A Silver Bubble?

Data and insights from Brett Friedman, Winhall Risk Analytics/OptionMetrics Contributor, with 30+ years building and managing three risk management organizations.

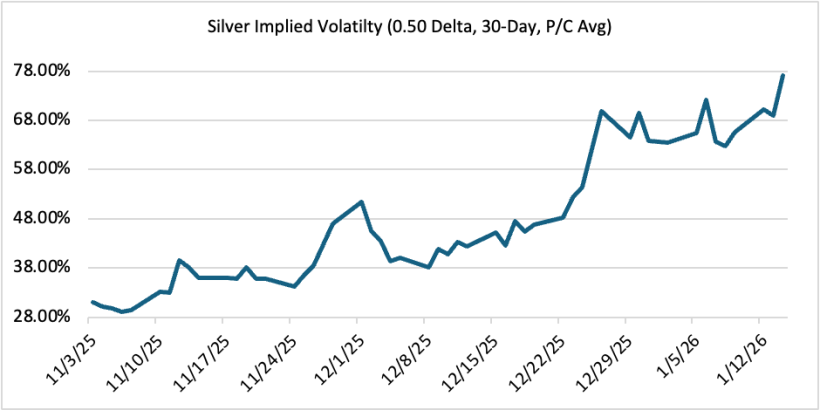

The rally in precious metals continues unabated. And, in particular, silver's implied volatility has exploded since the beginning of November and is currently trading at 77.1%, a full 46 percentage points higher. Are we in a silver bubble? Brett looks at four critical factors, using options data from OptionMetrics and other data sources, that may hold the answer.

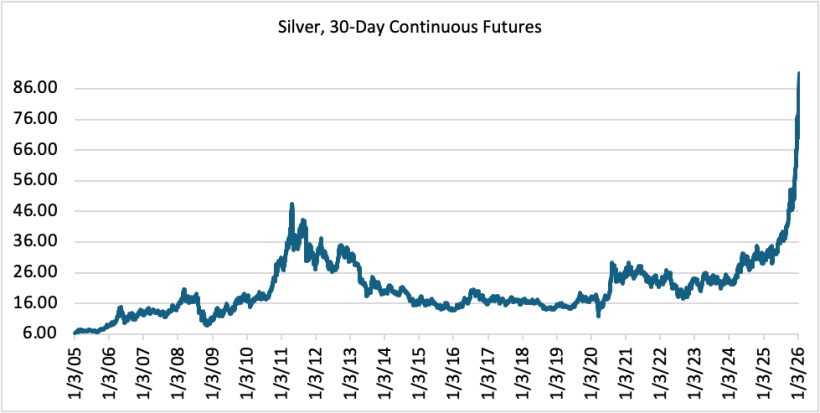

It is very early 2026, and certain trends from 2025 seem to be carrying over into the new year. Most prominently, the inexorable rally in precious metals continues unabated. Gold used to be the standard bearer of the complex, but now all eyes are on silver. At the time of this writing, it's already up a whopping 34.1% year-to-date. This follows its performance in 2025, when it registered the highest return of any commodity, 142.4% (platinum and palladium were second and third, up 127.1% and 77.5%, respectively). To put that into context, silver's 2025 performance was almost eight times that of the S&P.

Source: OptionMetrics

The trend has only accelerated since last Christmas, as has its volatility. Consider this: daily silver returns have been greater than +/- 4% for 10 out of the 13 trading days since December 26th; 6 were greater than +/- 7%. Given that, it's not surprising that silver's implied volatility has exploded since the beginning of November and is currently trading at 77.1%, a full 46 percentage points higher.

Source: OptionMetrics

The obvious question: is silver forming a bubble? A few factors may lead to that conclusion:

1) The Most Recent Fundamentals May Be Temporary.

Two factors are usually cited as driving the metal higher.

First, silver's increasing role in industrial applications and its use in electronics, EVs, and solar panels have all led to a tight supply/demand situation. In fact, the global market for silver has been in a supply deficit for the last seven years. Growing demand for silver-backed ETFs, as well as recent Chinese export restrictions, have made the situation even worse.

Second, the usual broad economic factors supporting gold are also applicable to silver. Inflation (the "debasement trade"), a declining dollar, and belief that the world is turning away from the US dollar, all support precious metals.

However, both of these factors have been true for some time and were present even before the metal almost doubled in price over the last few months. One could therefore question whether they are truly behind the most recent price action. They seem more like the background to the most recent rally, but not necessarily the immediate catalyst.

So, what could be setting off silver's latest meteoric rise? In short, one likely possibility is the unrelenting economic and political instability, uncertainty, and anxiety. Recent events in Venezuela, Iran, and Greenland, as well as questions surrounding the long term independence of the Fed, have all come within days or weeks of each other. This only confirms the perception that the world is increasing unstable and becoming more so every day. This has driven precious metals, and specifically silver, to ever new highs. Bubbles require constant feeding to keep them inflating, and closely spaced news events are tailor-made for this purpose. However, when the news cycle slows down, which it inevitably will, this catalyst will be mitigated and will not propel prices to the extent they are currently.

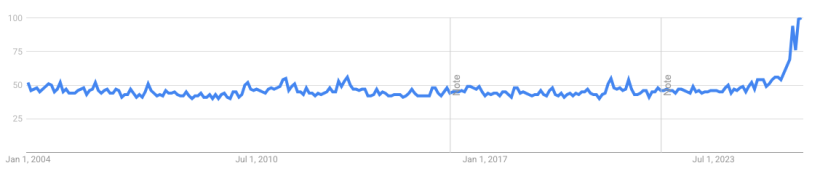

2) Excessive Social Media And Search Presence.

The "information ecosystem" (as one commentator put it) is abuzz with silver. As revealed by Google Trends, search interest for "silver" recently reached an all-time high:

Google Trends, Search Term = "Silver"

Recent price increases have only added to the trend and have driven volume in silver futures, options, and the ProShares Ultra Silver ETF (AGQ) to stratospheric levels. Confirming the increased interest, the CME recently announced that they are introducing a 100 oz. cash settled silver contract, specifically designed to attract retail investors.

All this suggests that investors who don't normally trade precious metals are entering the market. Since they are most likely and primarily opportunistic momentum investors, and their experience with silver is limited, their staying power in the event of downside volatility or margin increases may be limited. In other words, these participants may get in quickly and may get out just as fast.

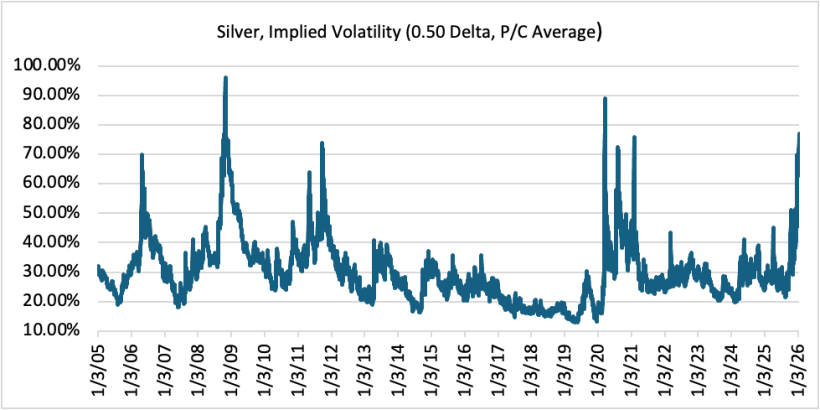

3) Prices Tend To Accelerate And Become More Volatile During The Last Phase Of A Bubble, The "Blow-Out" Period.

Silver's daily returns since 12/26 have been +/- 7% for 6 out of the 13 trading days since. Since 2005, that level of return variation has only occurred 1.2% of the time; greater than a 7% daily return has only happened 20 days, or 0.4%. Silver's implied volatility (see chart below) reflects this and is currently trading at roughly 77%. Levels above 60% have only occurred 2.4% of the time, and on average last just 14 days.

Source: OptionMetrics

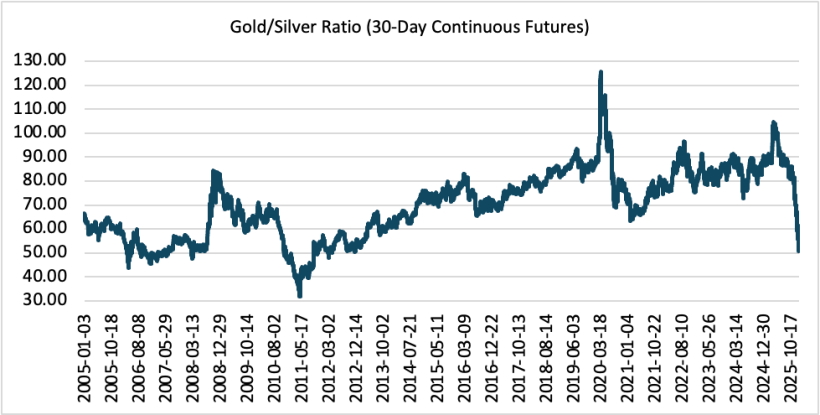

4) The Most Common Metric Used By Precious Metals Traders, The Gold/Silver Ratio, Has Been Plunging.

As you can see in the chart below, the ratio has been plunging since April 2025. As of 12/26/25, the ratio had declined 24.8% over the previous 20 trading days, its largest decline in percentage terms since 2005. It currently stands at 50.9; in comparison, at the beginning of last Q4, it was 83.0.

Source: OptionMetrics

The four factors described above are leading to a conclusion that the current market may be displaying "bubble-like" behavior. Although the fundamentals behind silver seem solid and are certainty supportive, they may be temporary. Supply shortages and locational dislocations will eventually resolve themselves and geopolitical events will become less regular. In addition, the magnitude of the most recent move, along with increased search and social media traffic, suggests that those not usually involved with silver have entered the market. These newcomers may be relatively weak hands, and can exit quickly, sometimes from rapid and significant increases in exchange margin requirements.

Silver has a history of this. Between 1978 and 1980, the Hunt Brothers, two Texas oilmen, attempted to corner silver by buying massive amounts of the physical metal and futures. After driving the price from $3.00 to $50, the exchange stepped in and raised margins to 50% and prohibited any new long positions. Consequently, silver crashed from $50 to $13 in a matter of weeks. The Hunt Brothers went bankrupt and then faced litigation for the rest of their lives. In 2010, the economic recovery following the financial crises increased the industrial demand for silver. Although the fundamentals were more solid this time, the resulting rally eventually reached a fever pitch by April 2011, having increased 57% in just the first four months of the year. The exchange then responded by increasing margins five times in eight days, or 150% in total. Silver never recovered and was back below $35 just 10 trading days later.

Of course, one caveat: not all aggressive bull markets are bubbles and confusing the two can be very expensive. Genuine bubbles are rare, and usually only apparent in retrospect. Consider that last year, AI, private credit, gold, and silver were all held forth as possible bubbles, ripe for imminent and dramatic destruction. Despite some short-term downtrends, this still hasn't happened (at least not yet).