The Banana Republic Portfolio: The Art of Outlasting the EYIs.

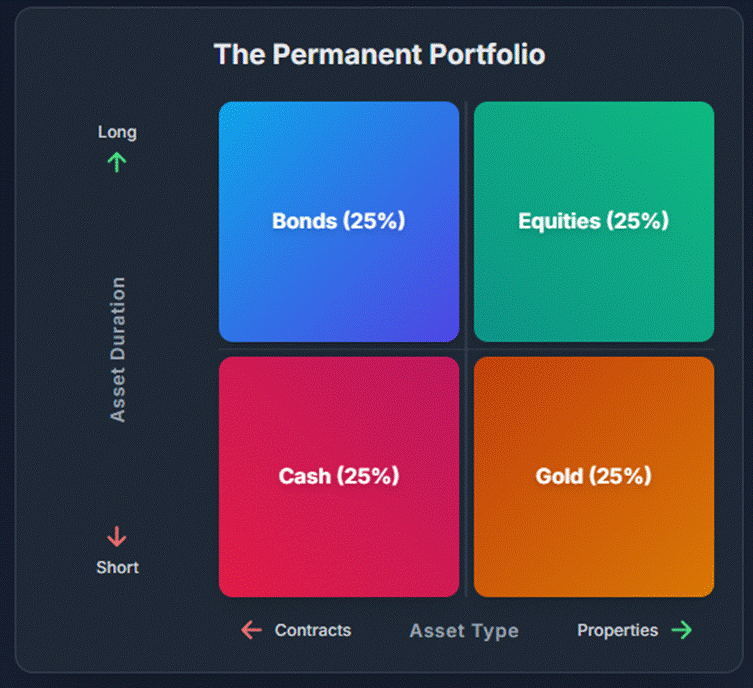

Anyone who is now mastering a modicum of financial literacy should have learnt that Harry Browne’s good old-fashioned Permanent Portfolio is the only way to deliver consistent inflation beating returns. Four simple ingredients, equally weighted: Cash, Bonds, Equities, and Gold. That’s it. No hedge fund wizardry, no crypto moonshots—just a balanced cocktail for sane investors in an insane world.

Within the Permanent Portfolio, financial assets fall into two main camps: contracts—legally binding promises of future payments, like bonds and cash —and properties, which represent ownership claims, through stocks and gold. Some of these assets have long maturities, such as government bonds and equities, while others are short-term, like cash and gold. In essence, this “forever portfolio” can be visualized as four quadrants formed by two axes: properties versus contracts, and long versus short duration—a simple yet elegant framework for balancing risk, reward, and resilience across time.

Every investor confined to domestic assets faces the same four flavors of the so-called Permanent Portfolio: Cash, Bonds, Stocks, and Gold — all in their local currency. Now, if you’ve actually done your homework, you already know that stocks and gold don’t care about your currency; they have intrinsic value, which is finance-speak for “real worth that doesn’t vanish when your central bank gets creative.”

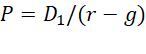

Intrinsic value, in theory, is just the present value of all the future cash an asset will generate, discounted for risk — or in plain English, what it’s really worth once you strip away market noise and central bank fairy dust. For dividend-paying stocks, the Dividend Discount Model (DDM) works just fine: . For everyone else, the grown-up version is the Discounted Cash Flow (DCF) model, which tallies up future free cash flows plus a terminal value — basically, the “and they lived happily ever after” of finance.

Gold is the oddball in the asset family—no coupons, no dividends, no earnings calls, and certainly no “guidance.” You can’t run a DCF on it because there are no future cash flows to discount. Yet, it stubbornly holds value while entire currencies come and go. Why? Because gold’s worth isn’t financial—it’s elemental.

Economists like to dress this up in fancy terms: scarcity and indestructibility (you can’t print or destroy it), universal acceptability (everyone from ancient Egyptians to modern central bankers wants it), and monetary independence (it’s nobody’s IOU, so it can’t default). Add in some industrial and jewelry demand—roughly half the market—and you get a hard floor under its price.

In short, gold’s “intrinsic value” comes from what it is, not what it earns. It’s the asset you hold when you stop trusting everyone else’s promises—and history shows that moment comes around more often than most investors care to admit.

Gold Price in USD terms adjusted to CP-Lie rebased at 100 as December 31st, 1920.

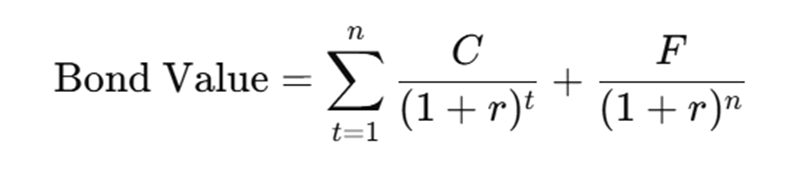

On the other hand, cash and government bonds are basically promises on paper—and not particularly good ones if the currency behind them starts melting. Bonds at least try to justify their existence with math: their value equals the present value of future coupons plus the repayment of face value, all discounted by the required yield. In short:

where is C the coupon, F the face value, r the discount rate, and n the number of periods.

It looks impressive on paper—until inflation or fiscal insanity make those “guaranteed” cash flows worth less than yesterday’s latte.

If a government is hell-bent on structurally devaluing its currency, then the smart move is simple: own property like gold and stocks—and forget contracts like bonds and cash. This becomes even more crucial when that same government, whether by incompetence or design, spreads chaos and erodes faith in public institutions. When trust collapses, citizens and investors stop believing that bureaucrats can fix the mess they created.

In short, when chaos reigns, it’s no mystery why stocks beat bonds among long-duration assets, and gold trounces cash among short-duration ones. It’s just the market’s polite way of saying: “I trust tangible value more than political promises.”

US Aggregate Chaos Index (blue line); S&P 500 to Bloomberg US Treasury Index (red line).

US Aggregate Chaos Index (blue line); Gold to Bloomberg T-Bills Index (red line).

Investors familiar with emerging markets often favor gold and equities over cash and bonds because chronic currency depreciation and inflation erode the real value of fixed-income assets. In places like Turkey, Argentina, and Venezuela, repeated currency crises, aggressive debt monetization, and capital controls have shattered confidence in local paper assets. Holding cash in lira, pesos, or bolívars often means watching purchasing power vanish, while local bonds—despite attractive nominal yields—rarely keep up with rampant inflation. History shows that when monetary policy is politicized or manipulated, investors instinctively flock to tangible, globally recognized assets that governments cannot arbitrarily debase or default on, prioritizing financial resilience over nominal returns.

Performance of 100 unit of local currency invested in MSCI US (blue line); MSCI Turkey (red line); MSCI Argentina (green line) since December 31st, 2019.

The “Educated Yet Idiots” (EYI)—Nassim Taleb’s polite way of saying, “Congratulations, you have a PhD… and still don’t know what you’re doing.” , are almost everywhere especially among those leading governments in the western world. These are the folks with impressive credentials who confidently tackle complex problems but spectacularly miss the point: real-world uncertainty doesn’t follow your neat models.

In finance, medicine, or policy, EYIs can churn out fancy analyses and charts, yet blissfully ignore rare disasters—Black Swans—or systemic risks. Overconfident and armed with technical know-how, they wield influence while being blissfully untested by reality. Taleb’s antidote? Skin in the Game. True competence comes from bearing consequences, not collecting degrees. EYIs are the cautionary tale of modern expertise: sophistication and credentials look great on a résumé, but judgment and practical risk awareness actually keep you from wrecking everything.

https://wisdomfromexperts.com/the-intellectual-yet-idiot-by-nassim-taleb/

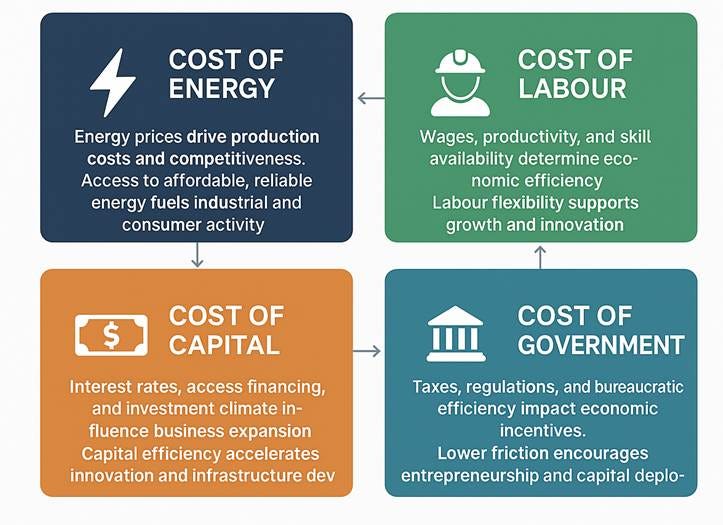

Investors should always keep in mind that economic growth rests on four key pillars: energy, labour, capital, and government.

The cost of energy matters because the economy literally runs on it—cheap, reliable energy powers industry, fuels consumption, and keeps production competitive. Labour costs, productivity, and skill availability shape efficiency, while flexibility and talent drive innovation. Capital costs, influenced by interest rates and access to financing, determine how quickly businesses can expand and invest in infrastructure. Finally, the cost of government—taxes, regulations, and bureaucratic friction—affects incentives, with lower friction encouraging entrepreneurship and capital deployment.

You don’t need an economics PhD to see the obvious: endless government spending and ever-higher taxes are basically a how-to guide for killing growth. Money wasted on bloated bureaucracies, transfer payments, or vanity projects crowds out private investment, stifles innovation, and slows job creation. Higher taxes sap the will to work or take risks, deficits push up rates and inflation, and eventually—surprise!—investors flee and the tax base collapses under its own weight. Fiscal mismanagement: predictable, yet endlessly entertaining.

Enter the Laffer Curve, economics’ version of “there’s a sweet spot for everything.” Too little tax = no revenue; too much tax = no incentive to earn = also no revenue. Somewhere in the middle lies the magical rate that maximizes government take without scaring off work, investment, or innovation. Policymakers love it as an excuse for tax cuts, but finding that exact sweet spot is about as easy as herding cats—it depends on the country, the era, and, frankly, how messy politics is that year.

https://laffercenter.org/about/curve/

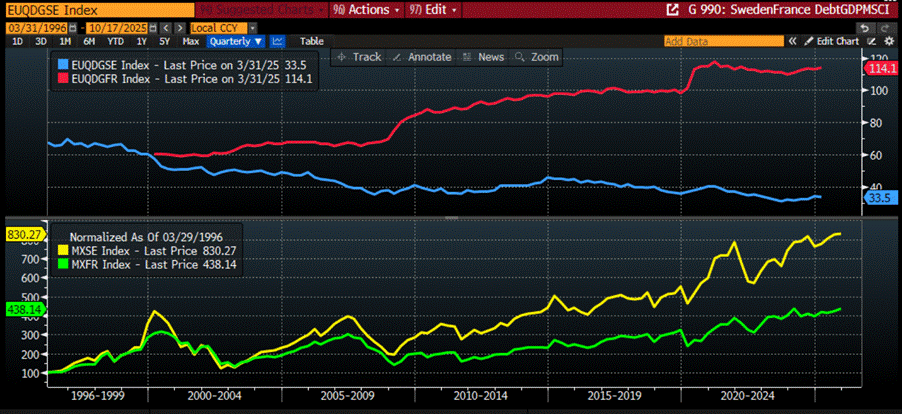

Want a quick lesson on how government spending can strangle—or free—economic dynamism? Let’s compare France and Sweden over the past 30 years. Sweden in 1992 looked bankrupt: government spending at 65% of GDP, three of the four major banks nationalized, and real bond yields above 7%. The Social Democrats did the unthinkable—they slashed state expenditures. Meanwhile, France kept spending like it was going out of style. Since then, government spending relative to GDP rose 9.5% in France and fell 22.4% in Sweden. According to the Keynesian “Educated Yet Idiots,” Sweden should have been in economic collapse—people starving, industries shuttered, markets vomiting under the weight of collapsing domestic demand. Reality check: no deindustrialization, no chronic deficits, huge current account surpluses, and financial markets that thrive. Sweden now borrows cheaply in its own currency and has a debt-to-GDP ratio of just 33%, compared with France’s bloated 114%.

Moral of the story: cut wasteful spending, let the private sector innovate, and stop believing that deficits automatically equal boom. Sometimes, less really is more.

Upper Panel: Sweden Debt to GDP ratio (blue line); France Debt to GDP ratio (red line); Lower Panel: Performance of $100 invested in MSCI Sweden Index (yellow line); MSCI France Index (green line) since December 31st 1996.

As the Western world—including the U.S.—gets run by ‘Educated Yet Idiots’ politicians who couldn’t balance a budget if their lives depended on it, and with media cluelessly speculating about stock and gold rallies, the smart money has already figured out the game. Enter the “Banana Republic Portfolio”: 50% stocks, 50% gold. Adapted from the Permanent Portfolio for a world drowning in chaos, it’s not just about preserving wealth after inflation—it’s about growing it while the political circus rages on. In a rising-chaos environment, this banana-smoothie mix consistently outperforms the so-called Permanent Brown Portfolio.

Simple rule: when governments mismanage and chaos spreads, stick to what actually works—tangible assets and productive equity—and let the bureaucrats flail.

US Chaos index (blue line); Relative of the US Banana Republic Portfolio (50% Gold; 50% S&P 500) to the US Permanent Portfolio (red line).

Read more and discover how to trade it here: https://themacrobutler.substack.com/p/the-banana-republic-portfolio-the

Join The Macro Butler on Telegram here : https://t.me/TheMacroButlerSubstack

You can contact The Macro Butler at info@themacrobutler.com

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence.