Gold: $5400 Max Pain as Macro Discretionary Funds Are Back

GOLD FUTURES RE-ENGAGEMENT AND THE VOLATILITY RESET

Sticky Vol Shows Macro Discretionary Bulls Have Returned

EXC SUM.

Authored by GoldFix

Goldman has identified what we believe are the early stages of a Gold Trading/ investment cycle where Macro Discretionary dominates as only they can. Nothing is guaranteed in early assessments, but there you have it…

Macro discretionary participation is beginning to re-enter gold after the volatility purge that cleared legacy positioning. With realized vol collapsing from extreme highs and option exposure running well below last year’s peak, the market has reset structurally. Directional flow is returning in measured form, primarily through selective convexity accumulation. Even if tactical for now, the re-engagement of macro buyers reduces liquidation risk and reintroduces upside optionality into the futures complex.

Open interest has cratered, Macro Discretionary has dry powder, and dealing banks are definitely trading scared after last months squeeze and purge.

Our piece focuses primarily on the futures and directional positioning dynamic with an options kicker for fans of short squeezes.

FUTURES RE-ENGAGEMENT AFTER POSITION CLEAN-UP

Goldman Sachs’ recent trading-desk commentaries (by Robert Quinn and company) frames the current gold market through the lens of derivatives positioning rather than outright macro narrative. The dominant theme is structural consolidation after an extreme volatility spike, with futures and options flows beginning to re-engage as spot stabilizes around the $5,000 handle.

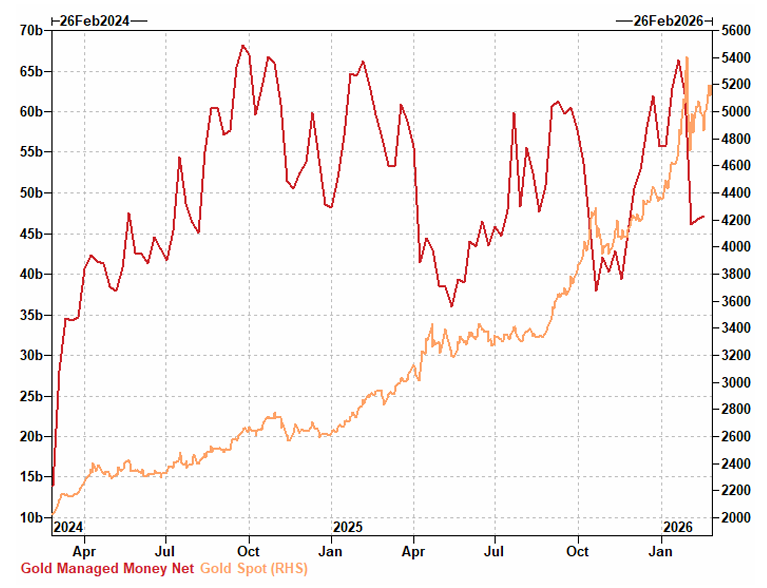

Gold’s advance into the $5,000 region forced a significant unwind of prior positioning. The desk notes that earlier speculative structures were effectively cleaned up through profit-taking and knock-outs. What remains is a market that has compressed from panic-volatility extremes into a consolidation range.

Gold Managed Money Net Positioning vs Price…

“Pre-existing positioning was cleaned up via a mix of both profit-taking trades being knocked out… we are now seeing some ‘consolidation’.”

Two-week high-frequency realized volatility fell sharply from 30-year highs near 69 vol to roughly 29 vol as price stabilized. This matters for futures because gamma exposure and option convexity directly influence dealer hedging behavior in the underlying contract.

As volatility collapsed, outright directional option flow slowly returned. Upside expression shifted away from aggressive knock-out structures toward a blend of vanilla calls, European knock-outs, and digital structures. Macro positioning through options remains materially below last year’s highs, estimated at 30–40% of prior peak activity.

That reduction in macro option exposure implies that futures markets are no longer heavily constrained by crowded positioning. The clearing of legacy structures reduces forced hedging flows and allows for cleaner price discovery.

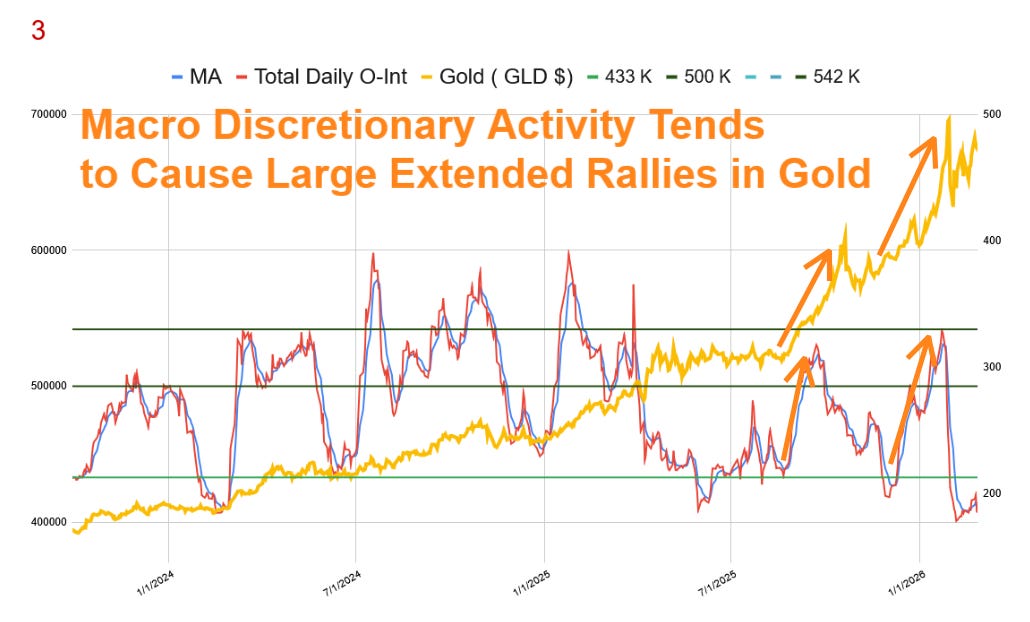

We May Be At The Beginning of a Macro-Discretionary Cycle…

Goldman: Dealing Banks Gamma-Squeezed in January

Insurance Buyers, Gamma-Squeezes, and the Structural Bid Under Gold

“Desk likes picking up convexity on dips in flat price to re-position for a break higher.”

The structural implication is clear. Futures are consolidating rather than reversing. The shift from aggressive knock-outs toward outright optionality reflects a market transitioning from forced repricing to measured accumulation.

THE ROLE OF STRUCTURE IN FUTURES EXPRESSION

A specific structure cited involves a six-month digital call above $6,215 at a defined premium. While the details are tactical, the strategic takeaway is more important. Upside convexity is being reintroduced after a volatility purge.

In English, volatility has bottomed at significantly higher levels as dealers are short vol and reluctant to sell it after getting burned last month

Gold Option Volatility is Now Sticky…

In futures terms, this matters because

Continues here

Free Posts To Your Mailbox