The new structural cycle driving gold and Bitcoin

This discussion with Charlie Morris of ByteTree Asset Management explores how gold, Bitcoin, and broader markets are being shaped by deeper monetary forces rather than short-term narratives.

We discuss market cycles, asset volatility, central bank behavior, and why gold continues to reassert itself as a monetary asset during periods of structural stress.

Follow Monetary Metals on X: @Monetary_Metals

Follow Charlie Morris X: AtlasPulse

Transcript

Monetary Metals:

Welcome back to the Gold Exchange podcast. My name is Ben Nadelstein. I am joined by our good friend Charlie Morris. Charlie is the founder and CEO of ByteTree and the creator of the BOLD ETF, which combines Bitcoin and gold. He joins us today to talk all things gold, macro, and Bitcoin. Charlie, welcome back to the show.

Charlie Morris:

Great to be here, Ben. Thank you.

Monetary Metals:

Charlie, let’s start off with a big Bitcoin question for the show. Bitcoin has seen its price come down in half from highs in the 120s, now into $60 range. Is Is this the bottom of Bitcoin?

Is this just the beginning of the end for Bitcoin? Where is the Bitcoin story right now for Charlie Morris?

Charlie Morris:

Ben, is this the bottom for tech?

Monetary Metals:

Good question. I think the answer is probably not. So it sounds like Charlie’s saying not the bottom for Bitcoin either.

Charlie Morris:

So I think that tech is a big bubble, and it’s been brewing for a long time, and that’s going to go on. The unwinding of tech is going to go on for a while. But that’s the correlation.

We’ll get to gold in a minute. But gold used to be correlated with 20-year tips for years and years and years, and then it wasn’t. It just went through the roof. It decoupled in 2022. And it’s still correlated. Gold still correlated with real interest rates. And we’ll come to that.

But Bitcoin goes up and down with the tech sector. But guess what? It always wins in the end. So it It goes up more, it goes down more, but net net, it’s the king. I think that’s going to happen again. So, yeah, we’re in the down cycle. That’s not much fun for Bitcoin holders. But at some point, tech will turn. And when it does, Bitcoin will be in front. I think that’s my simple view.

Monetary Metals:

Let’s get a little bit more detailed and more nuanced. You’ve heard some arguments there’s this quantum computing revolution that could potentially harm Bitcoin. The supply, the 21 million cap might not be so fixed. Where did these stand in to the Bitcoin narrative? Are they important?

Are they unimportant? And major macro themes will decide Bitcoin, or will these more technical matters really decide the price of Bitcoin going forward?

Charlie Morris:

Well, if people are talking about them and people are worried about them, they matter. It’s as simple as that. I think the quantum threat is probably overstated. We had just the last difficulty adjustment. We had a 15 % increase in the hashing rate required to mount Bitcoin. To mine Bitcoin. And it’s one terapeta something hash, and it’s 21 zeros. So we need to know it’s 21 zeros per second.

So one and then 21 zeros per second to my Bitcoin. I don’t really understand. After about a thousand, I’m lost. And maybe I can go a bit higher than a thousand, but not a lot higher. And so these are big numbers in terms of speed. Lead. That’s where we are. Quantum, when it comes in, it could be years and years and years away. It’s a threat to the early wallets, the 2009, 2010 wallets.

The fix you can put into the system is just to make the password longer or the private key. I mean, this could be done. We’ve had upgrades to the Bitcoin network before. We can have more. So I don’t think quantum is a great threat. And then, of course, who’s going to get a quantum computer?

Some government or What are they going to do? First thing they’re going to do, break Bitcoin. I doubt it. I think they’re going to be bigger threats. They would have to get into the hands of the black hats, the baddies on the Internet in North Korea and places like that.

I think that they’re a long way off, if ever. So Bitcoin, first and foremost, could just make the password longer. Not a problem. And the other thing is that it’s going to be a very long time before a baddy gets hold of a quantum computer.

Monetary Metals:

This is why I love getting to interview you, Charlie. Okay, another question on the Bitcoin front. We’ve seen these halving cycles. There’s been this trend.

Do you think the halving cycle is still an important discussion point when it comes to Bitcoin? Is that really priced in for the rest of time?

How important is that framework to you when it comes to thinking about the Bitcoin price?

Charlie Morris:

Well, cycles have been with us through history forever, mostly outside of finance and inside of finance, and so they’re a thing. We just agreed need the Bitcoin and tech are correlated. Right. So to drive technology sector doesn’t seem very likely. And so we’ve all got this halving cycle in our minds. A year and a half ahead of Loving everyone starts buying Bitcoin.

Then you have the hoohah, and then everyone gets bored. And you get… So that’s the four-year cycle. Of course, in the 2012, ’16 cycle, no one knew it was a cycle. In ’16 to ’20, a few people might have mentioned it, but I don’t remember it, and I was around. Then Plan B made it really famous in 2020, having seen two cycles.

And then the last cycle came about, and it was exacerbated by SBF and that thing. And this time everyone knows. The Financial Times and the Wall Street Journal know. So if they know, then everyone knows, right? So now it’s such an established theory. It’s probably irrelevant. I think that’s one way to think about it. And just go back to the tech sector. Bitcoin can’t possibly, one and a half trillion dollar Bitcoin or 1.

2 trillion dollar Bitcoin, can’t possibly drive the 30, 40 trillion dollar tech sector globally. So it’s a bigger question about why is there a four year cycle?

Well, there’s a thing called the Juggler wave, which has been around for years, and that was basically based around the US presidential cycle. Before Bitcoin came along, people used to talk about that all the time. There is a cycle in markets.

The idea is that a President promises nice things on the way into power. It’s a bit nice in year one, then gets nasty to actually do the things he wants to do. And then when it comes to re-election, they do nice things again. So there’s this logic to it. And you can take that cycle back to half a century. And there are events around the four years. I mean, it’s not perfect, but there it is.

And if we agree that Bitcoin is a major expression of market liquidity or excess liquidity, then it makes sense that the Bitcoin would feel it more than other things, right? When the stock market goes crazy these days, it’s the tech sector that feels it the most. You with crazy new ideas that may or may not be useful.

But even if they are useful, they go to 200 PE and all that. And so it’s hot money, hot money all over the place. And Bitcoin is a part of that.

Monetary Metals:

And what do you think about this AI narrative? It seems like it sucked a lot of air out of the room from the crypto story being the next big thing. Now, maybe AI is the next big thing. We need data centers not to mine Bitcoin, but to mine for GPUs and get AI infrastructure ready.

How much do you think that story has played out into the crypto bear market where the mind share of most investors is now thinking about the new hot tech, which is AI, rather than the new hot tech, which was the cryptocurrencies?

Charlie Morris:

Well, We nailed it. I mean, it’s exciting competition. I hope we’re going to get on to gold and silver soon. But they provide competition for Bitcoin. They haven’t done much in the last few years, but now they have. All the crazies have gone to silver. I used to say, five years ago, people said, Why is silver in the dark house? Well, the crazies are in Bitcoin. They’re buying Dogecoin. They’re buying this stuff.

Give them some momentum and they’ll come back. And they did. They took a couple cycles, whatever you’re going to call it. It took some time, and then…

And that’s where the action has gone back. Commodities always come and go. They’re always good fun when they’re going. And then you have a very long wait before the next one. But We were in a commodity cycle. I don’t know if it was the beginning or the end, but who knows?

But it’s exciting. Commodity is very exciting right now. And so Bitcoin has got the competition, as you say, in AI and in metals, and no doubt, one or two other things. It might be oil next. Who knows?

Monetary Metals:

In our Gold Outlook report for this year, that is one of the themes we touched on, is this monetary competition. Gold, obviously, really shining this year when it comes to that monetary stage compared to, let’s say, Bitcoin, crypto, even the US dollar.

Where do you see the gold and monetary story in this moment? Obviously, gold can trade just like a speculative asset, or it can trade more like a monetary asset when people are worried about the value of currencies or the value of money. Where do you see the gold and monetary story today in 2026?

Charlie Morris:

Yeah, well, I think the theme that I’ve latched onto in the last couple of years is really this non-OECD central banks increasing their reserves. I mean, it’s not an original story. It’s become well-established.

But in 2022, when we had the change of narrative, flipping from gold as tips, it’s like a 20-year tips, and to something else, that was a challenging time to make those arguments. And let’s go back a bit. The central banks were selling gold from 1980 down to 2009.

And then they had the credit crisis, and they went, Maybe we should have some of that. And then they roll it forward for 2022, and then Russia’s reserve get confiscated, and they go, Maybe we should have some more of that. And so you have the increase of gold reserves from 2009-2022, and And then it increased.

And then the bears say, oh, well, the central banks didn’t buy as much gold in 2025 as they did in the previous two years. And I said, well, did you see the price of gold? They put in a lot more dollars than they did, managed to get so many ounces they previously had because the price went up.

But they’re very motivated. And if you look at the $13 trillion global reserves for the central banks, their gold reserves are about 28 % right now. And the 50-year average is more like 70, 80.

So we’re going back to an era where G7 sovereign debt is not as exciting as it once was or asgilt hedged as it once was. And so people are saying, well, give me the alternative asset.

And limited supply is a thing. It’s no longer for cranks and gold bugs to go on about supply and money supply. I mean, it’s now everyone’s saying it. So it does make sense.

But we have got a gold price that is probably twice its 200-week moving average. And we got a Bitcoin price that’s half its 200-week moving average. And so What does the contrarian do, Ben?

Monetary Metals:

Let’s talk about the BOLD ETF, Charlie. Tell us a bit about how BOLD works. Obviously, you’re one of the people to combine gold and Bitcoin.

Very interesting story here, of course, as we’re seeing high gold prices, maybe low Bitcoin prices. Tell us about the BOLD ETF, Charlie.

Charlie Morris:

BOLD is a risk-weighted approach. Quite simply, if you got $100 and you put 50 into gold and 50 into Bitcoin, it doesn’t take a genius to figure out you got more risk in your Bitcoin 50 than your gold 50. Which is not to say that they can’t both fall. Of course, they can.

But you’d probably have less Bitcoin and more gold. And a very simple piece of financial maths in liquid assets is to use volatility. And so we look at the last year of volatility, 360 day, and then we invert it.

So it’s just called an inverse volatility. It’s fine in any old financial textbook. And you end up with about, at the moment, about a third Bitcoin and two-thirds in gold.

So on any given day or a typical average day, not that average really exists in finance, but it’s quite often you’ll find that Bitcoin would be up 3 % and gold will be down 1 %, or gold will be up 1 % and Bitcoin would be down twice that. You know what I mean? And so you find that the volatility of bold is incredibly low. So you basically get the same volatility You get Bitcoin and gold.

Everyone knows Bitcoin is volatile. Not as volatile as it used to be, but still volatile. And gold, everyone knows it’s low. Not as though as it used to be, it’s going up. But the bold volatility is not in the middle If you look at the Bitcoin and gold, it’s approximately gold.

So you basically put Bitcoin and gold together on a risk-weighted basis, and you get the vol of gold. Yeah? And that’s the exciting bit. And then the other thing is, well, okay, if you do that, well, then the prices move.

You know, Bitcoin goes up, gold goes down, or vice versa. What do you do next month? I’ve no longer got the weights, so you rebalance. And so you take it back to those target weights every single month. You recalculate the target weights every single month, and you rebalance into that weight. And guess what?

We are doing a secret financial strategy called buying low and selling high, which is really, really incredible. And so we sell the one that’s gone up the most and buy the one that’s gone down the most to go back to the target weights. Yeah.

And that little process of on average turnover about 5 % a month on in both directions, probably a bit less than that, probably more like four.

And that adds about 5-7 % per year to the strategy. So you’ve got this tailwind. There is a total return outcome that comes as a result of the low correlation. Now, of course, if you did that with silver and gold, you’d have no outcome.

You just get the average return. It’ll be nothing. If you did with Bitcoin and Ethereum, you’d get nothing. If you did it with US equities and international equities, you’d get nothing because they’re correlated.

But if you did it with assets that are uncorrelated, you’d get something. Now, it’s quite hard to find uncorrelated assets. And Bitcoin and gold are both high return, liquid, alternative assets that have this extraordinary quality when you put them together.

So that’s what this is all about. It’s like, okay, I want to have an alternative asset in my portfolio that’s liquid.

Should I have Bitcoin or gold? And it’s like, well, Okay, monetary metals would probably prefer gold, but it’s okay to have a bit of Bitcoin, too. And if you’re going to do that, then there’s an extra piece that you can add to that by rebalancing.

And of course, It depends on the jurisdiction you live in. But if you live in Europe, or in most countries, there’ll be a capital gains tax event by rebalancing. And so we do it inside our ETF, BOLD, Tickets BOLD, and so that’s rolled up. So that’s nice for investors.

So I just say, well, if you like Bitcoin and you want to sleep at night, own BOLD. You like gold, but you want to pick up the returns a bit long term, then think about bold. But the bottom line is that most people don’t care much for alternative assets.

I mean, they are still a minority sport, incredibly. And then the two big groups, Bitcoin and gold, hate each other. And so the old world don’t like them, and then the Bitcoin and gold people don’t like them. And then little me in the middle in Club Bold is a very minority sport. Everyone hates us.

Monetary Metals:

Well, we love you here, Charlie. I want to ask you about the volatility of gold and the volatility of Bitcoin that you mentioned. Obviously, over time, there’s this argument that the volatility of Bitcoin will go down. Who knows what’s going to happen with the volatility of gold?

Where do you see the volatility story playing in? Does Bitcoin need to be volatile to be interesting, or will lower volatility actually increase adoption of Bitcoin to outpace It’s that negative flow?

Charlie Morris:

Well, let’s look at it. So Bitcoin’s market cap, I’m going to make the numbers up because I can’t remember them. But 10 years ago, the market cap of Bitcoin was not that high. We’re talking billions rather than trillions. A few billions. And the volatility was really high. And as the volatility has been coming down from 100 % down to, let’s call it 40, now in the 30s, the market cap went through the roof, up to 2 Yeah.

So there you go. There’s your answer.

Gold basically had 15, 20 vol for most of its life, apart from 1979, when it pretended to be Bitcoin for a year. And so gold knows how to have volatility as well. It just hasn’t happened for a very long time. And so I think that’s pretty interesting. No, absolutely.

You can be a high return asset without volatility. I mean, NVIDIA and Tesla do have high vol. But you know, Microsoft and Google, much less so. There are plenty of stocks with low vol that have done extremely well over the years. And I think there are probably fewer high vol stocks over the years. Volatility, I always think it’s one of those things A low vol situation is generally what you would associate with a risk-free return, and high vol is what I generally associate with a return-free risk, if that makes sense.

I don’t think you get paid for VOL. It’s one of the things in a fishing market’s hypothesis that’s bullshit. If something is crazy, well, it’s just crazy. It doesn’t mean you need to get paid heavily to own it. You know what I mean? I mean, silver.

Silver has got twice the vol of gold, let’s say, roughly speaking on average over the years. And it’s at the same return. The return of you do not get paid for silver volatility, which is not to say you can’t tactically be bullish like I have been for the last five years.

That’s a different It’s very thick. But you don’t get paid buy and hold long term for an asset being more volatile than the other. I just think that if Bitcoin volatility keeps coming down, it will get more and more adoption and taken more seriously by famous, basically.

Monetary Metals:

I do want to ask you about silver. Obviously, central banks aren’t really known to buy crypto. They’re not really known to buy silver. They’re really known to buy basically dollar reserve assets and now gold.

Where do you see this silver story playing out? Will silver or continue to be a monetary metal where people think, Yeah, this has some monetary qualities like gold?

Or will it trend more like an industrial metal where people think, Hey, this is the new copper, this is the new platinum, and this is the new titanium? Where do you see the silver story playing out?

Charlie Morris:

The correlations are a fascinating thing, aren’t they? And we’ve talked about Bitcoin and tech. Why the hell does Bitcoin move up and down with Microsoft and NVIDIA and stuff? I mean, why? I don’t know. But it does. It just does. And why does silver mean with gold?

I don’t know, but it has done all my life. And so I assume that will carry on. And I guess there’s some pairs trading in it. And I guess there’s commonality like jewelers and the vault people. They have things in common. So I guess there’s some natural reasons for that correlation. But it just happens.

And I think that if you think about the value of all the silver, what it’s collectively worth, it’s a much, much lower number than gold, and deservedly so, because it hasn’t got the bid and all that, the structural bid. And the problem with all the industrial applications are saying, oh, AI needs it, satellites need it, solar panels in space need silver. The trouble with those arguments is they’re never true at any price. They might be true at 50 bucks an ounce, but they’re not true at a million dollars an ounce.

You know what I mean? So therefore, silver is going to go to where the market will bear. And ultimately, the speculators will be the last ones holding the hot potato. And we just see it in… You never bet against human ingenuity in commodities.

And gold is the exception to that, because it’s not really consumed. And so therefore, alchemy is apparently possible, but expensive, cheaper to buy it all. So there’s those sorts of things. But substitution in industry is someone’s always going to come along and do something super clever. And that’s the issue.

But yeah, the world of correlations is a fascinating thing and happens very, very naturally. And sometimes you can put a finger on it and say, why? Sectors would move together, wouldn’t they? I mean, why not? But other times it’s pretty unclear.

So I think you got to think of gold as the money one. Silver is the the crazy catch up trade. I don’t know what the trough Half of the gold-silver ratio will be this cycle. I don’t know if we’ll outdo the past. We’ve already had it. I just don’t know. But it could be quite fun. But I think we’ve had the best bit.

We’ve had the best bit in silver. It was dirt cheap five years ago. It was free, and now it’s not. You’ve had a huge return in silver, and the last bit gets all the noise. But gold, I think that it They will port at some point. I mean, it’s done extremely well.

But even if the central banks keep accumulating, it could still pause. It gets hard to push up. What is gold now? $35 trillion or something? Is that the number they’re saying at the moment? How do you double that easily? You need lots and lots of money.

Monetary Metals:

I want to ask you about that central bank story, because central banks were such big purchasers in 2025, obviously big purchasers in 2026, if you look at the dollar amounts of gold as well. Is there a risk that central banks either sour on gold? They decide, Hey, we don’t need gold.

We’re going to elect a great Fed President. And all of a sudden, our fiscal situation is cleared up, interest rates are high, and all of a sudden, the case for gold goes away when it comes to central banks who have obviously been quite big buyers. What do you think the risk is when it comes to central bank gold purchases?

Charlie Morris:

There’s 100% chance that central banks will get a board of gold at some point. Now, is that now or is that in 20 years time? Who knows? But hopefully what they’ll do is they’ll buy loads of gold and they’ll just sit on it, and they won’t do what they did the last time and start selling it again because they’ll recognize it’ll make the world a more stable place if there’s more gold in more central banks.

But the thing that would put… If I was a central banker, the thing that would put me off if I was sitting in Qatar, or Indonesia, or China, or somewhere, and I was looking around the world, I look at the G7. We’re talking about the G7, aren’t we? We’re not talking about anyone else. And I’d be looking at these places and say, look at those people. They’re balancing the budgets.

They’ve got falling debt GDP ratios. It’s all looking pretty good now. Inflation is under control. They got Volcker at the Fed and similar people like that. They’re doing the right things for the money. You might not get elected doing that stuff, but the money likes that stuff.

And so if the money is good, if all the money looks like Swiss money, then Why do you need God? Yeah, but if all the money looks like Turkish money, then you need lots of God. So it’s very simple, really, when it comes down to it, and it comes back to printing and money supply, and balancing the whole equation. I do think that it comes down to how much money there is in the world, what all the assets are worth, and some big seesaw, and how they fit together, and all that thing.

And then, of course, the things that’s really hard, it’s really easy to say, Okay, Apple’s worth that, and Google’s worth that, and China’s reserves are worth that. That’s all quite easy to calculate. The harder bit is when you’ve got intangibles and credit systems that have gone out of control, and you don’t really know what they’re worth.

Monetary Metals:

What do you think about the regulatory regime, the fiscal regime inside the United States? Obviously, Trump is currently the He’s looking to elect a certain Fed position.

Whether he gets it or not will be interesting to see. But how important do you think the regulatory environment inside the US is for different assets like gold, crypto, even the rest of the world?

Because obviously, if there is a democratic win where the power balance becomes a bit more even, that might slow some of these Trump initiatives, whether it’s tariffs or trade wars. How important is the US to this story? Or are emerging markets actually more important, and the US over time will actually play less of an important story.

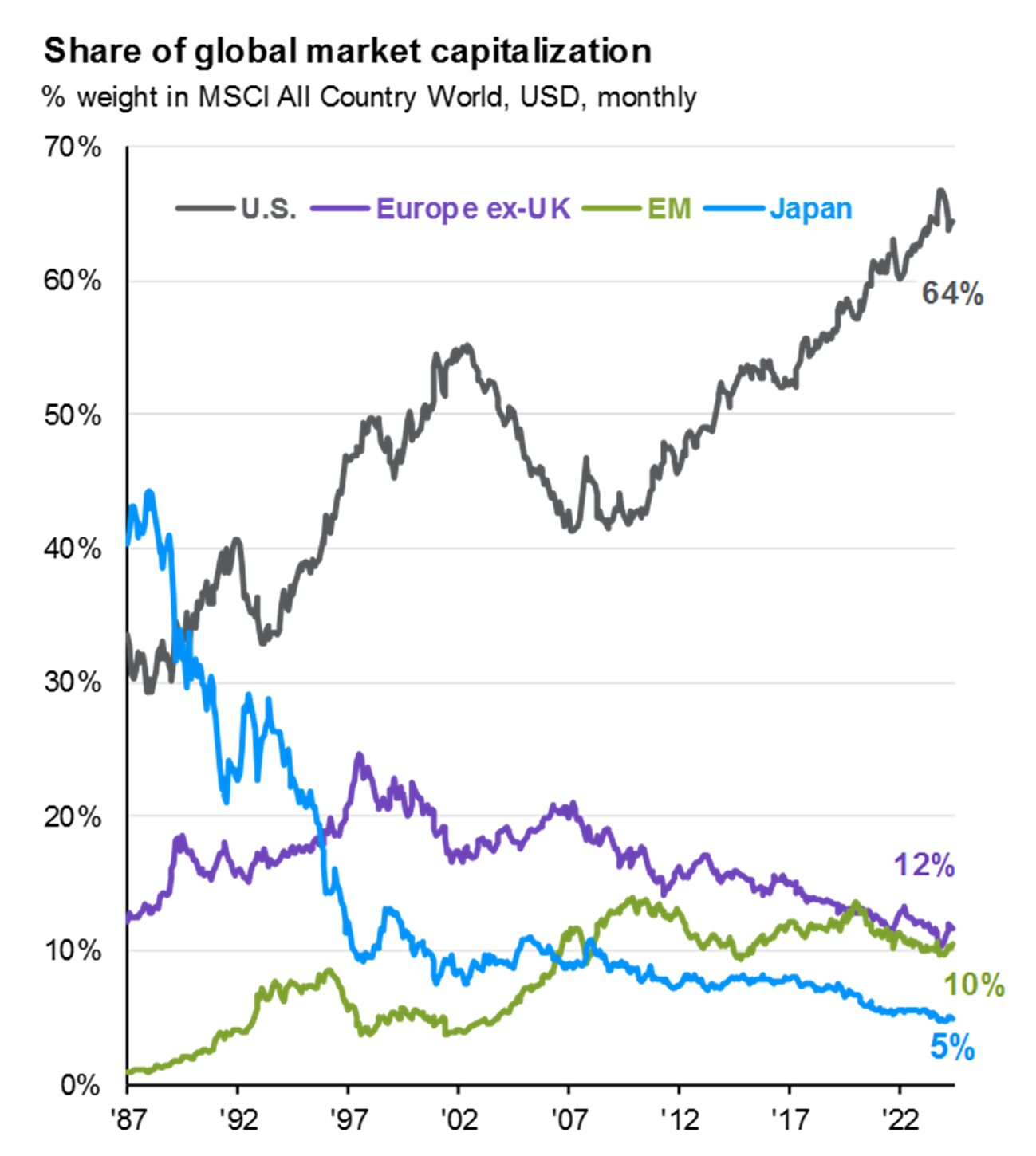

Charlie Morris:

I think the US has been the most important story, particularly in stock and bond markets, which basically are financial markets. But I think the balance will shift. It’s a cycle. We’ve talked about cycles earlier, didn’t we? The US equity market has been outperforming since 2009 until, what, about 14 months ago when it’s been lagging quite strongly.

And I think that big cycle has gone the other way now. I mean, it makes sense. You’ve got two-thirds of global market cap in the US, which is what is US GDP? I don’t know. Is it 20 % of the world or something? 70 % of the cap, 20 %. That’s just absurd. So the last time we had that situation was in the late ’90s. I think EM was 0. 2 %, 0. 2 of global market cap.

Asia was about the same, and the US was up there again. And there are a few other anomalies around the place, but those were the big one. In Japan, in 1990, was 50 % of global cap. So these things come around, and they always go back to where we should be. They’re never where they should be, but they always head back to some common sense thereafter.

And so I think there is going to be a big shift. And I think the US markets, whatever happens, whoever is in charge, will become less important just because of pricing. And I think that has started. I’m not suggesting that the rest of the world boom, and the US is going to the pan. I’m not saying that at all. It’s just the amount of market cap in the US is crazy high.

\And you can bet, and you do that on CAPE ratios or cash flows, however you measure it, it comes out there’s a rich market that it needs to adjust down. So the policy makers or US is the most important country in the world. I’m sure it always will be.

But we don’t even know who the President of Indonesia is anymore. We’ve forgotten. But I bet you, when everyone gets excited about emerging markets, we’ll all know. And we’ll all become experts on Timbuktu, because that’ll be the best stock of the year. It will be some Timbuktu.

Monetary Metals:

I All right, Charlie, I want to get to a fun lightning round section. So these will be rapid fire questions all around the map.

Of the BRICS countries, let’s say you had to short and long, which countries in the BRICS do you go short and which countries do you go long?

Charlie Morris:

I’d probably go short India, long Brazil. Brazil, I like the resources. It’s dirt cheap. India, I think, has been the tech bubble before the US tech bubble. It’s a very, very rich market.

I like the demographic story in India. It’s the best in the world, big and growing. We like that. GDP per capita is going up. All that’s great. But it’s been a very, very pricey market, and I’m a valuation guy at heart.

Monetary Metals:

Next question is about demographics for you, Charlie. Obviously, we’re seeing a low birth rate in many countries, often below the replacement rate.

How does this matter to assets like gold versus Bitcoin, where generally the boomer is the older generation like gold, maybe the younger generation a bit more into crypto. How much does this demographic story matter to these asset classes?

Charlie Morris:

Yeah, it’s a really good question. I don’t think I’m very strong on this, but I get the point. But what’s happening in Japan is really interesting, which has got probably the worst demographics of a rich country, I think. They’re more Korea. And more robots, please, right? I mean, you find a technological solution. But it will be odd. I mean, it’s hard to imagine a country like that.

I got Korean friends, and none of them are women having kids. Where will there be any Koreans? I mean, I don’t know. I don’t know how this plays out. Because they all want a career and no one wants a baby. And so it’s a big deal. It is a big deal.

But I’m sure the economy can adjust with more robots and AI and all that stuff. But what does it mean for gold? Well, the population is still growing, right? Globally.

Monetary Metals:

Yeah. Expected a peak in 2035, I think.

Charlie Morris:

Gold go up, Bitcoin go up.

Monetary Metals:

Okay, Charlie, next one for you. Let’s talk about interest rates in the United States before we get to interest rates around the world. Interest rates in the United States are mostly on the short term dictated by the Federal Reserve and the Fed funds rate.

Do you think that Trump and his cronies at the Fed, if you want to pit it not so nicely, are going to push interest rates down back towards zero?

Or do you think we’re going to have a hawkish Fed who says, Hey, we got to really clean up a mess here, and Trump put me in charge to do that, and we see higher rates for longer?

Where do you see interest rates in the United States going forward?

Charlie Morris:

Does President Trump know what he wants? Why does he pick the guy who wants to put them up if he wants them down? I mean, all I say about Trump is that he’s a property developer at heart.

A property people look at banks, they burst out laughing whenever they walk past a bank, and they go in, put a face on, and they go, Can I borrow a billion dollars, please?

And then they tend to care about the guy, and they get the money, and they just walk out thinking, I’m a bank robber, and they just gave me a billion dollars. And property people just want as much credit as they can possibly get. And they see that as the way the world goes round. And so I think that he believes in cheap money, I would think, being a property guy.

And I’m not sure that’s how the world works. From the Austrian school, a little bit. I’m not one thing. I try to have a broad range of views, but the Austrian in me would say that’s not necessarily true, that the lowest interest rate is the right way forward.

Monetary Metals:

Charlie, next one for you. I want to talk about the risk of inflation versus deflation. Obviously, in the past, we’ve talked about this affordability crisis. Inflation has been in the air in the United States and around the world, but we haven’t really discussed much about the risk of deflation. Which do you think is a bigger threat going forward? That we see inflationary regimes where prices continue to rise, CPI continues to rise, or a deflationary regime where something like an AI bubble pops, a stock market falls, which you think is the biggest risk going forward?

Charlie Morris:

Probably deflation because I think we’re all geared up for inflation. We’ve been talking about it for the last few years, and the bond market has had a big adjustment for it.

But let me tell you a little secret. The US 10-year treasury, the 200-day moving average is rising. You can’t ignore that. I’m not making a forecast here. I’m saying, look, everyone’s These bonds are shit.

They’re all going down, and they’re all awful. But the 200-day moving average is rising on not just the US 10 year, but on quite a few major benchmark bonds around the world. And not in Japan, obviously, give it time. But we haven’t seen Japanese inflation so despite the currency market. So it’s easy to be in the inflation camp and just talk about copper and stuff. But I mean, oil is only 70, and there’s a war threat. Not much, is it? Inflation-adjusted oil today is not far off the 2008 lows.

Monetary Metals:

Fascinating story on that front. Charlie, another rapid fire question for you. I want to ask you about Ethereum, which is in some ways the second largest cryptocurrency behind Bitcoin. We talked about silver, maybe being the second monetary metal to gold.

\Where’s Ethereum? Are people still interested in this as an asset class? Is it still a competitor to Bitcoin? Is it its own thing? Are people still interested in this story, or are most of the focus going to monetary assets, monetary competitors like Bitcoin, gold, and the US dollar?

Charlie Morris:

I think the gold-silver relationship, Bitcoin-Ethereum, is not dissimilar. I mean, Ethereum is the workhorse of digital, and it powers $310 billion of stablecoins. And for all the crypto bulls who believe we’re a really new financial system, then the future of stock markets and bond markets will be on crypto rails. It’s things like Ethereum that drive it. So it’s the powerhouse.

I think that Ethereum should certainly be in any tech portfolio. If you like tech and all that, you should own some Ethereum because it makes sense. I think Bitcoin is the alternative digital monetary asset. Ethereum is the digital workhorse.

I think it’s going to be very successful over the next 5, 10 I’m sure people who own it will make loads of money. The crypto coins. We do a bit of research on crypto and outside of Bitcoin, and we have a model portfolio and stuff. And we just been trying to look for real business models. That’s all we’ve been doing, plugging in our equity thinking into crypto. We’ve got half a dozen names that we own, and Ethereum is the most important one.

Monetary Metals:

Charlie, I want to ask you about some of these crypto companies that may or may not have a business. The last time you were on, we discussed digital asset treasury companies, of course, Michael Saylor and Strategy being the most famous, doing this financial alchemy where their pot of Bitcoin traded above the actual net asset value.

That trade has started to disintegrate in a lot of ways, and that financial alchemy may be over. Where do you see the digital asset treasury companies going forward? Was this a weird blip in the markets where people thought that this might be a fun trade and it’s now over? Or is there actually more to this digital asset treasury story than meets the eye?

Charlie Morris:

They’re regulated by arbitrage, okay? So there are lots of countries in the world where you can’t buy Bitcoin. Yeah, can’t buy a Bitcoin ETF. So the UK was on that list until last October. Uk, it’s supposed to be a free international whatever.

So we’ve lost the plot banning shit over here. And you could buy it in Germany and Sweden and a place like that. But how do you restrict it? So it’s not like anyone can easily buy it. It’s not as easy as you think to buy a Bitcoin ETF in the UK. And the wealth management industry never bought it.

And there are countries like Singapore, another financial center that doesn’t have Bitcoin ETS. Hong Kong does. Japan doesn’t. China doesn’t. India doesn’t. Yeah. Brazil does. Russia, who knows? Who cares? And so you’ve got these big places that won’t let you buy it.

But then they probably can’t really ban a stock. And so the Treasury Company is a regulatory arbitrage. And I think you’ll find, if you do the analysis carefully, you’ll find a lot of the buying is overseas. There’ll be some people who like Michael Saylor in America who buy that, but there’ll be a huge amount of overseas buying because it’s the only way they can get into Bitcoin.

And incidentally, the premium, the Michael strategy premium peaked in early October the last time, and that was when London listed ETFs for Bitcoin.

So you give more ETFs to the world, less need for these things. And all the magic tricks around the balance sheet, well, I mean, come on, please. It’s happening. You can’t just crank around by issuing bonds and convertibles and buybacks and issues and stuff and create alpha. It’s just not how it works.

Monetary Metals:

Couldn’t agree more. Charlie, last rapid fire question for you. When it comes to Bitcoin and gold, which do you see outperforming in 2026?

Charlie Morris:

Can you make it a bit easier?

Monetary Metals:

I ask the tough questions here on the Gold Exchange podcast, Charlie.

Charlie Morris:

If you give me two years, then I can say Bitcoin.

Monetary Metals:

Yeah, why don’t you give us a one year, a two year, and maybe a five year?

Charlie Morris:

Okay. Gold, Bitcoin, Bitcoin.

Monetary Metals:

Maybe it may be a bit easy for you. All right, Charlie, I want to ask you a question here.

Charlie Morris:

That’s exactly it. I’m going to change that. I’m going to go Bitcoin, Bitcoin, Bitcoin.

Monetary Metals:

I like it. A little bit contrarian on this episode here.

Charlie Morris:

Charlie, what’s- Bitcoin is a prize. It doesn’t have to do very much at all as a surprise. You’ve seen a tiny bit of stability in the tech sector, and it could fly deeply oversold. And goal’s like, it’s done so much. I love them both. Gold has done so much.

I’ve been defending gold most of my life against Bitcoin. It’s now Bitcoin has come crying, saying, Why can’t we be more like gold? It’s like, just embrace both.

Monetary Metals:

Charlie, I want to ask you for our viewers, what do you think is the biggest risk to both gold and Bitcoin so when they’re looking out at the macro environment, they can think more about how to tactically allocate into gold and into Bitcoin?

Charlie Morris:

The biggest risk to any of them, well, as I said, it’s all the government Governments turning Swiss and having sound money and balanced budgets. If all the government ran their affairs well, then Bitcoin and gold, I think, it would be less to talk about. People wouldn’t say, well, give me some scarce assets, liquid scarce assets. This isn’t baseball cards, right?

Which are not liquid or fine wines or art. This is highly liquid alternative assets. And there’s something very special that. So I think the world becoming remarkably normal is the biggest risk to owning them or just bubbles.

Gold might be a bubble, probably isn’t, but I don’t think it is, but it could be overdone. But bubbles are always a problem. You have to wait a few years before that draws out. But I think that people should just strongly consider, if you’re not Bitcoin gold people, just go and do something else. Go and stick with NVIDIA. Good luck.

But if you if you do like gold, consider Bitcoin. If you do like Bitcoin, consider gold, and think about pairing them. We publish the data for free on our website.

Monetary Metals:

What’s something you think the Bitcoin people can learn from the gold people and vice versa? What’s something the gold people could be learning right now from the Bitcoin people?

Charlie Morris:

Well, the Bitcoin people need to learn that they stole gold narrative, but then did fail to tell Bitcoin, if that makes sense. So you’ve been I’ve been watching for years, these Bitcoin people going on about the end of the world and all the arguments, debatement and stuff.

And then Bitcoin does something completely different. And I’ve been trying to build frameworks around it. And basically, Bitcoin does an overheating economy. It loves it when rates are going up and gross good and employment is strong. It just loves all that. Strong ISM, these sorts of things.

Whereas gold genuinely is the Ice Age trade. I mean, things are going wrong. We’re all starving and nothing works, and gold goes up. So there is a sense of that. Now, Bitcoin has never got that non-correlation, that negative correlation to risk. And I don’t think it will for a very long time, if ever. It doesn’t need to be interesting, because the world’s not always going to shit. Sometimes it’s going quite well, and sometimes it’s not. So we will BOLD photos should reflect that. Have a bit of risk on, a bit of risk off. But I think that to pair them is a strong concept.

Monetary Metals:

Charlie, where can people find more you and more BOLD?

Charlie Morris:

Bold. Bold, if you want data on BOLD, if you’re interested in gold ETF flows, Bitcoin stuff, ETF flows, and our weights and all that, we publish it on boldetf. Com. B-o-l-d-e-t-f. Com.

Go there, all free. Help yourself. Then if you want to hear about our clever TradFi research, which is truly amazing, global deep value stocks and stuff, then that’s bike tree. Com.

Monetary Metals:

Charlie, final question for you. What’s a question I should be asking all future guests of the Gold Exchange podcast.

Charlie Morris:

Do you have a six-month-old puppy like I do?

Monetary Metals:

Tell us about your puppy, Charlie. That’s a great way to end our conversation.

Charlie Morris:

There you go, Ben. Let’s get her in the light. The light’s not very good here. So there you go. If they do have a six-month-old puppy, then they win. They win an ounce of bold. They win an ounce of bold.

Monetary Metals:

Make sure to contact Charlie for your ounce of bold and the cute puppy.