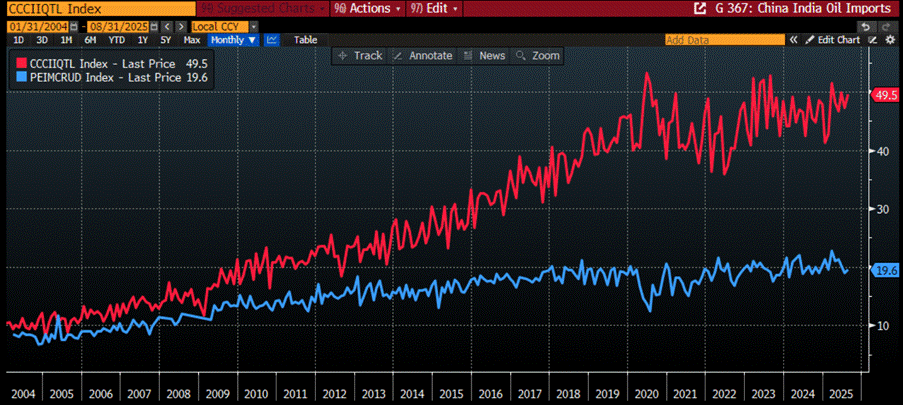

As with most commodities, investors naturally look to China and India to fuel the world’s oil demand story. On paper, it all looked perfect: Chinese consumers buying cars like there’s no tomorrow, China exporting vehicles to every emerging market with a port, and India’s booming population hungry for growth. The setup screamed bullish for energy. Yet somehow, the grand oil demand surge never showed up. China’s oil imports are still hovering around early 2020 levels, and India’s barely above where they were in 2018. Of course, that’s according to official data — the same kind that politely ignores the “dark fleet” of tankers moving sanctioned oil under the radar. After all, when nations like Russia, Iran, and Venezuela are locked out of the dollar system, and buyers like China and India don’t exactly worship Washington’s rulebook, it’s fair to assume a lot more crude is flowing than the spreadsheets admit.

India Oil Imports (blue line); China Oil Imports (red line) (in metric tons).

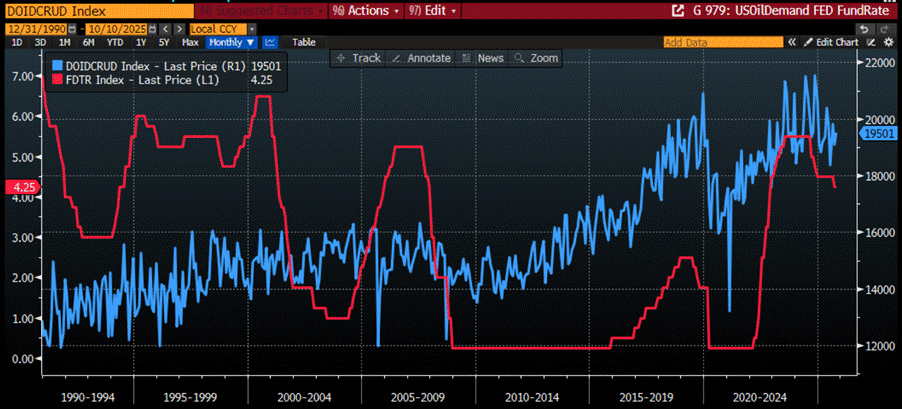

In the U.S., while the folks in the White House keep patting themselves on the back for a “strong economy,” the numbers tell a less glamorous story. Monthly implied oil demand has been sliding since last November, quietly drifting back to the same levels seen before the plandemic lockdowns of early 2020. In other words, beneath the confetti of government press releases and Wall Street cheerleading, oil demand is flatlining. Those who can see through the smoke and mirrors already know what this means — weaker oil demand is moving hand in hand with falling Fed Funds rates, a classic sign of economic fatigue, not strength.

DOE Crude Oil Output Implied Demand Data (blue line); FED Fund Rate (red line).

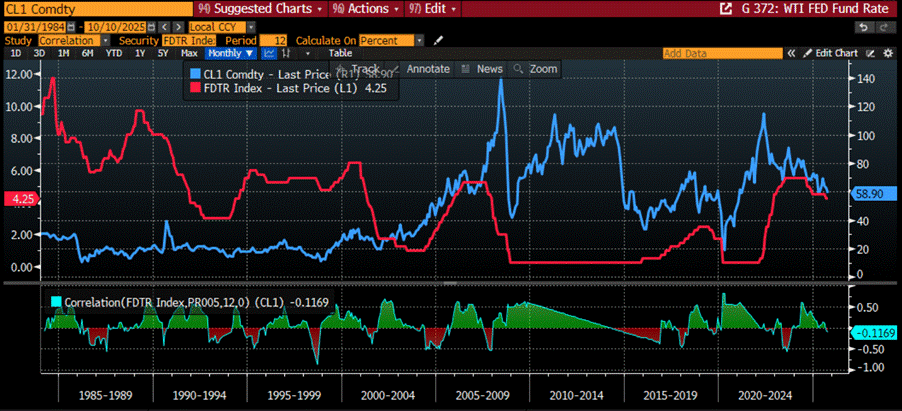

Anyone who’s actually studied the business cycle — and isn’t sipping the Wall Street propaganda cocktail — knows there’s been a tight 40-year dance between WTI oil prices and the Fed Funds rate. Historically, they move together: when rates drop, oil tends to follow. If the Fed is forced to slash rates even further over the next year, it won’t be a sign of economic genius — it’ll be a flashing neon warning that the U.S. is sliding into what could be dubbed Trump Stagflation. In that scenario, investors should brace for more than just lower oil prices; the price of pretty much everything could be headed south.

WTI Price (blue line); FED Fund Rate (red line); & Correlations.

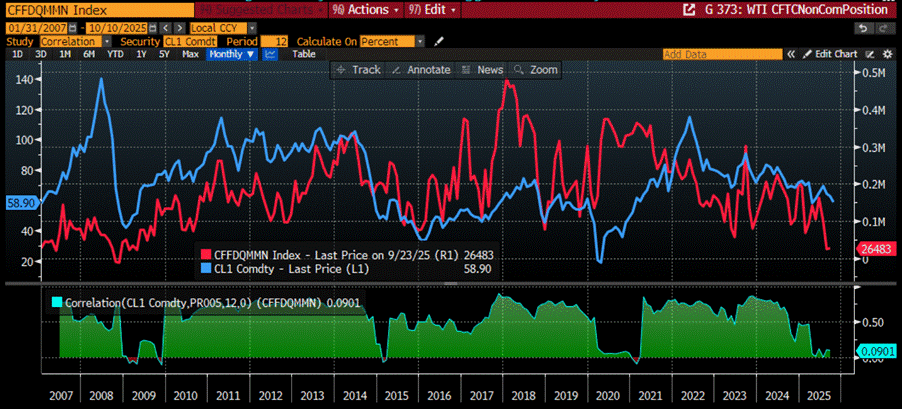

While falling rates and a slowing U.S. economy might look like a drag on oil prices, the market tells a different story. Speculators betting on major rate cuts over the next year have slashed their net long positions in non-commercial oil futures to levels not seen since Q1 2020, right at the start of the Covid panic. Any investor with a shred of common sense would see that — barring a full-blown lockdown or some election-year martial law stunt — hedge funds’ gloom over oil demand is overdone.

WTI Price (blue line); CFTC NYMEX Non-Commercial Net Positions (red line); & Correlation.

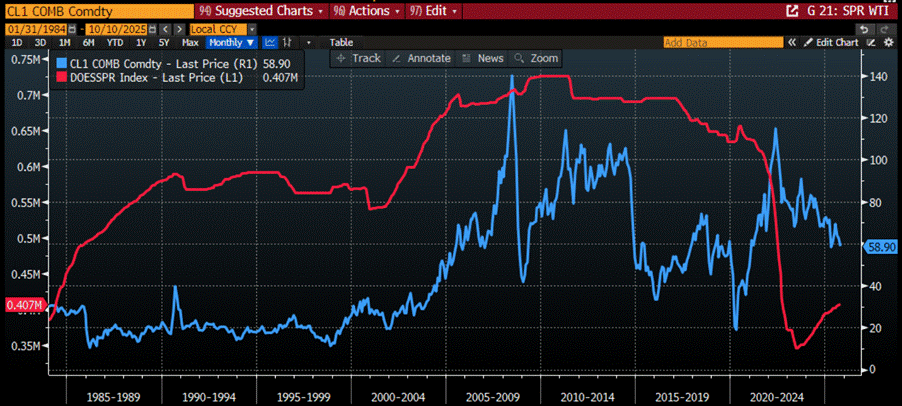

It’s no great secret — and hardly a conspiracy theory — that the Strategic Petroleum Reserve, meant for actual emergencies, has been treated like a political toy to tweak oil prices and pamper the plutocrats to try to impact last year US Presidential Circus. Since Donald Copperfield waltzed back into the Oval Office, the SPR has been rebuilt with all the enthusiasm of a diet salad, while he and his merry band of Malthusian, eugenist warmongers keep doing their best to “teach Russia a lesson” for daring to snicker at ‘Trumperialism’. Cheap oil not only cramps Moscow’s war chest but also nudges Middle Eastern producers like Saudi Arabia and Abu Dhabi for not doing the U.S.’s dirty work in its zionist agenda. And, naturally, the SPR still flirts with a 40-year low — apparently, “strategic” is now just a polite suggestion.

WTI Price (blue line); US Strategic Petroleum Reserve (red line).

Meanwhile, commercial oil inventories outside the SPR are running on fumes. Cheap prices and a tempting futures curve have convinced energy companies to hoard… well, nothing. By 15-year standards, Cushing, Oklahoma’s stocks remain alarmingly low — yet, somehow, every time inventories drop, oil prices still stumble. Logic clearly took the day off.

Read more and discover how to trade it here: https://themacrobutler.substack.com/p/oil-is-well

Join The Macro Butler on Telegram here : https://t.me/TheMacroButlerSubstack

You can contact The Macro Butler at info@themacrobutler.com

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence.