When the Blue Owl Roosts Before the Credit Reckoning…

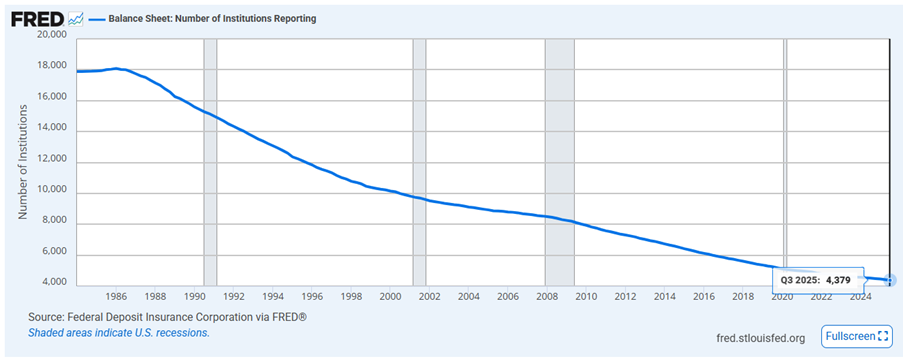

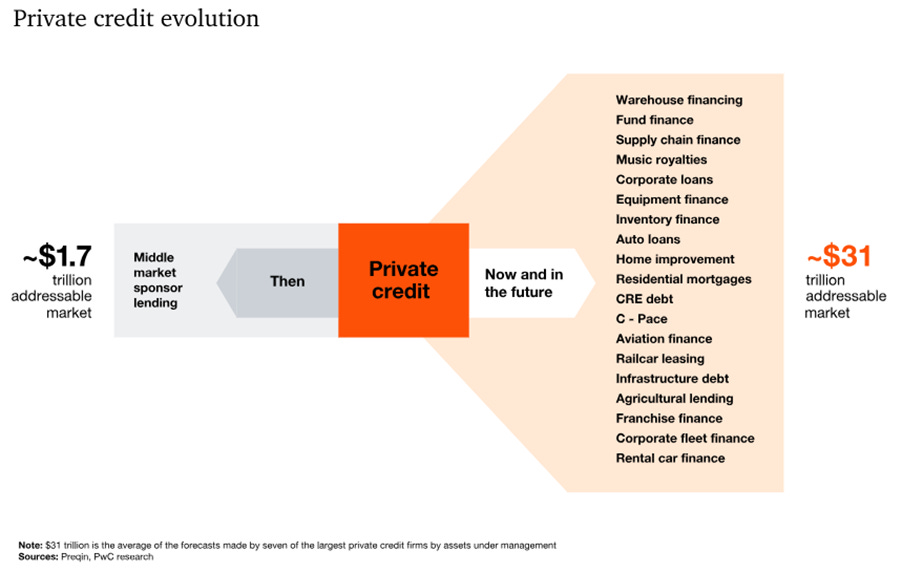

The birth of private credit is inseparable from the evolution — and gradual slimming — of the U.S. banking system. In the decades following World War II, America was home to roughly 13,000 to 15,000 banks, a dense forest of lenders serving businesses of all sizes. Then came the Savings and Loan crisis, which thinned the herd to about 8,000 institutions. A generation later, the Great Financial Crisis delivered a second consolidation wave, reducing the count to roughly 4,400 today. But it wasn’t just the number of banks that changed — it was their scale. The survivors grew larger, more regulated, and more focused on either very large corporate clients or ultra-safe lending. In Confucian terms: when the big fish grow fatter, the pond for the middle fish grows smaller. The result was a widening gap in middle-market lending — precisely the vacuum into which private credit stepped, offering capital where traditional banks increasingly could not, or would not, lend, especially in times of crisis.

https://fred.stlouisfed.org/series/QBPBSNUMINST

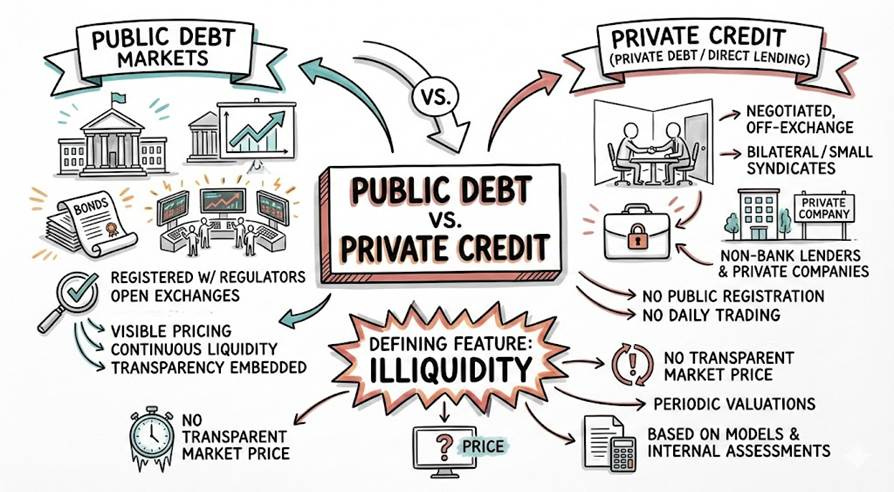

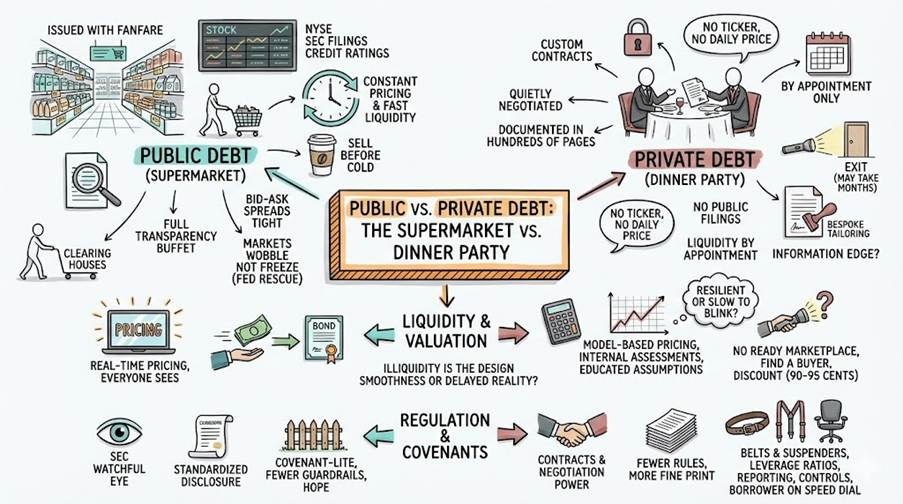

In traditional public debt markets, borrowers issue bonds registered with regulators and traded on open exchanges, where pricing is visible, liquidity is continuous, and transparency is embedded in the structure. By contrast, private credit — also known as private debt or direct lending — operates in a negotiated, off-exchange world. Loans are arranged bilaterally or through small syndicates between non-bank lenders and private companies, without public registration or daily trading. The defining feature of the asset class is therefore illiquidity: there is no transparent market price flashing on a screen, only periodic valuations based on models and internal assessments.

Private credit is basically lending behind closed doors, the nice words for shadow banking. Instead of banks or bond markets, private funds and Business Development Company (BDCs) lend directly to companies — mostly middle-market firms, but increasingly the big kids too. No exchange, no ticker symbol, just a handshake (and a 200-page contract). Deals are customized, floating-rate, usually senior secured, and often come with “extras” like equity kickers or strict prepayment penalties — because if you’re locking up money without a resale market, you want perks. And since there’s no easy exit button, lenders typically stick around until maturity — sometimes with a seat at the table.

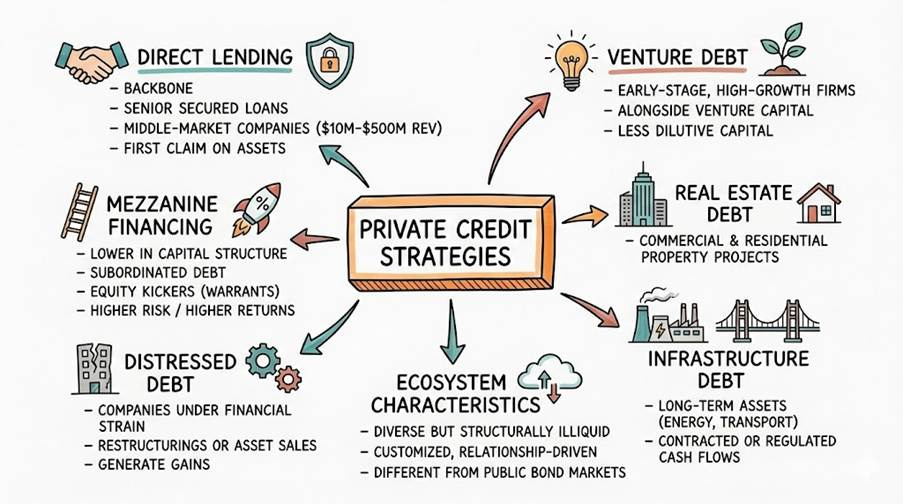

Within the bespoke Private Credit universe, several strategies coexist. Direct lending forms the backbone, providing senior secured loans to middle-market companies — typically firms generating between $10 million and $500 million in revenue — with lenders holding first claim on assets in the event of default. Mezzanine financing steps lower in the capital structure, offering subordinated debt often enhanced with equity kickers such as warrants, compensating investors for higher risk with higher potential returns. Distressed debt targets companies under financial strain, where lenders aim to generate gains through restructurings or asset sales. Venture debt supports early-stage, high-growth firms alongside venture capital, offering less dilutive capital. Real estate debt channels private financing into commercial and residential property projects, while infrastructure debt funds long-term assets such as energy facilities and transport systems, typically backed by contracted or regulated cash flows. Together, these segments form a diverse but structurally illiquid ecosystem — customized, relationship-driven, and fundamentally different from the public bond markets they increasingly rival in size.

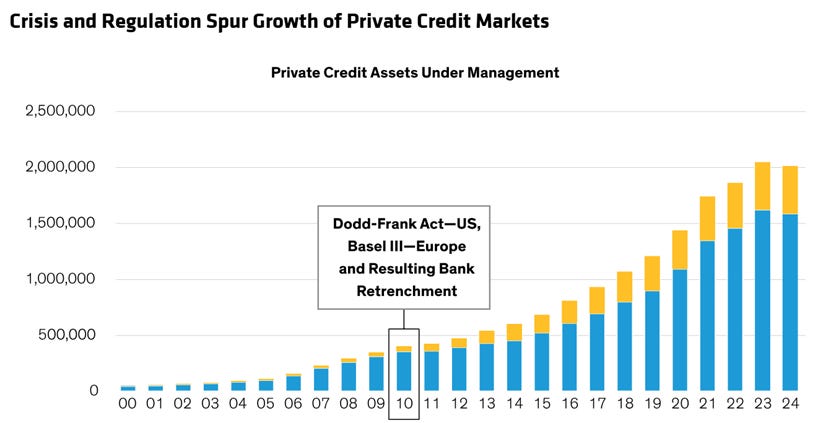

Private credit didn’t appear by accident — it was basically the financial system’s “nature abhors a vacuum” moment after the 2008 crisis. When Dodd-Frank Act and Basel III told banks to hold more capital, reduce leverage, and behave themselves, traditional lenders looked at middle-market loans and politely said, “No, thank you.” Balance sheets became precious, regulators became vigilant, and return-on-equity math became less forgiving. So, banks stepped back — especially from anything that looked remotely adventurous. Right on cue, private equity firms and credit funds marched in like well-dressed opportunists at a clearance sale. Pension funds hunting for yield, insurers craving spread income, endowments seeking diversification — all found comfort in private credit’s promise of 8–12% returns with valuations that moved about as calmly as a swan (at least on paper). Thanks to the Federal Reserve flooding the system with liquidity and pinning rates near zero, government bonds paid next to nothing. Private credit suddenly looked less like an alternative and more like the only party in town serving dessert.

Private credit prospered because it moved with the decisiveness of a well-trained general approving in days what banks pondered for months. It offered flexible covenants, tailored repayment terms, and discreet capital, all highly valued in competitive situations where speed and certainty win the mandate. For middle-market companies—too large for small banks, too small for bond markets—private credit became the pragmatic path: swift, adaptable, and respectfully silent.

https://www.pwc.com/us/en/industries/financial-services/library/private-credit.html

https://www.pwc.com/us/en/industries/financial-services/library/private-credit.html

The difference between public and private debt is a bit like the difference between shopping at a supermarket and negotiating at a private dinner party. Public bonds are issued with regulatory fanfare, trade on exchanges like the New York Stock Exchange, come with SEC filings, credit ratings, clearing houses — the full transparency buffet. Prices update constantly, bid-ask spreads are tight, and if you want to sell, you can usually do it before your coffee gets cold. Even during the 2020 panic, markets wobbled but never truly froze — especially once the Federal Reserve stepped in with its rescue toolkit. Private debt, on the other hand, is bespoke tailoring. Every loan is a custom contract, negotiated quietly, documented in hundreds of pages, with no ticker symbol and no daily price. There are no public filings, rarely any ratings, and liquidity is more “by appointment only” than on demand. Sophisticated lenders may enjoy the information edge — but when it comes time to value or sell the loan, the absence of a visible market can feel less like exclusivity and more like being the only bidder at your own auction.

Private credit lives in a liquidity universe where the exit door is technically there — but you may need a flashlight and a few months to find it. Unlike public bonds, where market makers and exchanges keep things moving, private loans have no ready marketplace. If you want to sell, you must locate a specific buyer, convince them to like your particular loan, hand over piles of documents, and usually accept a discount for the privilege. Even healthy loans often trade at 90–95 cents on the dollar in calm times, and far lower when markets get nervous. In stress periods, bids can feel less like negotiations and more like clearance sales. Illiquidity here isn’t a bug — it’s the design.

Valuation follows the same philosophy. Public bonds enjoy real-time pricing — screens flash, spreads move, and everyone can see the verdict instantly. Private credit relies on models, internal assessments, and educated assumptions. When public markets dropped sharply in early 2020, many private portfolios appeared serenely stable — raising the awkward question: were they resilient, or simply slow to blink? Model-based pricing can smooth volatility, but sometimes smoothness is just delayed reality wearing a polite face.

Regulation also tells two different stories. Public debt issuers operate under the watchful eye of the SEC, standardized disclosure rules, and securities law. Private loans, by contrast, are governed mainly by contracts and negotiation power. That flexibility allows customization — but also shifts responsibility onto the sophistication of the participants. Fewer rules, more fine print.

Finally, covenants. Public bond investors have, over time, accepted increasingly “covenant-lite” structures — meaning fewer guardrails. Private lenders, however, prefer belts, suspenders, and sometimes a seat at the boardroom table. They impose leverage ratios, reporting requirements, dividend restrictions, and operational controls. In public markets, you buy the bond and hope. In private credit, you lend the money — and keep the borrower on speed dial.

Public debt is the open-air market of finance — mutual funds, pension funds, insurers, hedge funds, and even retail investors all mingle freely, creating liquidity through sheer diversity. If one investor wants out, another usually wants in. Private credit, by contrast, is more of an invitation-only dinner. The guest list features pension funds hunting illiquidity premiums, insurance companies matching long-term liabilities, sovereign wealth funds, endowments, and family offices — all sophisticated enough to lock money away for years without technically panicking. According to the Federal Reserve Board Financial Stability Report, pensions alone account for roughly a third of private credit assets, with...

Read more and discover how to trade it here: https://themacrobutler.substack.com/p/when-the-blue-owl-roosts-before-t…

Visit The Macro Butler Website here: https://themacrobutler.com/

Join The Macro Butler on Telegram here : https://t.me/TheMacroButlerSubstack

You can contact The Macro Butler at info@themacrobutler.com

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence