Capex Unsustainable for Mag 7

Welcome to MktContext! I am a professional money manager, trader, and investor who has been timing and beating the market for over a decade. We specialize in predicting market direction by studying the economy and market signals. Join 12,000 subscribers at MktContext.com for our weekly deep dives and analysis!

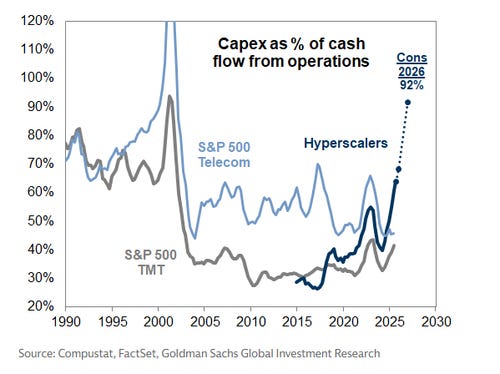

Capex by hyperscalers is set to reach 92% of cash flow (chart below). AI spending is effectively soaking up all excess cash generated by these lucrative businesses. As a result, stock performance is tied to their ability to monetize investments — by demonstrating revenue growth.

For example: Microsoft fell -10% because their earnings report showed disappointing cloud revenue growth. Amazon fell -6% because revenue guidance was unexceptional. In contrast, Meta rose 10% on the back of higher revenue guidance, despite a big increase to capex. Google had better-than-expected cloud growth, which also justified its massive capex increase.

As you can see, big capex spending in itself isn’t good or bad, but it must be accompanied by evidence of profitability to translate to higher share price.

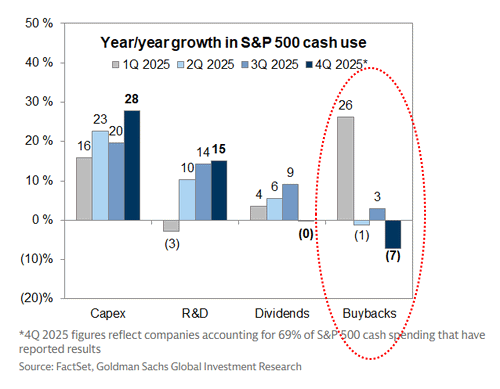

The other issue with diverting all cash flow to capex is it leaves little to buy back their own stock with. Given the copious amounts of idle cash they had before, stock buybacks were previously a major source of buying support. No buybacks means no price support. This explains the Mag 7’s awful stock performance in recent times.

Here's our contrarian thesis: The capex walk-back is going to follow soon. This will lift all Mag 7 stocks and therefore the Nasdaq as well...

Continue reading at MktContext.com to see our trades and portfolio.

Join 12,000+ macro investors who get these insights before the mainstream media catches on!