Goldman: Central Banks Raise Floor While ETFs Raise Roof

Contents

- CBs Bide Time While Americans Fomo-Buy

- Gold Dealers Got Gamma-Squeezed Higher

- Base Case $5400: Americans Stop Buying and CBs Step Up

- Upside Risk: Americans Keep Buying and Someone Panics

- Tactical Downside Risk from a GLD Puke

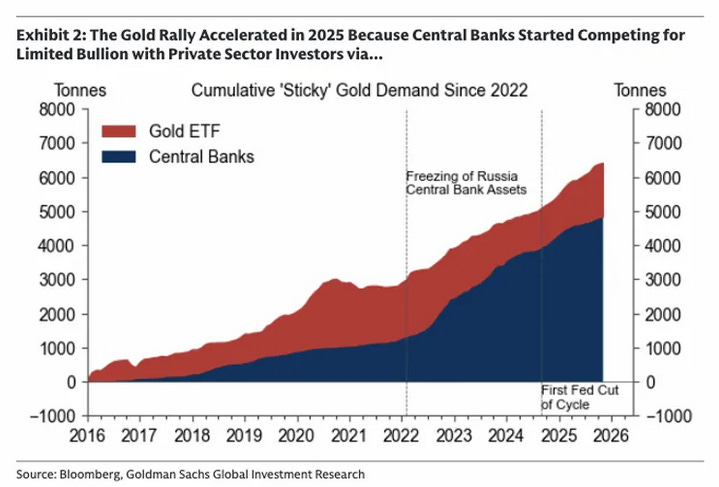

CBs Bide Time While Americans Buy

Authored by GoldFix

In January of this year, Goldman Sachs raised its 2026 gold forecast to $5,400, citing sustained private-sector diversification into bullion as a structural demand driver rather than a temporary hedge. The bank argued that persistent macro policy risk, combined with continued central bank buying and renewed ETF inflows following Fed easing, has created a higher base for prices. Reversals, it notes, would likely require falling demand tied to reduced fiscal or monetary uncertainty, not increased supply.

This week they are back to double down on their call despite the very recent pullback in recent Central Bank activity— calling it temporary and laying the blame for it at the feet of call-buying and vol-triggered FOMO types. We wonder outloud if they are talking about Tether outbidding the more patient bankers recently.

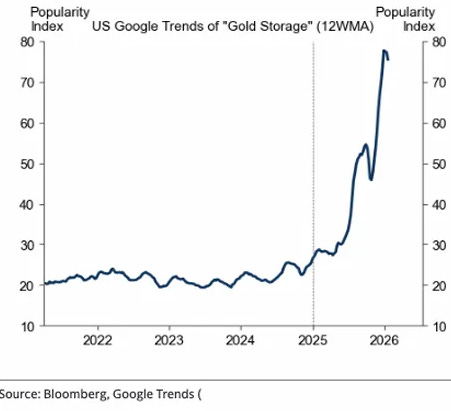

Recent developments in private sector portfolio diversification (Ray Dalio et al telling people to buy gold) behavior have begun to influence gold price dynamics through derivatives positioning.

Demand for gold exposure via call-option structures has introduced additional volatility into spot price formation, with observable implications for both investor activity and official sector accumulation patterns.

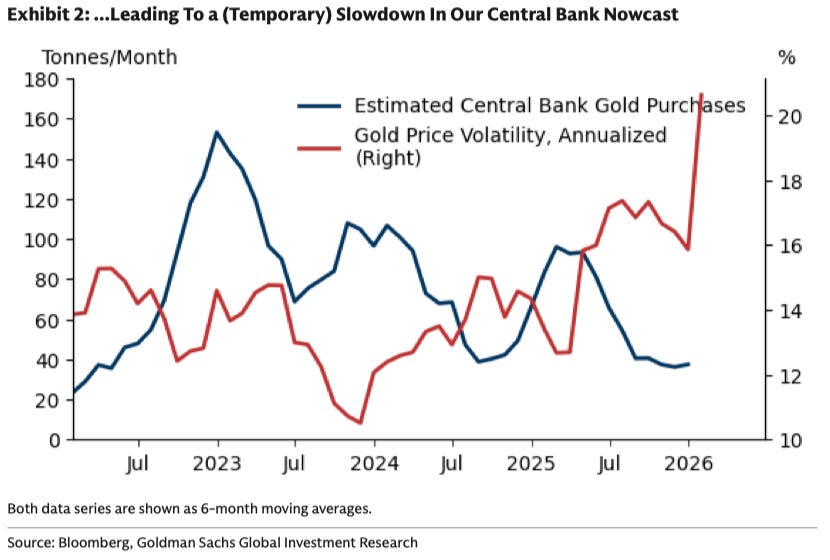

Thursday Goldman Sachs analysts Lina Thomas and Daan Struyven identified an interaction between rising private sector options activity and a deceleration in central bank gold purchases. The analysts characterize this slowdown in official demand as temporary, citing structural changes in reserve management practices following the freezing of Russian foreign exchange reserves in 2022 and noting that emerging market central bank allocations to gold remain below perceived long-term targets.

“Reserve managers remain willing buyers of gold to hedge geopolitical and financial risks but prefer to delay purchases until prices stabilize.”

Goldman identifies increased physical purchases by high-net-worth families and rising investor demand for call options as meaningful incremental sources of demand.

Gold Dealers Got Gamma-Squeezed Higher

According to the report, elevated price volatility can be mechanically linked to dealer hedging behavior in response to investor demand for call options. As gold prices rise, dealers who have sold upside exposure must increase hedges through spot or futures purchases. These flows may amplify upward momentum during rallies. Conversely, moderate price declines may prompt hedging adjustments that reinforce downside movement, potentially contributing to investor stop-outs and localized drawdowns, as observed in late January.

Goldman: Dealing Banks Gamma-Squeezed in January

As dealers hedge short call exposure, they purchase underlying gold, reinforcing upward momentum. This dynamic persisted until late January, when policy communication from Fed Governor Kevin Warsh eased fiscal concerns, prompting a reversal. Dealer hedging then shifted from buying strength to selling weakness, contributing to cascading stop-loss activity.

“As prices move higher, dealers who have sold these calls are forced to buy gold to maintain hedges, mechanically amplifying upside moves.”

The bank reports that recent volatility has corresponded with a decline in its central bank demand nowcast, which stood at 22 tonnes in December 2025. The 12-month rolling average is now estimated at 52 tonnes. While sustained weakness in official purchases has previously been identified as a key risk factor for medium-term gold price performance, the analysts view current conditions as transitional rather than indicative of a structural shift.

Base Case: Americans Stop Buying and CBs Will Step Up

The report outlines two potential forward-looking scenarios. In the base case, no additional private sector diversification into gold occurs beyond recent levels. This outcome would likely coincide with moderation in price volatility, allowing central bank purchases to re-accelerate in line with the pace observed during 2025. Private investor participation in this scenario would remain conditional on prospective Federal Reserve policy easing.

“Under that base case, we expect central bank buying to re-accelerate, with accumulation continuing broadly at the pace seen in 2025.”

Under these assumptions, the bank forecasts a gradual increase in gold prices toward $5,400 per troy ounce by the end of 2026

Upside Risk: Americans Keep Buying and Someone Panics

In an alternative upside scenario, further private sector diversification driven by fiscal concerns across several Western economies could increase volatility through sustained options-based exposure.

Continues here