Silversqueeze: How We Got Here, Where We’re Going

Short-Squeeze: How We Got Here, Where We’re Going

Summary:

Silver is entering the early phase of a structural short squeeze driven by physical scarcity rather than speculative excess. For decades, bullion banks arbitraged between long physical holdings in London and short futures on COMEX, profiting from carry trades supported by ample inventory.

That system is now breaking down as London’s free float approaches depletion. Accelerating U.S. industrial demand, tariff pull-forward buying, growing ETF inflows, potential sovereign accumulation, and sustained physical withdrawals by China and India are draining available supply. With silver unable to be leased like gold and upstream production increasingly pre-sold to China, banks are rolling futures positions to defer delivery, expanding balance-sheet risk. Current stress reflects financial postponement, not yet full physical capitulation.

I. Core Observation

What we are witnessing in silver is still not close to over.

The available evidence indicates that large short holders who are called on to deliver metal are doing so when they can. When they cannot, they are deferring delivery by rolling their positions forward. This process extends obligations into future months in the hope that new supply will materialize and ultimately resolve the shortfall.

If this interpretation is correct, then the banking system is attempting to financialize a physical supply problem. The outcome falls along two possible paths:

- Failure to financialize the shortage, resulting in a direct and immediate physical short squeeze.

- Temporary success in financializing the shortage, by continually rolling delivery forward. This process risks creating a funding or financial squeeze that eventually culminates in a physical squeeze anyway.

In both paths, physical scarcity eventually asserts itself. The difference lies in timing and mechanism.

II. The Core Banking Trade

For roughly three decades, bullion banks monetized silver by maintaining:

- Long physical metal positions in London, and

- Short futures positions on the COMEX.

This structure allowed banks to collect the carry: the contango spread incorporating storage costs, interest rates, and financing premiums. The trade functioned reliably for years because London served as the flexible pool of readily accessible silver that could be moved to satisfy U.S. delivery needs.

This trade is no longer profitable, largely because buyers now want immediate physical metal rather than paper exposure. The proof of this shift is visible in:

- Rising physical delivery volumes at COMEX.

- Declining available silver inventories in London.

London historically functioned as the stockpile capable of flexibly funding delivery requirements as needed. That stockpile has now been depleted to the point that the free float is effectively near zero. Almost every ounce held in London is contractually committed elsewhere.

Much of this pledged metal now sits backing ETF obligations that have continued to grow as investment demand rises. As a result, the warehouse of excess silver once drawn upon to feed the COMEX is effectively empty.

III. Market Structure

COMEX

COMEX houses both buyers and sellers, primarily acting as a delivery conduit rather than a primary supplier:

- Buyers include speculators but more importantly industrial users, such as major manufacturers that periodically take delivery. Their demand patterns have been large but consistent and predictable for years.

- Sellers are predominantly bullion banks acting on behalf of producers, hedging customer output where producers remain active.

For decades, this system functioned smoothly because banks could hedge production with confidence that London inventory would always replenish any liquidity gaps.

IV. The Shift in Physical Demand

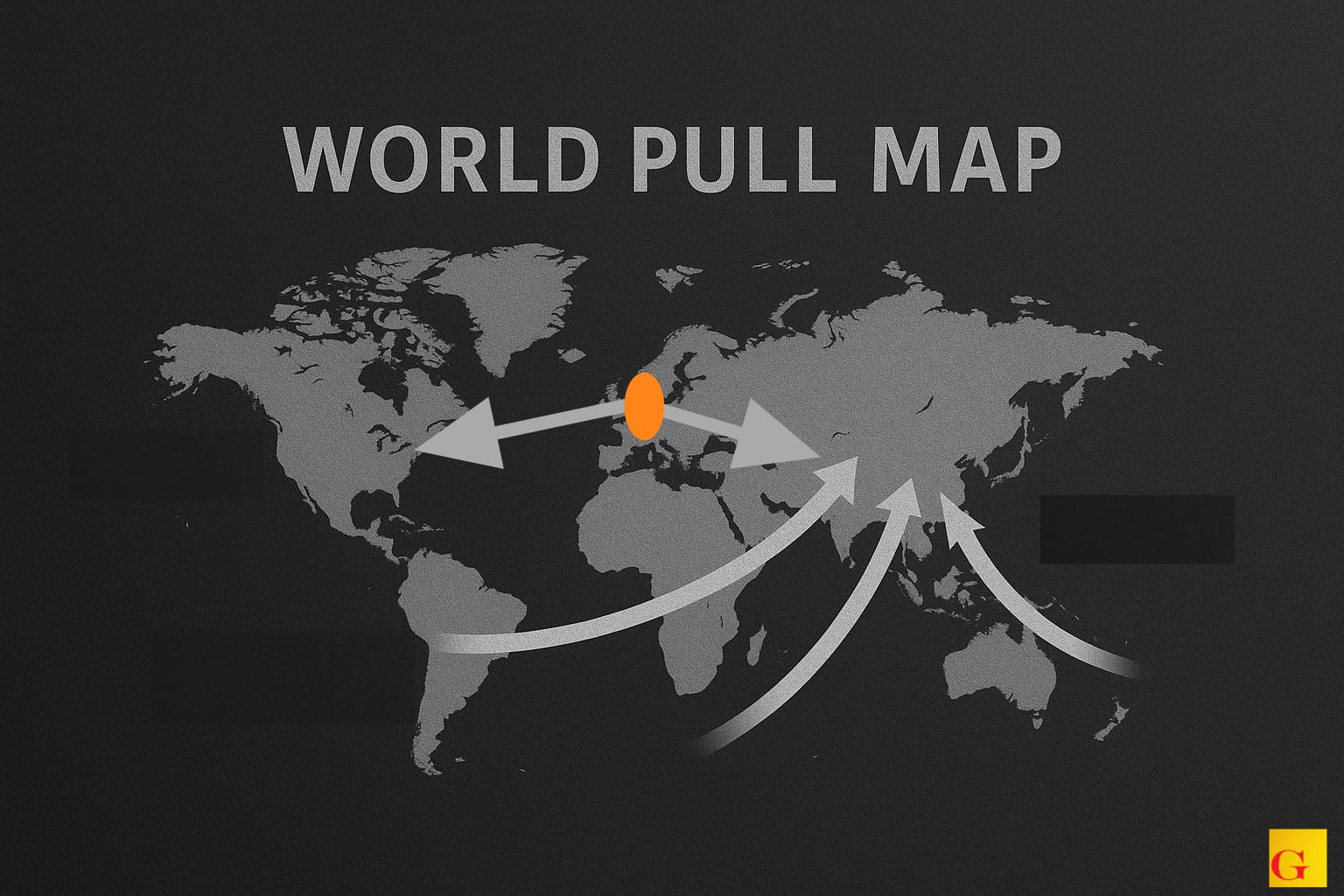

BRICS Demand

A new physical buyer has arrived on the global stage: the BRICS bloc, particularly China and India. These buyers purchase silver directly in the physical market and remove it from London inventories without using futures contracts. Metal purchased is delivered outright.

This created a second drawdown stream on London at the same time as U.S. deliveries were accelerating.

United States Demand

The United States experienced two separate pressures:

- Ongoing industrial demand, now accelerating.

- Tariff-related pull-forward demand, where manufacturers, fearing pending tariffs, advanced years of purchasing into spot markets rather than waiting on future deliveries.

This behavior became most evident during what is referred to as the tariff tantrum following Liberation Day. Industrial firms such as General Electric chose to secure and warehouse supply immediately rather than rely on future contracts vulnerable to tariff uncertainty.

Additional U.S. demand now includes:

- Growing ETF investment interest in silver triggered by increased inflation awareness.

- Reclassification of silver as a critical mineral.

- The probable participation of U.S. sovereign entities accumulating physical supply.

All of these pressures funnel through COMEX deliveries and ultimately draw from London inventories.

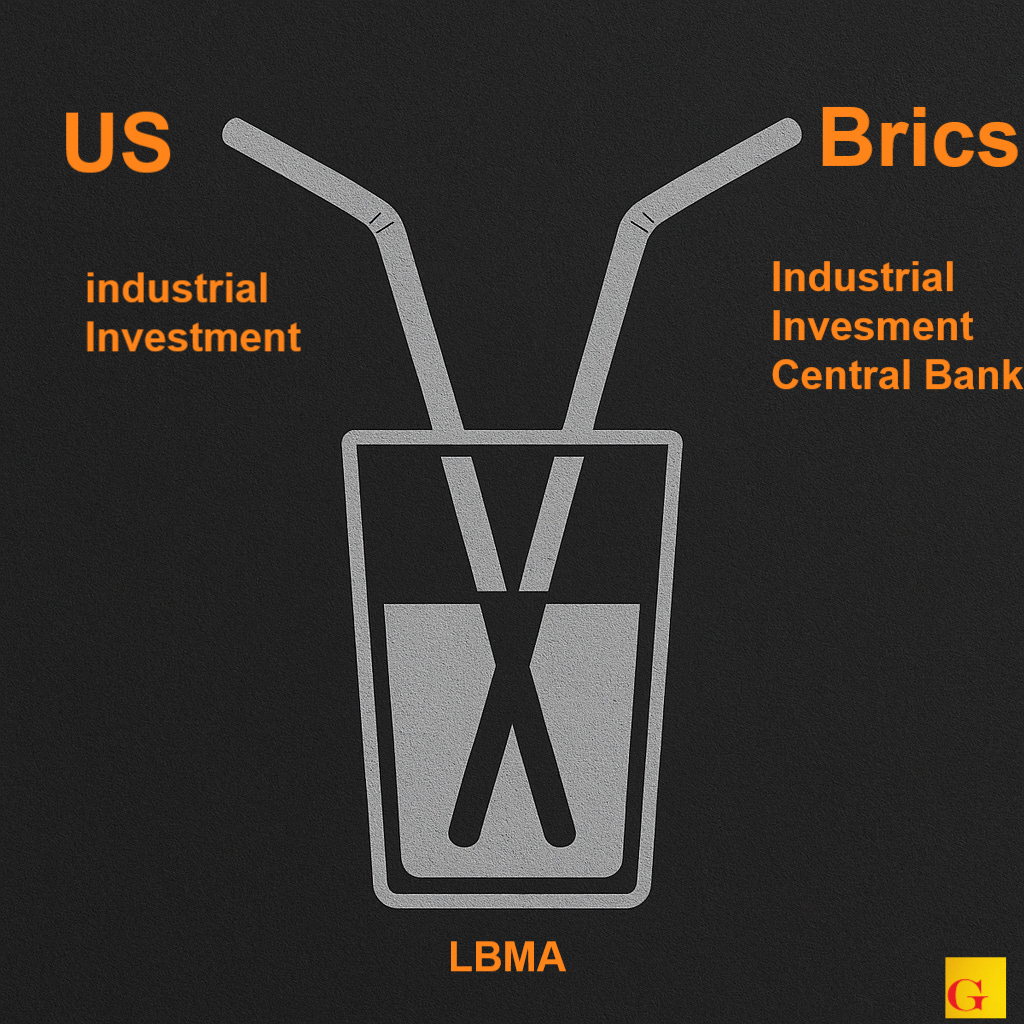

V. London: The Shrinking Middle Pool

At the center of the system sits London with its once ample above-ground supply, now experiencing accelerated depletion.

Both the United States and the BRICS are pulling metal directly from this pool, described metaphorically as two straws extracting the same diminishing stockpile.

Replenishment has failed to keep pace with off-take. Significantly, bullion banks no longer possess a meaningful replacement mechanism:

- Silver cannot be leased from central banks in the same manner as gold.

- No strategic bullion reserves exist to bridge shortages.

- Mine output has not increased sufficiently to offset rising demand.

- Much of available new supply has already been pre-sold.

VI. Mine Intercept- Upstream Supply Disrupted

For more than a decade, China has systematically secured silver supply at the pre-refining stage by purchasing:

Silver concentrate, material bought directly from mines before final processing.

Doré bars, unfinished bullion blends of gold and silver prior to separation and refinement.

By purchasing material before it becomes market-ready metal, China effectively intercepted supply flows long before they could reach global exchanges.

As bullion banks now contact traditional mining clients to source replacement metal, they encounter a consistent response:

- Concentrate is pre-sold.

- Doré bars are pre-allocated.

- Future production streams are contractually committed.

This has resulted in a structural break in traditional sourcing networks that historically supplied bullion banks.

Remaining Sections

- VII. The Mechanics of Rolling Shorts

- VIII. Balance Sheet Stress

- IX. Indicators of Squeeze Timing

- X. Potential Resolution Pathways

- XI. Closing Summary

Continues here

Free Posts To Your Mailbox