Heading into Q1 earnings, it would be timely to recalibrate the numbers on compute demand.

There are many data points that are indicative of a growth rate in the demand for compute that is much higher than current projections of the volume of compute produced by key AI chip players such as NVIDIA, Google, and Huawei. Key indicators of this dynamic:

Industry indicators suggest that growth in computational demand is outpacing existing market projections. High-level executives at Google, for instance, have signaled a requirement to double compute capacity every six months, a trajectory that would result in a 1,000x increase in capability within the next five years. To put this in perspective, current projections for NVIDIA’s compute sales reflect a CAGR of approximately 210% through 2028; if extrapolated over a five-year horizon, this would represent a 300x increase in accumulated compute—significantly trailing the 1,000x expansion targeted by frontier developers.

Furthermore, research from Epoch AI supports the narrative of rapid expansion in the resources dedicated to training LLMs. Their recent study projects a 2.6x annual increase in compute utilized for LLM training from 2025 through 2030. This consistent scaling underscores a sustained commitment to resource-intensive development as the industry moves toward the next generation of AI capabilities.

“We conclude that the largest individual frontier training runs in 2030 will likely draw 4-16 gigawatts (GW) of power, or enough to power millions of US homes…. Power demands for frontier training runs have historically grown at a rate of 2.2x per year, with the largest runs now exceeding 100 MW. This has primarily been driven by frontier training compute, which has been growing at 4-5x per year…. Training compute scaling will likely continue at around 4-5x/year, despite recent advances in compute efficiency and the shift toward reasoning models. Scaling has historically existed alongside algorithmic efficiency improvements, and the reasoning paradigm will still incentivize further compute scaling in reinforcement learning.”

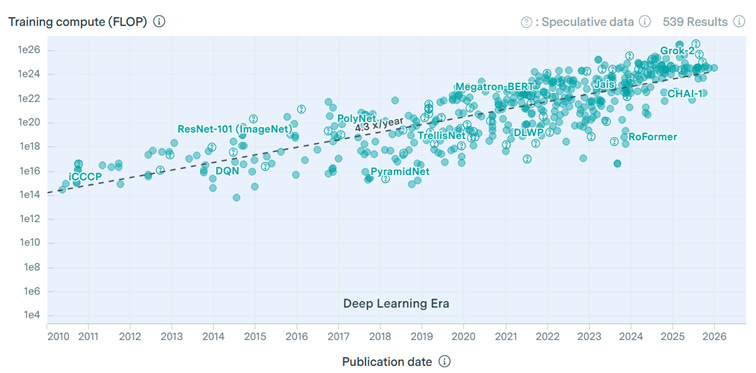

The following EpochAI chart points to a ~4.3x annual increase in computational power used to train LLMs

If we extrapolate these training growth numbers and overlay them with MS NVIDIA projected chip sales, the percentage of chip sales for LLM training alone escalates rapidly.

Extrapolating the EpochAI Projected Growth in Compute Used for LLM Training, and Comparing Against projected NVIDIA Chip Sales, the Result is a High Share of NVIDIA Chip Sales for Training:

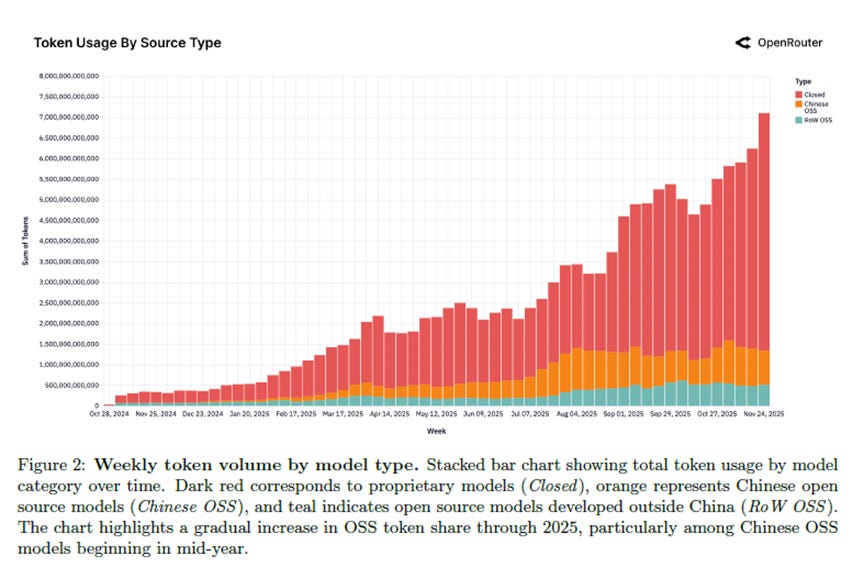

Data from the past year confirms an exceptionally rapid acceleration in token demand, which serves as a critical proxy for overall computational requirements. According to OpenRouter metrics, average weekly token demand surged by more than 2,200% between late November 2024 and late November 2025. This exponential growth underscores the intensifying scale of AI utilization and the corresponding pressure on infrastructure to keep pace with market consumption.

Token Usage By Source Type:

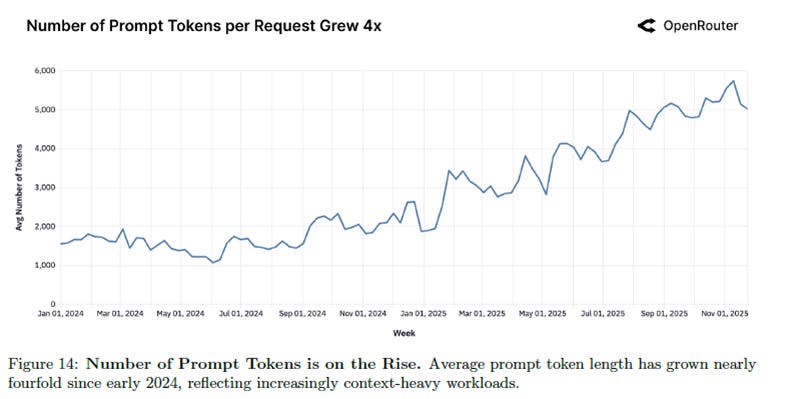

The computational intensity per LLM query is rising sharply, driven by a proliferation of diverse use cases and the increasing complexity of AI interactions. Data from a joint study by Andreessen Horowitz and OpenRouter illustrates this trend, highlighting a rapid surge in the average token intensity per request. As users transition from simple queries to more sophisticated, multi-step workflows, the underlying compute required to fulfill each individual interaction scales accordingly.

Number of Prompt Tokens per Request Grew 4x:

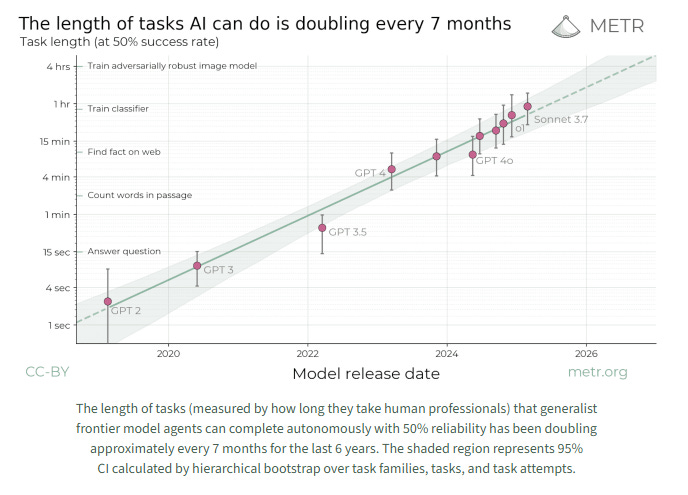

The rising computational intensity per query is further exemplified by the “time horizon” of tasks performed by AI agents. According to research from METR, the average duration of autonomous work a frontier LLM can perform per customer query is currently doubling every seven months.

This metric—the length of a task an agent can complete with 50% reliability—serves as a critical indicator of real-world utility. Even if the total customer base were to remain constant, this seven-month doubling cycle represents a growth in compute demand that significantly outpaces current infrastructure supply projections. Specifically, this trajectory exceeds the approximately 120% CAGR in compute capacity projected to be sold by NVIDIA over the coming years, suggesting a looming gap between model capabilities and available hardware.

The length of tasks AI can do is doubling every 7 months:

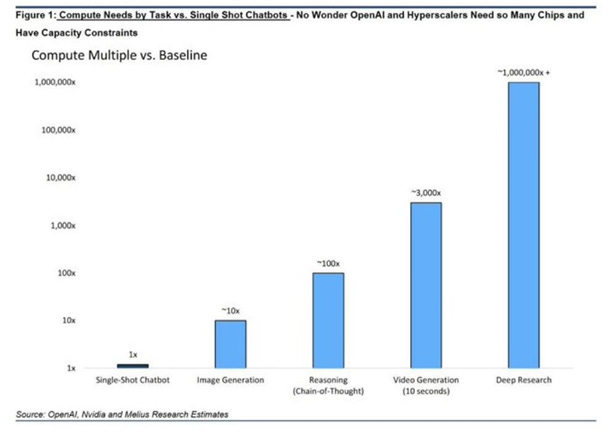

The complexity of emerging AI use cases represents a shift in computational requirements that is orders of magnitude greater than current predominant applications. Recent data shared by Michael Dell highlights this trajectory, demonstrating that several critical, next-generation AI workflows require exponentially higher levels of computational intensity.

Compute Multiple vs. Baseline:

Source: OpenAI, Nvidia and Melius Research Estimates

Recent high-profile transactions underscore the extreme urgency for securing compute and power, revealing a market where access to physical infrastructure is often valued more highly than the underlying hardware.

Asset Resilience: CoreWeave recently re-contracted leases for legacy NVIDIA Hopper GPUs at 95% of their original pricing. This figure significantly deviates from standard economic depreciation models for semiconductors, suggesting that the immediate availability of operational clusters outweighs the typical performance-per-dollar decay of older hardware.

The Power Premium: A strategic “powered shell” agreement involving Google, Anthropic, and FluidStack with Bitcoin miner Hut 8 ($HUT) highlights the critical role of energy access. The deal, which yielded an 18.5% unlevered return on capex for Hut 8, implies a ~300% premium for existing power access—the primary driver for Google and Anthropic’s participation.

Bullish

The investment implications of these moves are decidedly bullish for the merchants of compute, including chip manufacturers, neoclouds, and data center developers. Furthermore, there is significant tailwind for companies providing critical data center components such as memory, optical interconnects, backup power, and cooling systems. Perhaps most notably, this environment favors “de-bottlenecking” providers capable of accelerating power access—specifically those involved in fuel cells, turbines, energy storage, and the repurposing of Bitcoin mining sites or existing power plants for data center use.

Contributor posts published on Zero Hedge do not necessarily represent the views and opinions of Zero Hedge, and are not selected, edited or screened by Zero Hedge editors.