The $600 Billion Prescription Drug Cartel Just Got Disrupt

The prescription drug market in America isn't broken—it's rigged. For decades, a handful of pharmacy benefit managers (PBMs) have operated as a legalized cartel, extracting billions from patients, employers, and taxpayers while hiding behind layers of opaque pricing schemes that would make a Vegas card counter blush[1][2].

But the house of cards is crumbling. New Trump administration regulations, Federal Trade Commission lawsuits, and Congressional investigations have exposed what many suspected: PBMs have been systematically inflating drug prices while pretending to lower them[3][4]. And now, two small-cap companies—DataVault AI (NASDAQ: DVLT) and Wellgistics Health (NASDAQ: WGRX)—have developed blockchain technology that could render the entire PBM cartel obsolete.

For investors, this represents a rare "category killer" opportunity: a chance to profit from disrupting a $600 billion industry that's ripe for demolition.

The PBM Cartel: A $7.3 Billion Shell Game

Three companies control 75-80% of prescription drug processing in America: CVS Caremark (CVS Health NYSE: CVS), Express Scripts (The Cigna Group NYSE: CI), and OptumRx (United Health Care NYSE: UNH). These aren't healthcare companies—they're extraction machines masquerading as middlemen.

How the scam works:

Spread Pricing: The PBM tells a pharmacy it will reimburse $10 for a drug, then charges the insurance company $15, pocketing the $5 "spread" while patients remain in the dark about the true cost. This isn't negotiation—it's price-fixing with extra steps.

Rebate Manipulation: PBMs receive percentage-based rebates from drug manufacturers. Higher list prices mean bigger rebates, so PBMs systematically exclude lower-cost alternatives in favor of expensive drugs. The FTC found that insulin prices increased 1,200% (from $21 to $274) between 1999 and 2017 specifically because PBMs chased higher rebates while millions of diabetics rationed their medication[1].

Ghost Company Fee Laundering: Recent investigations exposed PBMs using shell companies and Group Purchasing Organizations (GPOs) to hide billions in fees. They promise "100% rebate pass-through" to employers, then route funds through Swiss-based subsidiaries that collect additional "administrative fees" never disclosed to clients. It's money laundering in plain sight.

The numbers are staggering: The FTC's latest report shows the Big 3 PBMs marked up generic specialty drugs by thousands of percent and extracted $7.3 billion in excess revenue between 2017-2022 just from their own affiliated pharmacies. That's pure profit extracted from sick people buying medication.

The Regulatory Sledgehammer

The scam worked beautifully—until it didn't. Multiple regulatory and legal attacks are now converging:

Congressional Perjury Accusations (August 2024): House Oversight Committee sent letters to CVS, Express Scripts, and Optum executives accusing them of providing false testimony under oath. The letters specifically cited evidence contradicting executive claims that PBMs don't steer patients to their own pharmacies or manipulate contracts.

FTC Antitrust Lawsuit (September 2024): The Federal Trade Commission sued the Big 3 PBMs for artificially inflating insulin prices through their "perverse drug rebate system." The complaint alleges systematic exclusion of affordable alternatives to maximize rebate revenue.

DOL Transparency Rule (February 2026): The Department of Labor mandated full disclosure of PBM compensation to self-insured employers covering 90 million Americans. This directly targets spread pricing, hidden rebates, and clawback schemes.

Consolidated Appropriations Act (CAA 2026): This legislation banned spread-based compensation, mandated rebate pass-through, and imposed extensive audit requirements. For PBMs that historically made most revenue from spread pricing and rebates, this is an existential threat.

$10 Million Antitrust Verdict (January 2025): AIDS Healthcare Foundation won arbitration against Prime Therapeutics for price-fixing with Express Scripts. The arbitrator found federal and state antitrust violations and permanently blocked the collusive arrangement.

The regulatory noose is tightening. UnitedHealth—owner of OptumRx—reported its first annual revenue decline in three decades in January 2026. These aren't cyclical headwinds. This is structural demolition of a business model built on opacity.

Disruptors Using Blockchain as PBM Kryptonite

Here's where Wellgistics Health (NASDAQ: WGRX) and DataVault AI (NASDAQ: DVLT) enter the picture with a technology that solves the exact problem regulators are trying to fix: transparency.

The Digital Prescription Revolution

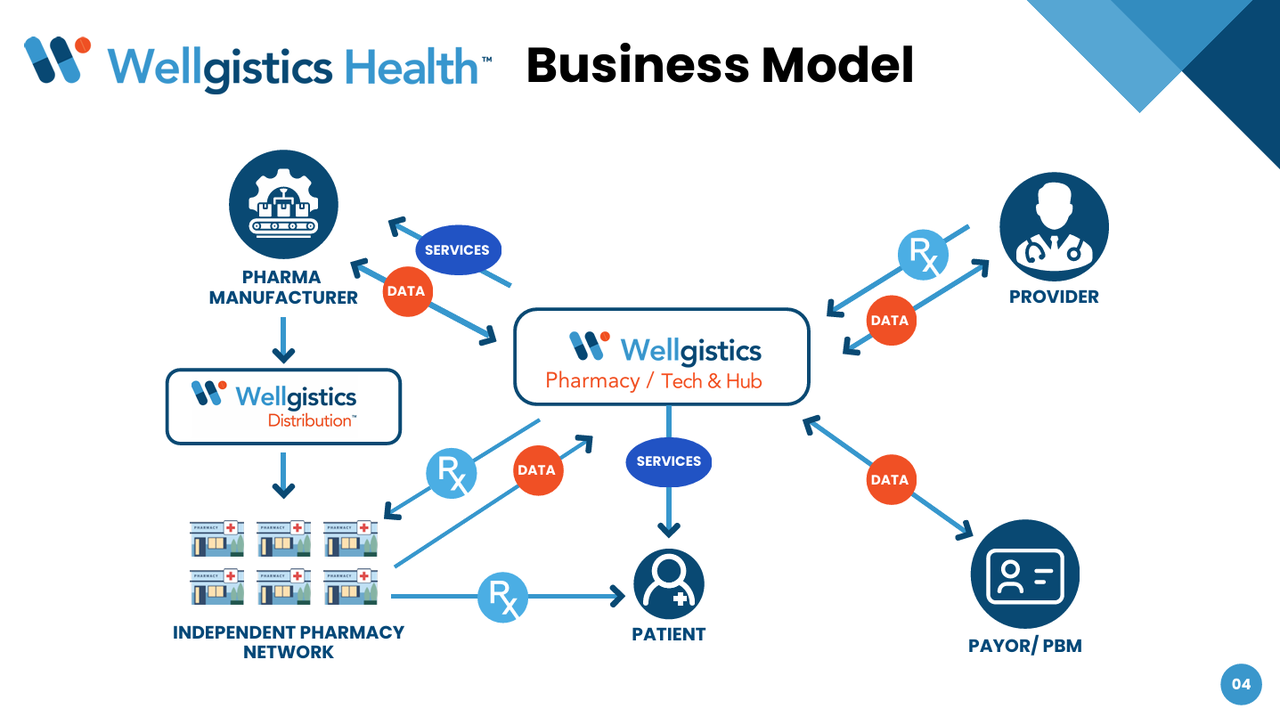

Wellgistics' PharmacyChainTM platform, built on DataVault's patented blockchain infrastructure, creates an immutable "Digital Twin" of every prescription from manufacturing to patient pickup. Every transaction, modification, price point, and dispensing event is permanently recorded on a decentralized ledger.

Why this obliterates the PBM advantage:

Built-In Transparency: Blockchain records show the exact cost at every step—manufacturer price, distributor markup, pharmacy reimbursement, insurance charge. No more spread pricing because everyone sees the same ledger.

Automated Auditing: Smart contracts automatically verify and process claims in 60 days without manual audits. The CAA 2026's expensive audit requirements become irrelevant—the blockchain provides a permanent, tamper-proof audit trail on every single transaction.

Elimination of "Doctor Shopping" Fraud: The "pick-up tag" feature timestamps exactly when and where medication is dispensed, ending duplicate prescriptions and fraudulent refills—problems that cost insurers billions annually.

Quantum-Resistant Security: DataVault's quantum-key encryption ensures patient data remains secure even against future technological threats. This isn't just regulatory compliance—it's future-proofing against cyber attacks that plague centralized PBM databases.

The Intellectual Property Fortress

DataVault AI holds over 70 patents governing blockchain tokenization and real-world asset security, including the Information Data Exchange (IDE) technology that enables prescription digitization. Wellgistics secured an exclusive license for this IP in the commercial drug distribution industry.

First-mover advantage: No competitor can replicate this technology without either licensing from DataVault or spending years developing around the patent portfolio. Every major PBM facing regulatory pressure to implement transparent, auditable systems will need to either build inferior alternatives or license PharmacyChain technology.

Licensing potential: The patents underlying PharmacyChain could be worth billions if just a fraction of the $600 billion prescription market adopts blockchain verification. Even capturing 5% of transaction fees in a transparent, automated system would generate $30 billion in annual revenue across the platform.

The GLP-1 Gold Rush Timing

Wellgistics isn't just building infrastructure—they're positioning for the biggest pharmaceutical product launch in decades: GLP-1 medications for weight loss and diabetes (Ozempic, Wegovy, Mounjaro).

The rejection rate for the weight/diabetes drugs as a class is 62.4% based on a 2024 AJMC article. The pool of rejected patients is actually larger than existing patients. Since the GLP-1 drugs are so expensive the PBM’s excluded them or placed them on a specialty tier that required coinsurance. Another tactic utilized was to require “prior authorization” by verifying the employees BMI along with documented comorbidities. While PBMs are the main reason for rejection, many employers concerned about the cost of health coverage classify weight-loss drugs as cosmetic or lifestyle treatments, and therefore exclude them from employee health plans.

GLP-1 drugs from Eli Lilly (NYSE: LLY) and Novo Nordisk (NYSE: NVO) currently face massive friction from PBM "prior authorization" delays—deliberate administrative hurdles that slow prescriptions and protect rebate-paying incumbents. Wellgistics' EinsteinRx AI platform automates prior authorization, eliminating the bottleneck that prevents patients from accessing these high-demand medications.

The arbitrage opportunity: By reducing administrative friction and increasing prescription fulfillment speed, Wellgistics captures more transaction volume in the fastest-growing pharmaceutical category. They're essentially installing a toll booth on the GLP-1 highway right as traffic is exploding.

Network Effect and Distribution

Wellgistics already partners with over 6,500 independent pharmacies in their network[14]. As PBM practices squeeze independent pharmacies (the FTC documented systemic underpayment to non-affiliated pharmacies)[10], these independents have strong incentive to adopt a platform that provides fair, transparent pricing.

Every pharmacy that joins makes the network more valuable. Every prescription on PharmacyChain creates data that trains the EinsteinRx AI to process future authorizations faster. This is classic network effect economics in a market where incumbents are bleeding market share to regulatory pressure.

The Investment Thesis: Asymmetric Upside

Bear case risks:

- Technology adoption slower than expected

- EstablishedPBMs develop competitive blockchain solutions

- Regulatory environment shifts away from transparency mandates

Bull case catalysts:

- PharmacyChain launch in coming weeks could demonstrate proof-of-concept

- Major PBM forced to license technology due to compliance pressure

- State-level mandates requiring blockchain prescription tracking

- Medicare/Medicaid pilot programs adopting transparent verification

- Continued legal pressure forcing PBM unbundling

- Highly shorted and considered a zero borrow stock

Valuation disconnect: CVS Health trades at a $75 billion market cap despite its PBM division facing existential regulatory threats. If Wellgistics and DataVault capture even 2% of the prescription processing market through licensing and direct platform usage, the current valuations represent enormous upside.

The Buffett-style moat: DataVault's patent portfolio creates a genuine competitive advantage—not from brand loyalty or economies of scale, but from legal exclusivity on the technology that solves regulators' exact concerns. When the government mandates transparency and auditability, there's one licensed platform ready to deploy.

Why This Matters Beyond Returns

For years, insulin users rationed life‑saving medication because pharmacy benefit managers (PBMs) prioritized rebate economics over affordability—leading to preventable harm. Employers absorbed billions in opaque fees they never agreed to. Independent pharmacies shuttered as PBM‑owned chains manipulated reimbursement formulas to their advantage.

The PBM cartel didn't emerge from market efficiency—it emerged from regulatory capture and information asymmetry. A blockchain‑based model doesn’t just disrupt the PBM structure—it renders their core value proposition obsolete.

For investors, the opportunity is clear: profit from demolishing a rigged system while funding a technology that could genuinely lower drug costs and improve patient outcomes. That's not corporate PR spin—that's what happens when you replace opacity with transparency and cartels with open networks.

The prescription drug underworld is being dragged into sunlight. The only question is whether you're positioned to profit from what happens next.