How ‘Educated-Yet-Idiots’ Converted the Fed into a Political ATM…

What’s behind the numbers?

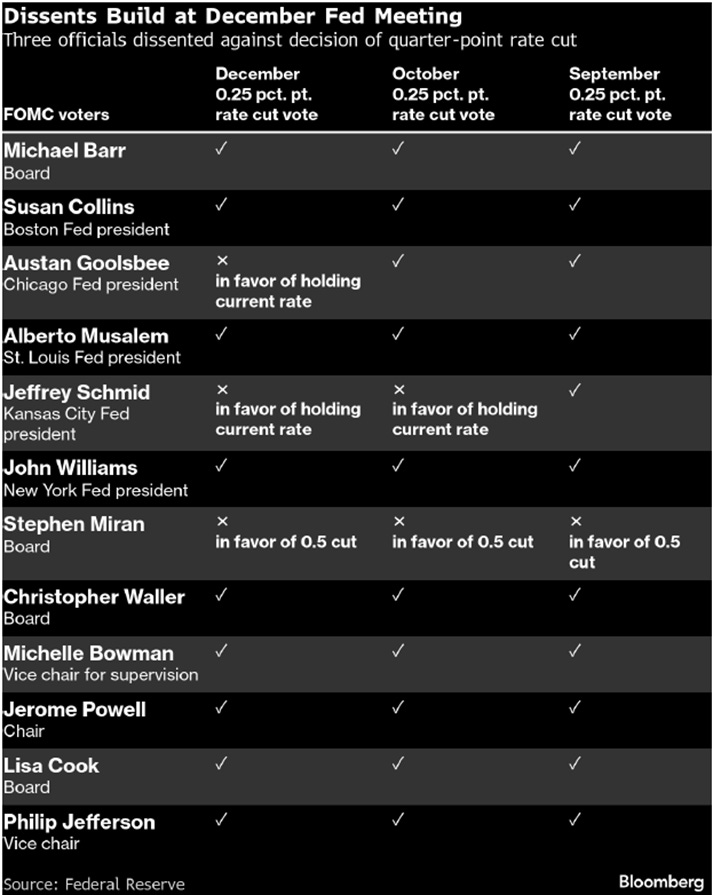

As predictably as a scripted reality show, the Fed delivered its oh-so-expected 25 bps rate cut to 3.50–3.75%, complete with a 9–3 vote that added just enough drama to pretend it wasn’t predetermined. Miran lobbied for a 50-bps slash, while Goolsbee and Schmid played the “steady hands” role, insisting on no change at all.

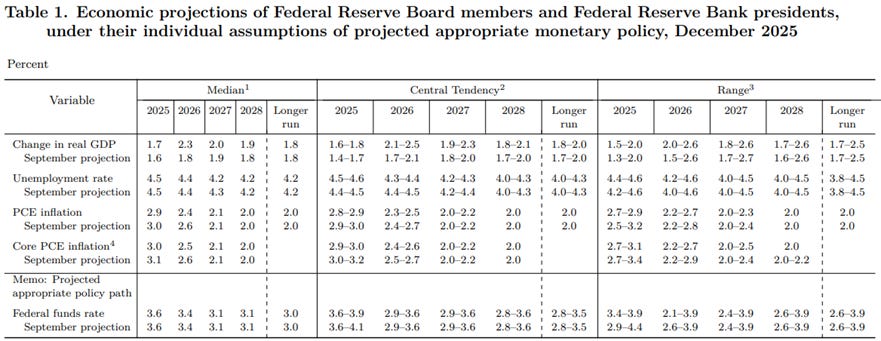

In its latest SEP, the Fed basically photocopied its old rate projections, signalling the same slow march toward the long-run rate. But the 2025 dot plot revealed a fun twist: six members pencilled in 3.75–4.00% for year-end — meaning four non-voters would’ve slammed today’s rate cut if they actually had a vote. The Fed also acknowledged softer job gains and a mild uptick in unemployment, dutifully updating its statement to reflect that things have “edged up through September,” which is Fedspeak for “nothing to see here, please move along.” Inflation remains sticky, though core PCE has cooled just enough for the Fed to pretend it’s feeling optimistic. Growth is still labelled “moderate,” risks are still “uncertain,” and the Fed’s crystal ball now sees slightly stronger GDP in 2026 — proving once again that long-range forecasts are where central bankers allow themselves to dream.

https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20251210.pdf

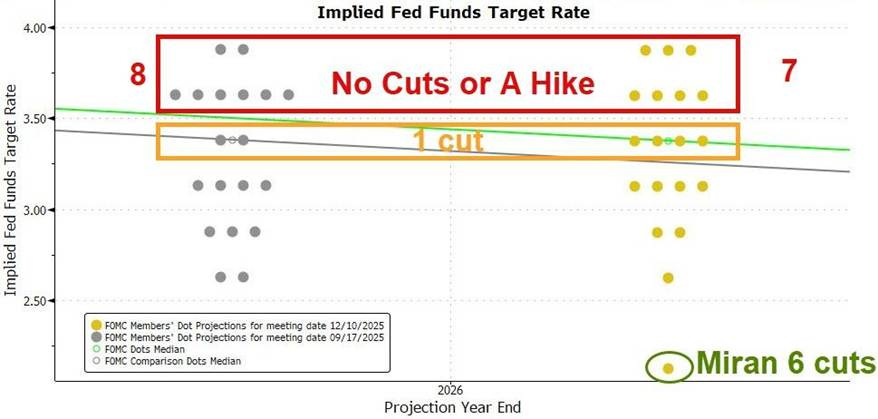

Since the last FOMC meeting on October 29th, the Fed has been operating with almost no fresh macro visibility thanks to the government shutdown. The little data available has been split hard data surprised to the upside, soft data fell apart, and alternative labour indicators were either mixed or hopelessly lagged. Against that backdrop, the updated 2026+ dot plots delivered no new hawkish drama. The median official still expects one quarter-point cut in 2026 and another in 2027 — exactly what they projected in September. If anything, the 2026 dots leaned slightly dovish, with the number of policymakers favouring no cuts or even a hike slipping from eight to seven.

The Fed’s balance sheet update read like a bureaucratic shopping list, but the punchline was simple: the FOMC told the New York Fed to fire up the money vacuum again and start buying about $40 billion in T-bills beginning December 12, just to keep reserves “ample” rather than “abundant” — central-bank speak for “we’re topping up the tank, not flooring it.” These reserve-management purchases will run hot for a few months (conveniently covering the spring spike in liabilities… and the Powell-to-Trump-era transition some are already whispering about) before cooling back down. Everything gets packaged into neat monthly schedules, sector weights, and reinvestments, because nothing says “steady hands” like spreadsheets buying T-bills.

The FED balance Sheet.

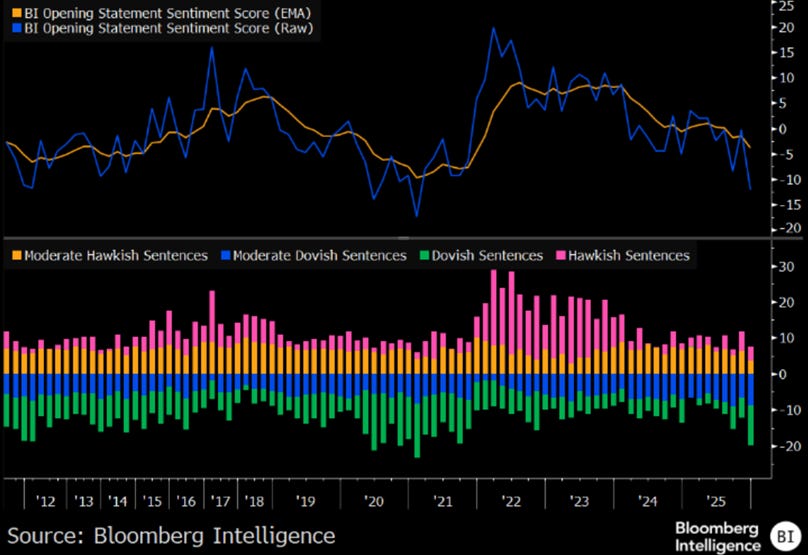

At the press conference, Powell delivered full Fast & Furious: Monetary Drift energy — reserves are fine, the labour market is “kind of stable,” spending is hanging in, inflation is still honking at everyone but it should be a one-time effect, and the Fed is easing off the throttle just enough to avoid blowing the engine before things heat up again. Powell’s opening remarks came in more dovish than last month and the most dovish since 2021 as the comments around the asset purchases were a bigger driver of this move.

Thoughts.

While Wall Street and Donald Copperfield keep performing their favorite magic trick—making investors believe that Fed rate cuts are somehow “good news”—the cold, unenchanted data tell a different story. Every time the Fed waves its wand and declares the cutting season open, it’s less “abracadabra” and more “brace for impact.” The S&P 500-to-oil ratio balloons like an overfed pigeon before plummeting through its 7-year moving average faster than a kamikaze seagull. In truth, every rate cut is the Fed’s polite way of ringing the dinner bell for the next economic bust.

Upper Panel: FED Fund Rate (purple line); Lower Panel: S&P 500 to WTI ratio (green line); 7-Year Moving Average of the S&P 500 to Oil ratio (red line).

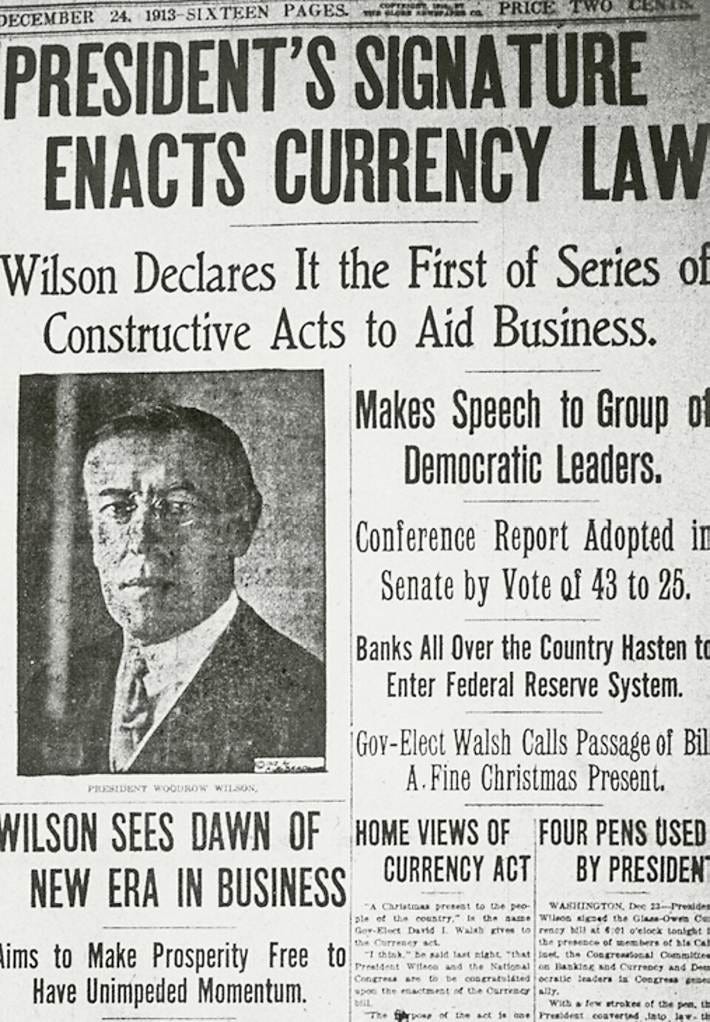

Those with a grounding in history, rather than merely blaming the FED for every stray cloud in the economy, recognize that the institution was birthed from financial chaos and refined by elite manoeuvring. Following the Panic of 1907, Senator Aldrich, demonstrating proper concern for stability (and self-interest), convened a secret gathering of the wise on Jekyll Island. Their mandate was clear: craft a central bank that would both stabilize the markets and, quite prudently, cement the influence of the financial titans over the nation’s purse. Thus, the Federal Reserve Act of 1913 was presented to the public as a majestic safeguard against ruin, while quietly ceding the Mandate of Monetary Heaven to Wall Street—a clever dual design that ensures both its power and its endless controversy to this very day.

The Federal Reserve Act of 1913 established a system of studied compromise. Presented to the populace as a necessary safeguard to end financial panics by supplying an “elastic currency,” its true genius lay in its complex structure: a hybrid central bank with twelve regional branches overseen by a Washington Board.

While the stated purpose was noble—to stabilize the financial order and refine supervision—the quiet legacy was the cementing of Wall Street’s influence over the nation’s monetary destiny. This deliberate design, which fused public necessity with private interest, ensured the system’s power and its unending controversies, making it the critical, yet always contested, pillar of American financial stability to this day.

https://www.federalreserve.gov/aboutthefed/fract.htm

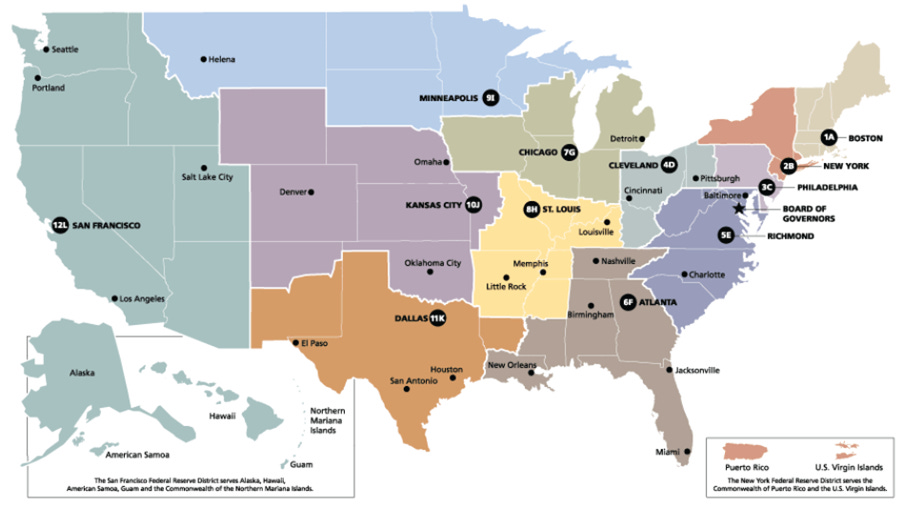

In the crafting of the Federal Reserve System, the architects sought harmony through dispersion, establishing Twelve Regional Federal Reserve Banks. This thoughtful division, based on the population and economic character of the land in 1913, ensures that national monetary policy is not a monolithic decree, but a balanced reflection of the nation’s diverse needs. Each of these twelve districts—from the financial hub of New York to the vast expanse governed by San Francisco—operates as an independent yet interconnected pillar. This structure wisely permits the voices of every distinct region to be heard and considered, preventing policy from favouring one area to the detriment of others, thereby maintaining a crucial equilibrium in the management of the nation’s wealth.

https://www.stlouisfed.org/in-plain-english/the-feds-regional-structure

The Federal Reserve’s nature is a careful exercise in duality, existing by Congressional decree yet structured like a private enterprise for public service. While the Board of Governors acts as the independent government overseer, the twelve Reserve Banks adopt the form of corporations. Member banks hold non-controlling stock and elect two-thirds of each Reserve Bank’s nine-member board of directors. The remaining third, including the Chair, is appointed by the central Board. This arrangement ensures that local business experience and diverse regional interests guide the banks’ actions, blending the necessary wisdom of the marketplace with the authority of the central government to serve the common good.

https://www.federalreserve.gov/monetarypolicy/fomc.htm

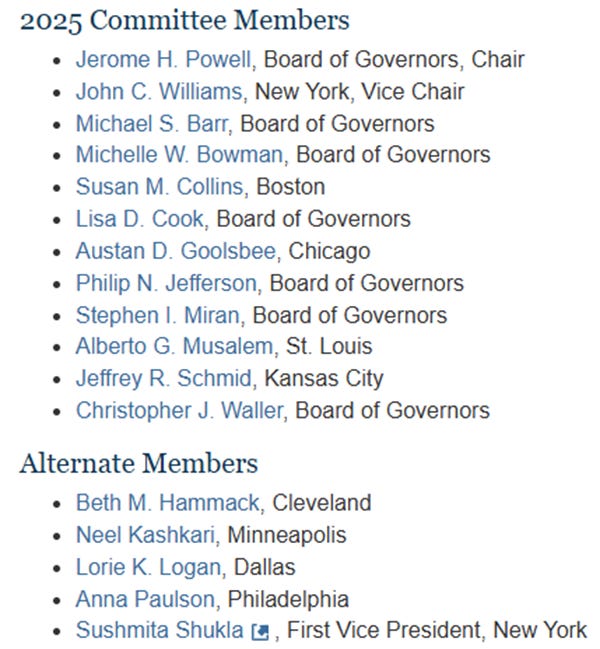

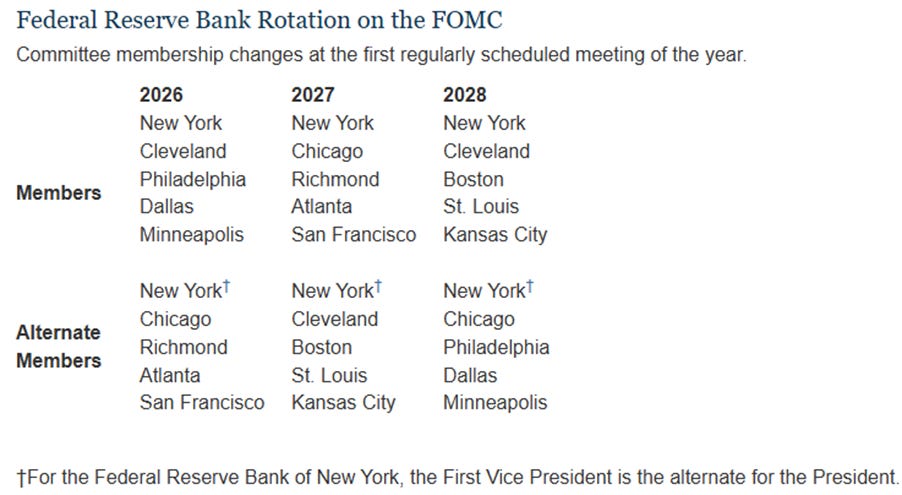

The Federal Open Market Committee (FOMC), the highest assembly for monetary deliberation, is composed of Twelve Voting Members to ensure a harmonious blend of central and regional wisdom. This body includes the seven Governors of the central Board and the President of the New York Fed, who hold permanent votes. To ensure the voice of the entire land is heard, four remaining votes are held by the regional Federal Reserve Bank presidents, who rotate annually through four distinct groups. Though only four may cast a vote in any given year—a mechanism established since 1943 to ensure fair rotation—all regional bank presidents are summoned to the table. They participate fully in discussion and contribute their vital regional wisdom, for in the pursuit of sound policy, all counsel is valued; only the vote is reserved. This annual rotation, which subtly shifts the committee’s prevailing disposition (as seen by the recent move toward a more “hawkish” posture), is a necessary rite to maintain the stability and legitimacy of the national mandate.

People perpetually blame the Fed because pointing the finger at a secretive central bank is infinitely easier than admitting the real problem is the government—our original, never-reformed sin. The tragedy is that the 1913 Fed was a stroke of genius: a decentralized, mechanical system where regional branches beautifully managed local capital flows (the movement of crop money!) and, brilliantly, only dealt in corporate paper, which matures. This allowed for an elastic currency that actually contracted when not needed. It was never meant to be a political ATM.

Then came World War I, and like any promising young man sent to the trenches, the Fed was immediately corrupted. Washington needed to borrow staggering sums, so the Treasury simply commanded the Fed to stop buying real business assets and buy government debt instead. This was the original sin: trading a self-liquidating asset for a debt that never expires.

Roosevelt finished the job, usurping the regional power and concentrating all authority in Washington under a single chairman—a perfect symbol for a centralized, one-size-fits-all political tool.

The bottom line is simple: The central bank doesn’t need reform; the government does. The Fed doesn’t create inflation; our permanently indebted fiscal masters do. Since government debt never contracts, the money supply is doomed to perpetual expansion as they continually borrow to pay interest on interest. So go ahead, continue blaming the poor, corrupted Fed for a system that was perfectly designed to be ruined by the very people we elect.

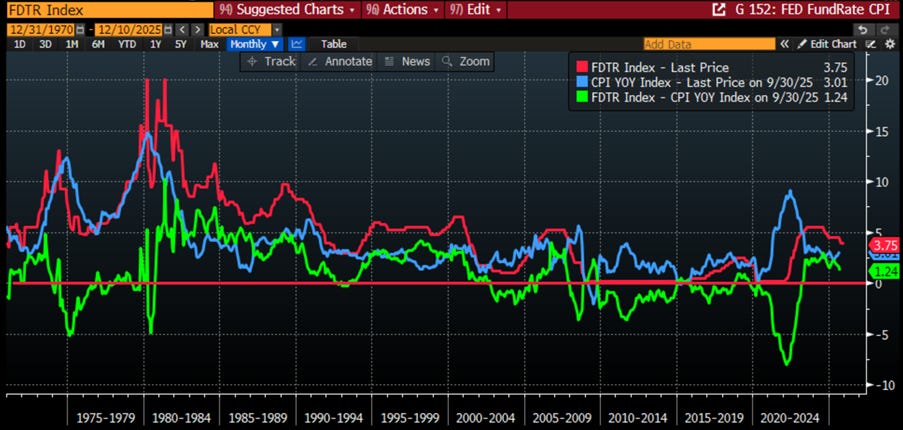

US CPI YoY Change (blue line); FED Fund Rate (red line); Spread between US FED Fund Rate & US CPI YoY Change (green line).

While the apprentice economists of TikTok screech about the Federal Reserve being the source of all American misery, a sober glance at history tells a more inconvenient tale. The so-called Misery Index (Unemployment plus CPI change) clearly demonstrates that the Fed is not the villain; in fact, the opposite is true. Misery only begins its polite decline when the Fed, in its infinite wisdom (or political maneuvering), finally deigns to cut rates. It seems the cure for financial pain is not found in blaming Jerome Powell, but in waiting for him to finally put the punch bowl back out.

US Misery Index (blue line); FED Fund Rate (red line).

The true economists, those who comprehend that inflation springs from shortages, unbridled demand, and decaying public institutions, already know the Fed is a mere scapegoat. The real culprits are the reckless ‘Educated Yet Idiots’ who have steered Western nations toward economic ruin using Keynesian theories that only look appealing on academic paper. The undeniable misery inflicted upon ‘We the People’ actually correlates beautifully with the simple truth: a glance at history confirms a damning link between the spiraling Debt-to-GDP ratio and the dreaded rise of the US Misery Index.

US Misery Index (blue line); US Debt to GDP ratio (red line).

The true Fed villain is not the Fed itself, but the politically gutted shell it became after endless Washington meddling—a far less satisfying truth for the media than blaming the central bank. The American political class, demonstrating the economic grasp of grade-schoolers, perpetually dismantles the system, ensuring the Fed is reduced to a reactive idiot forever chasing the crises created by its own uninitiated masters.

Read more and discover how to trade it here: https://themacrobutler.substack.com/p/how-educated-yet-idiots-converted

Visit The Macro Butler Website here: https://themacrobutler.com/

Join The Macro Butler on Telegram here : https://t.me/TheMacroButlerSubstack

You can contact The Macro Butler at info@themacrobutler.com

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence.