Gold Miners: WRLG and Other Special Situations

Authored by GoldFix

Why WRLG and its peers are interesting comes down to three simple factors: asset quality, timing, and leverage to gold.

Here are some key aspects that attracted us to them as a special situation play and served as a template for the others in the list. That is followed by a simple table giving our starting points on where the others are similar and where they differ.. at first glance. This is all a starting point for our own work and can be a guide in your own research if you choose to use it. Financials have yet to be parsed for most of these companies

Pictures are AI and (such as they are) serve our purpose.

Contents

- Historic High-Grade Mine Restart

- Production Inflection Point

- Strong Gold Price Leverage

- District Expansion Potential

- Scarcity of Restart Stories

- Main Risk- Single Factor Focus

- Peer List: Similarities and Differences at first glance

- ***Full disclosures.

1. Historic High-Grade Mine Restart

KEY INGREDIENTS

1️. Mine restart stories

Old infrastructure + new gold price environment.

2️. High-grade districts

Red Lake historically produced 30M+ oz of gold.

3️. Production ramp optionality

Madsen (WRLG) alone could scale from roughly 45k oz/year initially to much higher levels with Rowan satellite deposits.

That combination often drives 5-10× equity rerates in gold bull cycles.

WRLG controls the Madsen Mine in the Red Lake district of Ontario, one of the richest gold camps in the world. The mine historically produced over two million ounces of gold at very high grades. The infrastructure already exists, which dramatically lowers the cost and timeline to restart production.

2. Production Inflection Point

The company is transitioning from developer to producer. In mining markets this phase often drives the largest valuation change because the business moves from a concept to a cash-flowing operation.

3. Strong Gold Price Leverage

Because Madsen is high-grade underground ore, the economics improve quickly as gold prices rise. A $200–$500 move in gold can materially change margins and investor perception.

4. District Expansion Potential

WRLG controls additional deposits around Madsen (such as Rowan). If these satellite deposits are developed, the operation could evolve from a single-mine restart into a multi-deposit district platform.

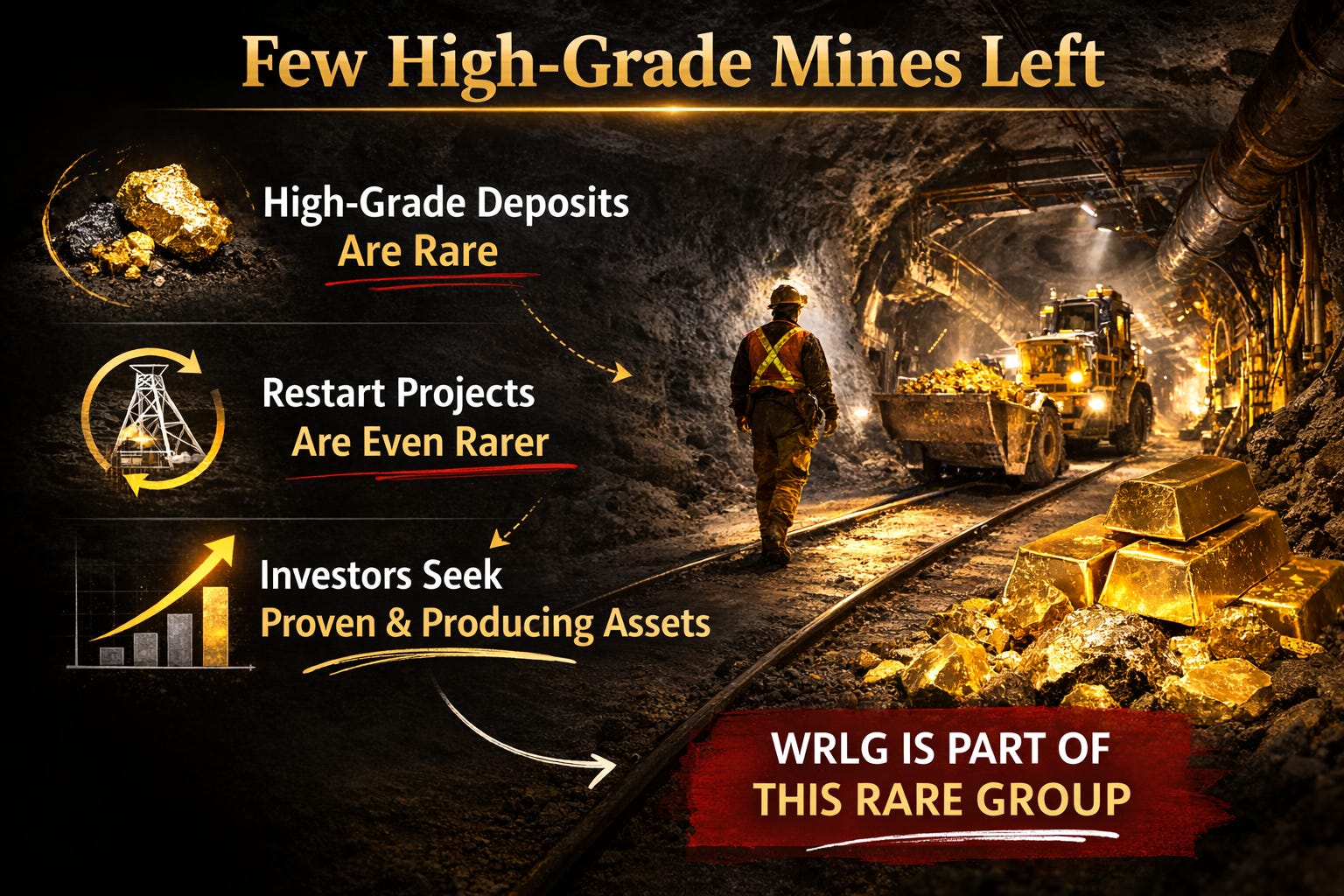

5. Scarcity of Restart Stories

There are relatively few high-grade mines in safe jurisdictions that can be restarted quickly. That makes WRLG part of a small group of junior miners with meaningful torque to the gold cycle. This also makes WRLG and others like it attractive targets if a major ramps up…

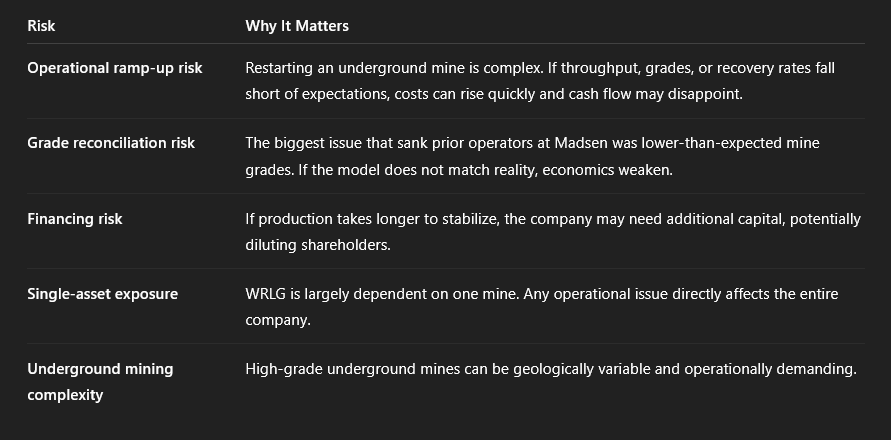

6. Main Risks- Single Factor Focus

The WRLG thesis works if Madsen produces consistent high-grade gold at scale. If the ramp-up succeeds, the company can re-rate quickly. If it struggles operationally, the market tends to punish restart stories severely.

***Full disclosure. GoldFix has no financial relationships with any of these miners. This is purely for idea generation using fundamental analysis in what is perceived to be special situation investing.***