2/27 Market: Flows Analysis and Trigger Points for S&P Sell-Offs

From the TightSpreads Substack.

February 27, 2026

A hotter-than-expected producer price index (PPI) print with pricing rising 0.5% m/m versus 0.3% m/m expectations, widening High Yield credit spreads (+25bps w/w), and lingering digestion of NVIDIA’s earnings created a risk-off rotation this week. Despite the market remaining firmly inside its YTD trading range (~6800-7000), the moves underneath were sharp and fast: Cyclicals vs Defensives posted its worst week of the year (-3.4%), Beta names lagged (-3%), and Industrials, Tech, Discretionary and Financials all closed lower. Yet defensives and the Hard Asset Limited Obsolescence basket (MSXXHALO) held up well (+2% each), while the “new $1T club” (LLY +4%, WMT +4%) continued to grind higher. To understand this week’s flows and where it goes next, read the market flows section in the second half of this article.

The numbers (Feb 27, 2026 close):

S&P 500 (SPX) -0.4%, Nasdaq (NDX) -0.2%, Russell 2000 (IWM) -1.2%

Software vs Semis pair (MSZZSFSE) +1.5% — first outperformance in five weeks

AI Tech Beneficiaries (MSXXAIB) -1%, NVDA -6.6% w/w

New $1T club strength: LLY +4%, WMT +4%

Defensives +2%, MSXXHALO +2%

Financials -2.5% led lower by Alts (MSXXALTS -8%) and BDCs (MSXXBDC -4.5%)

10y yields crossed below 4%; SPX skew rose to highest since Aug 5 2024 vol panic

The headline indices barely moved because extreme dispersion is masking the rotation. High-beta, cyclical, and AI-exposed names sold off aggressively on growth and credit concerns, but real-asset defensives and hard-asset themes absorbed the flow. To note on financials underperformance, there are concerns of Software exposure, dividend cuts + asset sales at select BDCs and uncertainty on the left tail risks of AI on the labor market showed through in credit sensitive areas. A prime example of applied pressure include the headlines on AI-driven headcount reductions with XYZ cutting 40% of their work force – though an important caveat is that XYZ over-hired materially during COVID.

This is exactly the environment we have been flagging since early February: the market is broadening, de-risking crowded longs, and rotating into under-owned, heavy-asset names.w

Post-NVDA digestion set the tone

Even with what MS Research’s Joe Moore called “the cleanest beat in history,” NVDA and the broader AI stack saw immediate profit-taking on Thursday and Friday. The street focused instead on three bigger questions: durability of hyperscaler AI capex, pressure on their FCF profiles, and whether the massive ROIC will ultimately justify the spend. A low single-digit percent beat on revenues for NVDA does not move the needle much on eps (earnings per share), therefore the reaction on selling/shorting where there are other names in tech that can out-earn has made NVDA a funding source for hedge funds (i.e. hedge funds short NVDA to go long other tech names). It’s a common theme for hedge funds where finding short alpha may be scarce but have net exposure (long and shorts) to balance. Asset-heavy AI names (MSXXAHVY) fell -5% w/w (CRWV -10% on margin miss despite strong bookings). PB Content showed -2.6z long reduction in Semis and -3z short reduction (covering) in Software on Thursday — classic rotation mechanics.

Market flows confirm the de-risking and rotation

Long/Short Equity Hedge Funds

Hedge funds added to both longs and shorts in size this week as US equity dispersion hit its widest span in two decades.

Net leverage: 56% (75th %-tile last year, up +3% WoW)

Breaking this down for readers who are unfamiliar with hedge funds:

Net leverage is simply (long positions less short positions) ÷ Capital.

At 56%, for every $100 of fund capital the average US equity long/short manager is net long $56. Usually firms have a mandate to keep this relatively leveled near 50/50 or take tilts, this 56% is a moderately bullish long tilt.

Gross leverage: 214% (86th %-tile last 12m, 97th %-tile since 2010) — still very elevated

Gross leverage is (long positions + short positions) ÷ Capital.

At 214%, for every $100 of capital managers have $214 of total exposure on the books.

Both figures express hedge funds are still high gross invested in the market and only moderate net long = classic dispersion regime. Managers are not making a huge directional bet on the market going up (net 56% is not extreme), but they are playing the rotation aggressively: adding longs to under-owned areas (HALO, defensives, quality software) while keeping or even adding shorts in crowded AI/semi/momentum names. The +3% WoW net increase despite the week’s risk-off tone shows conviction in the broadening story — they are not de-risking overall; they are repositioning within the market. But the 97th %-tile gross leverage means fragility is high: if the rotation reverses or vol spikes, forced unwinds can be violent (we’ve seen this in early Feb).

Americas Hedge Funds (L/S) Net Performance:

MTD: +0.7% outperforming the S&P 500: -0.3%

YTD: +2.1% outperforming the S&P 500: 0.4%

Quant funds

Systematic macro strategies (CTAs, vol control, risk parity) have sold an estimated $80-90bn of global equities in the last month (-1.0 z-score) and are expected to sell another ~$5bn next week.

Corporate buybacks

Corporate buybacks hit the busiest week in over 2.5 years (notionals +75% w/o/w, fourth consecutive increase), led by Software and Financials — companies clearly undeterred by the AI narrative noise. 60% of Buyback flow currently consists of 10b5-1 plans. A 10b5-1 plan is a pre-scheduled, SEC-compliant buyback program that a company sets up in advance (often weeks or months earlier). Once the plan is active, the repurchases execute automatically on a fixed schedule — e.g., “buy up to $50mm of stock every Tuesday if the price is below $X” — regardless of current news, market volatility, earnings, or sentiment.

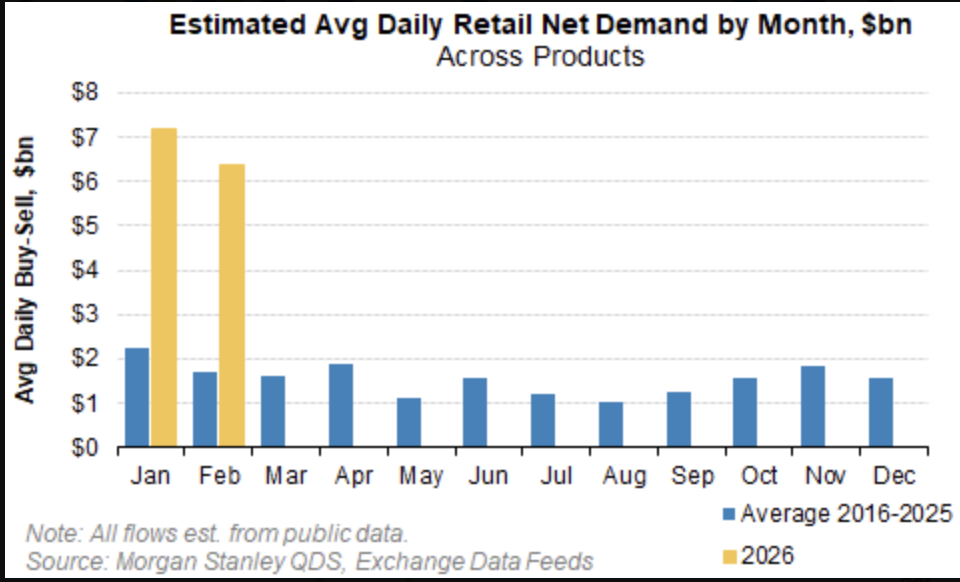

Retail (everyday investors)

Retail demand moderated to $6.3bn per day in February (down 12% m/m from January’s $7.2bn). This is milder than the historical seasonal drop of 20-25%, but any further slowdown into Tax Day could add pressure to momentum pockets (Retail Favorites basket MSXXRFLO already -11% since Jan 22 peak).

Gamma

Gamma measures how much delta (directional exposure) changes when the market moves. Option dealers are long gamma overall ($3bn per 1%), but levered ETFs (TQQQ, etc.) are very short gamma ($8-9bn per 1%). The net result is now that the street as a whole is short gamma.

The profile is asymmetric:

On the upside, dealers become very long gamma (peak +$25bn per 1% of SPX increase near 7020) — they buy strength, which caps big rallies.

On the downside, they flip to short gamma at 6675 — they sell weakness, which can accelerate drops.

Right now it is dampening volatility in both directions near current levels, but the downside flip point (6675) is only ~2.5% away. If we break lower, dealer hedging could add fuel to the fire.

ETFs

ETF flows tilted hard international: EM Equity +$9.7bn (3.7 1Y z-score), Intl Equity +$12.6bn (2.3 1Y z-score), plus strong Gold +$3.7bn and Commodities ex-Gold inflows — a risk-off rotation out of US growth into real assets and non-US.

Dispersion at two-decade extremes

The spread between the top 50 and bottom 50 performers in the S&P is now ~68% — widest since at least 2005 and above the 2009 peak. Single-name realized vol sits in the 90th percentile while index vol remains near 20-year medians. Historically, when this single-name vs index vol gap stays above its 1Y 80th percentile for more than 20 days, forward SPX returns have been weaker or negative. We are now on day 20 through Feb 26. This is not yet a outright sell signal, but it is stretched and explains why the SPX can feel “stuck” even as violent rotations play out beneath the surface.