Independent in Name Only

What’s behind the numbers?

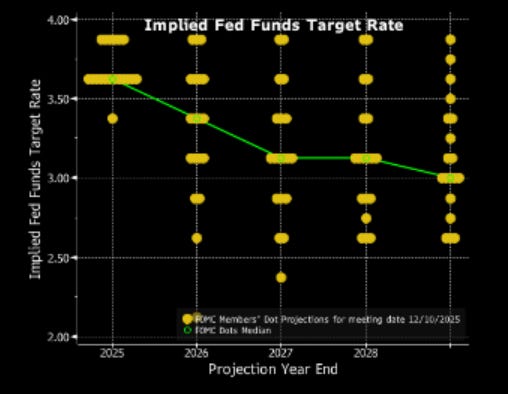

As predictably as a scripted reality show, the Fed voted 10–2 to keep rates parked at 3.5%–3.75%, with Christopher Waller and Stephen Miran playing the rebels by calling for a modest quarter-point cut. Officials insist policy is hovering around the elusive “neutral rate”—the monetary equivalent of room temperature—though no one can quite agree where that thermostat is set. December’s projections offered 11 different guesses from 19 policymakers, neatly confirming that while the Fed can hold rates steady with discipline, it remains impressively flexible when it comes to defining neutral.

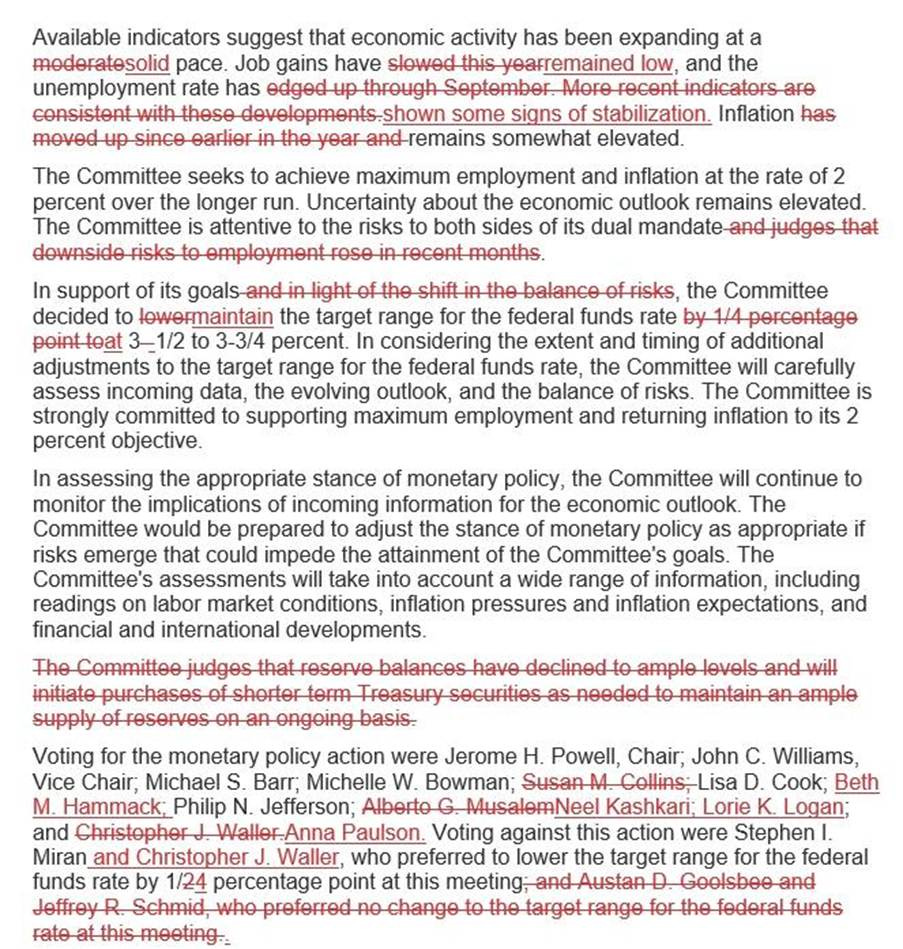

In its press release, the Fed struck a subtly more upbeat tone: growth got an upgrade, with officials noting that economic activity “has been expanding at a solid pace.” Inflation, however, remains the familiar guest who refuses to leave, still described as “somewhat elevated.” On the labour front, the Fed quietly shelved its earlier worries about rising downside risks, instead observing that job gains are low, but the unemployment rate is showing tentative signs of stabilizing—less a victory lap than a cautious nod that the patient is no longer getting worse.

Since the December FOMC meeting—and the widely anticipated signal that more, not less, liquidity would be required to keep politicians happy and the Fed’s ATM conveniently stocked—the Fed’s balance sheet has quietly expanded by more than $40 billion. An impressive sum for anyone living outside Wall Street, but little more than loose change in a balance sheet that still weighs in north of $6.5 trillion.

The FED balance Sheet.

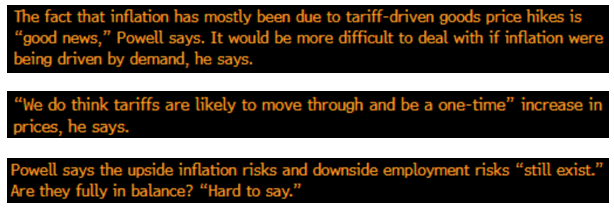

At the press conference, the Central Banker-in-Chief replayed the greatest hits on Fed “independence,” reminded everyone that monetary policy is allergic to election calendars, ignored the dollar like an embarrassing dinner guest, and reassured markets the Fed is “well positioned” to wait—assuming the data isn’t delayed by yet another government shutdown. Translation: the economy is “fine,” easing is paused, patience is policy. On the more awkward notes, Powell swatted away questions about the DOJ investigation and his post-chair future, pointing reporters back to his earlier statement and proving that some topics are even more “data-dependent” than inflation.

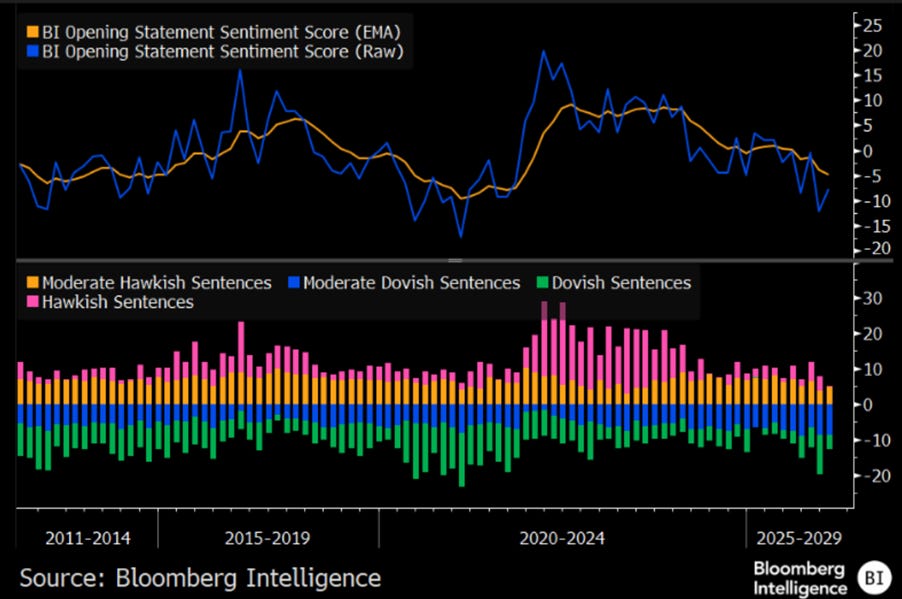

According to the Fed Sentiment model, Jerome’s opening remarks took a small step away from dovishness—but only a small one. Think Beige Book vibes: things are a bit better, still not great, and definitely not worth popping champagne over.

Thoughts.

While Wall Street and Donald Copperfield keep performing their favourite magic trick—making investors believe that Fed rate cuts are somehow “good news”—the cold, unenchanted data tell a different story. Every time the Fed waves its wand and declares the cutting season open, it’s less “abracadabra” and more “brace for impact.” The S&P 500-to-oil ratio balloons like an overfed pigeon before plummeting through its 7-year moving average faster than a kamikaze seagull. In truth, every rate cut is the Fed’s polite way of ringing the dinner bell for the next economic bust.

Upper Panel: FED Fund Rate (purple line); Lower Panel: S&P 500 to WTI ratio (green line); 7-Year Moving Average of the S&P 500 to Oil ratio (red line).

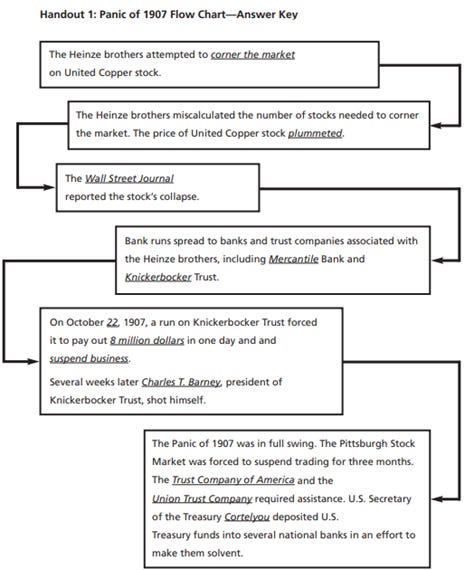

When the Federal Reserve Act was signed in 1913, the idea was simple (and optimistic): create a central bank smart enough to stop financial panics, but aloof enough to ignore politicians in campaign mode and bankers in bonus season. America didn’t lack banks—it lacked adults in the room. After repeated panics and the near collapse of 1907, rescued not by the government but by J.P. Morgan passing the hat, the republic had to admit an awkward truth: the world’s rising power was one margin call away from begging a private banker for help.

The lesson wasn’t to crush markets or hand the keys to Congress, but to build a referee wedged awkwardly between Washington’s printing presses and Wall Street’s greed. Thus was born the “independent” Fed—not holy, not sovereign, but cleverly insulated enough to annoy both sides. The Federal Reserve Act of 1913 was a masterclass in American compromise: sold to the public as a cure for panics via an “elastic currency,” and engineered as a bureaucratic labyrinth—twelve regional banks watched over by a board in Washington. Officially, it was about stability and supervision. Unofficially, it locked Wall Street into the plumbing of monetary power. The result was an institution strong enough to matter, opaque enough to endure, and controversial enough to never quite belong to anyone—except history, which keeps putting it back on trial.

https://www.federalreserve.gov/aboutthefed/fract.htm

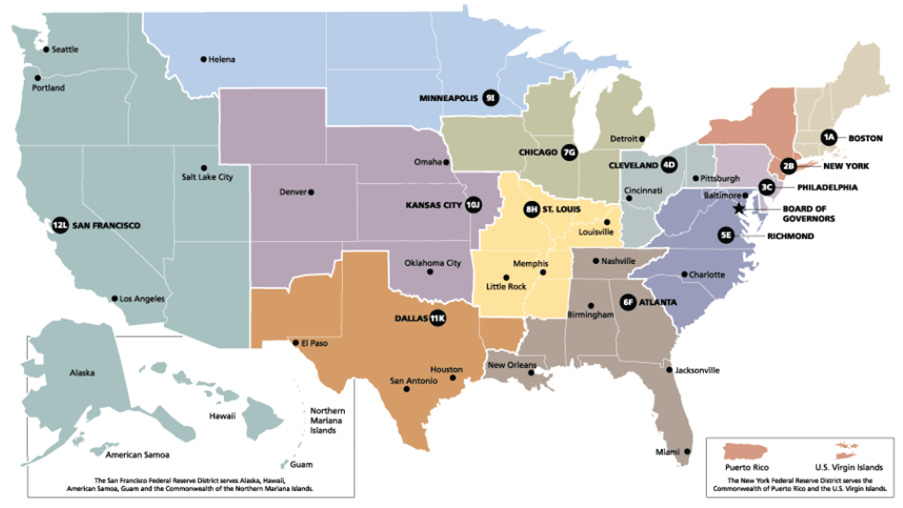

To grasp what the Fed was meant to be, forget Keynes and Friedman and think Bagehot, Aldrich, and a banking system that kept tripping over itself. The Panic of 1907 helpfully exposed the problem: money that wouldn’t stretch in a crisis, thousands of tiny banks with no conductor, and no lender of last resort—unless you counted J.P. Morgan’s living room. Europe had central banks; America preferred chaos to centralization, thanks to a long memory of Jackson smashing the Second Bank. So, the Fed was engineered as a decentralization paradox: twelve regional banks, a board in Washington, a public-private mash-up, and governors with terms long enough to outlive election slogans. Its original job was refreshingly boring—lend in a panic, smooth seasonal hiccups, keep the system upright. No growth targets, no inflation obsession, no macro wizardry. The Fed was a plumber, not an economist—and it definitely wasn’t supposed to pick up Congress’s bar tab.

https://www.stlouisfed.org/in-plain-english/the-feds-regional-structure

The Fed was designed to be independent—but not sovereign, which is a polite way of saying Congress owns the deed and keeps a spare key. Lawmakers created it, can rewrite its mandate, and can remodel the whole building whenever the political mood swings. From birth, the Fed came with three design flaws: a mandate vague enough to invite constant reinterpretation, a cozy proximity to government finances that only works if politicians show restraint (they didn’t), and a crisis playbook where every “temporary” emergency measure mysteriously becomes permanent. Independence, it turns out, wasn’t a constitutional right—it was a conditional privilege, dependent on disciplined government, limited deficits, and respect for boundaries. Those conditions, like the gold standard, did not make it through the 20th century.

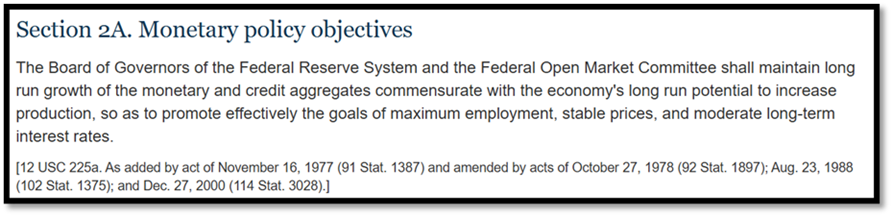

https://www.federalreserve.gov/aboutthefed/section2a.htm

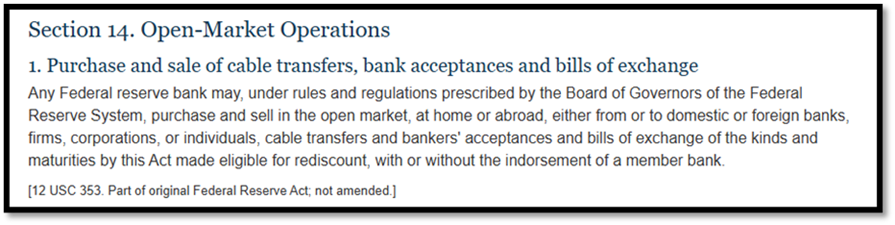

Officially, the Fed has a tidy two-part mission: keep inflation under control and maximize employment—price stability by day, jobs by night. Unofficially, there’s a third mandate that never makes the brochure: whatever it takes to keep the American financial system from blowing up before breakfast. When markets wobble, banks sneeze, or leverage starts screaming, the dual mandate politely steps aside and the real job begins—provide liquidity, print reserves, open facilities, and reassure everyone that “the system is sound.” Inflation and employment matter, of course, but history suggests the Fed’s true north is simpler: no crashes on my watch.

https://www.federalreserve.gov/aboutthefed/section14.htm

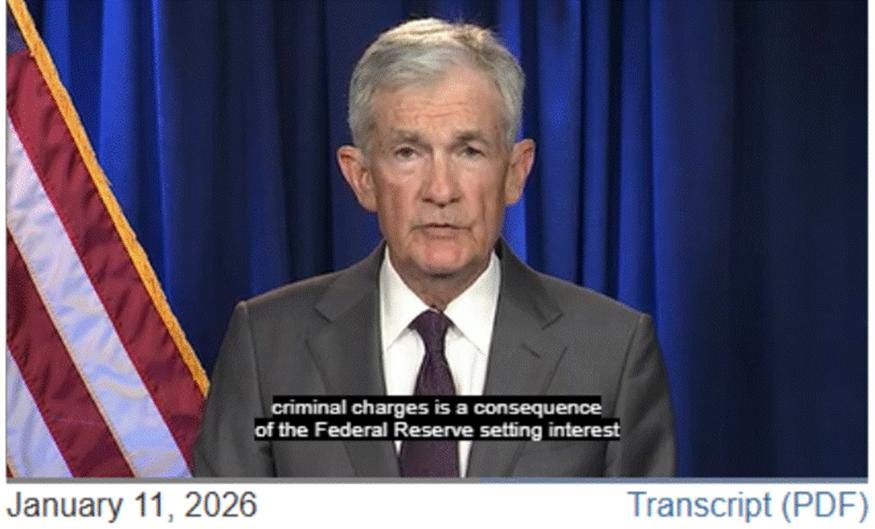

One hundred thirteen years after its birth as an “independent” institution, the Fed finds its Chairman politely subpoenaed to the Department of ‘Just-Us’, proving that all animals are equal—especially interest rates. In the latest episode of Freedom Is Rate Cuts, political power discovers a bold new frontier: if markets won’t obey guidance, perhaps prosecutors will. Weaponizing justice against rivals was last season’s scandal; weaponizing it to bully monetary policy is the reboot. Powell, guilty of the ultimate thoughtcrime, dared to say rate decisions serve the public, not presidential mood swings. In proper Orwellian fashion, independence is now sabotage, pressure is patriotism, and coercion—naturally—is merely “stimulus.”

https://www.federalreserve.gov/newsevents/speech/powell20260111a.htm

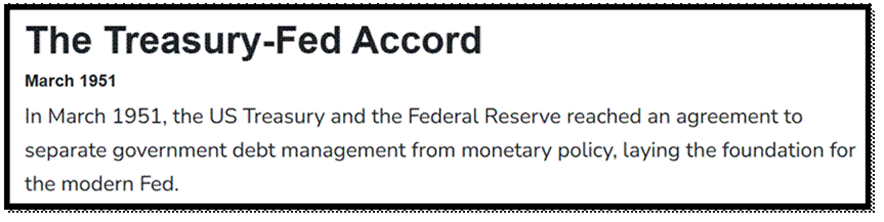

The weaponization of monetary policy is hardly new—just 75 years after Truman tried to arm-twist the Fed into capping rates to pay for the Korean War, the same script is back with updated costumes. It failed then, and history suggests it won’t end well now. If Donald Copperfield truly believes he can replace the Central Banker-in-Chief with a compliant chimpanzee trained to smash the rate-cut button on command, the United Socialist America may soon discover that monetary magic always fades—usually right around the morning of the post-midterm hangover.

https://www.federalreservehistory.org/essays/treasury-fed-accord

The real question is whether the Fed was ever truly independent—or merely tolerated until it became inconvenient. In responding to the latest criminal referral, J.P., the Central Banker-in-Chief insisted that the threat of prosecution is simply the price of committing monetary thoughtcrime: setting rates based on data rather than presidential desire. In other words, evidence is insubordination, independence is defiance, and intimidation is now policy coordination. This drama taps into a century-old ambiguity. On paper, the Fed sits neatly under the executive branch; in practice, everyone politely agreed to pretend it didn’t. Courts have nodded vaguely at its independence, never quite pinning it down in constitutional stone. J.P. assumes this latest episode is just another attempt to bully rates lower—but that may be optimistic. The subpoena traces back to a far less abstract offense: allegedly lying to Congress about a $600 million renovation complete with VIP dining, marble, water features, and a roof garden—features that somehow materialized despite repeated denials.

This is where Orwell meets Versailles. Independence may excuse unpopular rate decisions; it does not authorize imperial refurbishments funded by creative accounting and inflation alibis. J.P. maintains he acted “without fear or favour,” focused solely on price stability and employment. Fair enough—but in the Ministry of Central Banking, it turns out that credibility, like marble terraces, is expensive and surprisingly hard to hide.

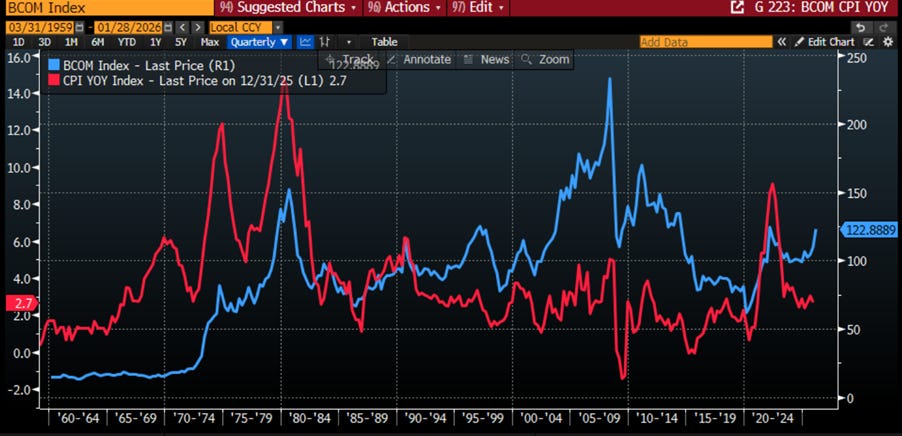

Here lies the awkward timing problem. The USA just lived through the second-worst inflationary episode in a century of modern monetary policy. Between 2021 and 2024, the dollar quietly lost roughly 25–30% of its purchasing power across a broad basket of goods and services—and in many everyday categories, prices didn’t creep higher, they outright doubled. This is, to put it mildly, not the ideal backdrop for invoking the Fed’s unwavering “commitment to price stability.”

Bloomberg Commodity Index (blue line); US CPI YoY Change (red line).

Read more and discover how to trade it here: https://themacrobutler.substack.com/p/independent-in-name-only

Visit The Macro Butler Website here: https://themacrobutler.com/

Join The Macro Butler on Telegram here : https://t.me/TheMacroButlerSubstack

You can contact The Macro Butler at info@themacrobutler.com

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence