A Breakdown of the World Gold Council’s Bearish Dollar Thesis

Authored by GoldFix for Scottsdale

The World Gold Council’s latest market commentary examines the relationship between U.S. dollar cycles and gold performance. The report argues that while the dollar recently avoided a technical breakdown, structural forces shaping global capital flows may ultimately push the currency into a renewed downtrend. In that environment, gold remains positioned as a primary beneficiary.

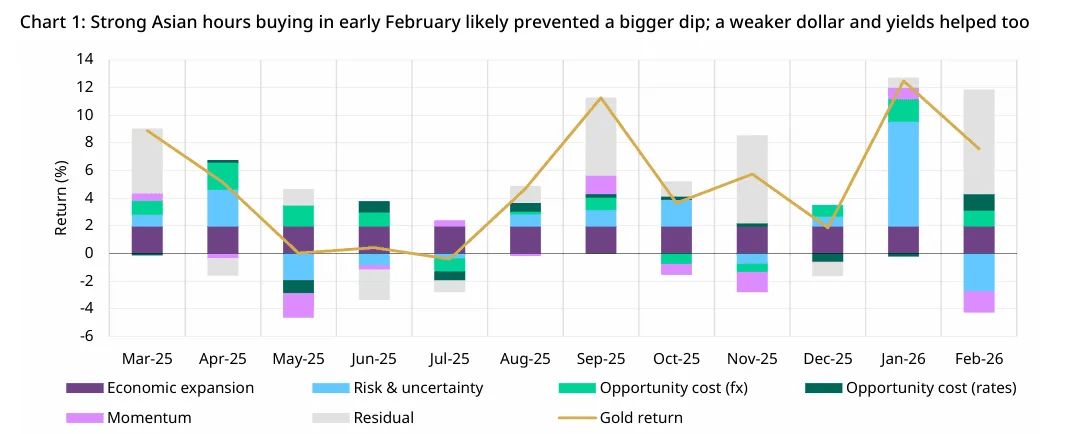

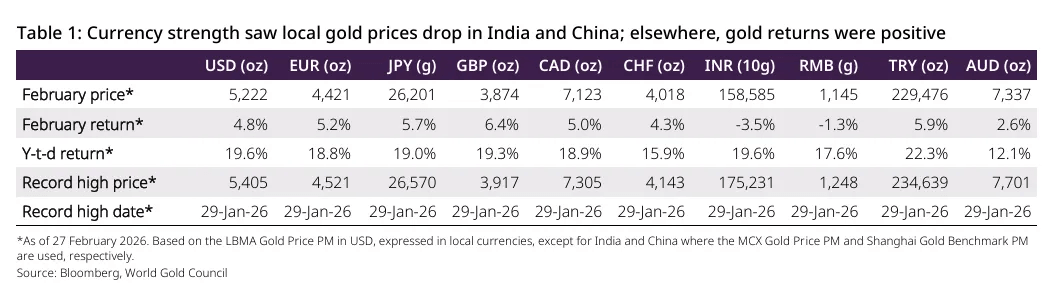

February’s market behavior provides the immediate backdrop. Gold rose roughly five percent during the month and nearly twenty percent year to date, reaching approximately $5,222 per ounce. The advance occurred despite declining speculative positioning and falling implied volatility, developments that might normally weaken momentum-driven assets. Instead, the market found consistent support from physical buying and macro tailwinds.

The report attributes February’s gains primarily to a weaker U.S. dollar and lower U.S. Treasury yields, both of which reduce the opportunity cost of holding gold and increase its attractiveness to global investors.

“Gold gained another 5% in February… contributions to the positive return came from a weaker US dollar… and a lower 10-year US Treasury yield.”

February’s Gold Rally and the Residual Demand Signal

Yet the World Gold Council’s Gold Return Attribution Model did not fully explain the magnitude of the move. The analysis identified a sizable residual component beyond the influence of traditional macro variables, suggesting an additional source of demand.

The chart illustrates how dollar weakness and falling yields contributed to February’s rally, while a large unexplained residual remained. The report argues that this component likely reflects strong Asian physical demand, evidenced by price resilience during Asian trading hours and elevated volumes on the Shanghai Futures Exchange. In effect, physical buying appears to have offset the decline in volatility and reduced speculative positioning that might otherwise have pulled prices lower.

ETF flows reinforced this geographic divergence in sentiment. Gold ETFs added approximately $5.3 billion during February, led by inflows from North America and Asia. Europe recorded moderate outflows as investors took profits following the sharp price advance in January. Meanwhile, managed-money net long positions on COMEX contracted early in the month before stabilizing toward the end of the period.

The Dollar’s Temporary Stabilization

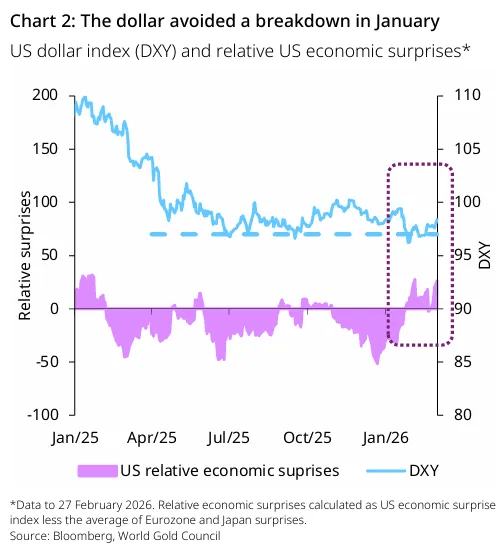

The report’s central thesis concerns the trajectory of the U.S. dollar. According to the World Gold Council, the dollar avoided a technical breakdown earlier in the year due to temporary macro support rather than structural strength. Positive economic surprises in the United States and supportive futures positioning helped stabilize the currency index, allowing the dollar to rebound briefly.

“The downward trend in the US dollar index is likely to resume… and is a key positive force for gold prices going forward.”

The chart shows how stronger U.S. economic data temporarily supported the dollar and prevented a breakdown in early 2026. However, the report suggests that this support may prove short-lived once broader valuation and capital-flow dynamics reassert themselves.

Relative Valuation Pressures on the Dollar

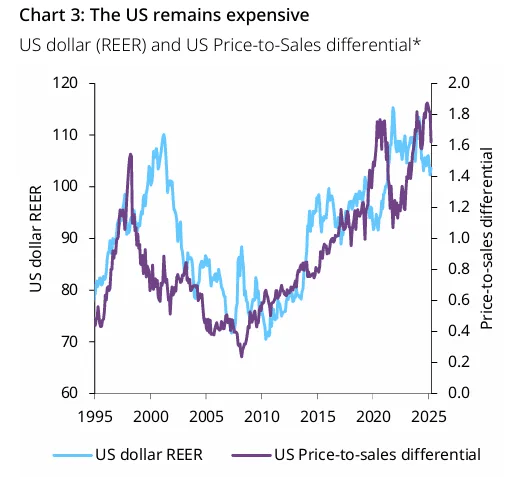

One of the key arguments presented in the report concerns relative valuation across global markets. By several measures, U.S. assets remain expensive compared with their international counterparts. The report highlights both the real effective exchange rate of the dollar and the valuation of U.S. equities relative to Europe and Japan as evidence of this imbalance.

These valuation differences create conditions in which international investors may increasingly consider reallocating capital away from U.S. assets. If such flows accelerate, they could place downward pressure on the dollar and reinforce the macro environment that typically supports gold.

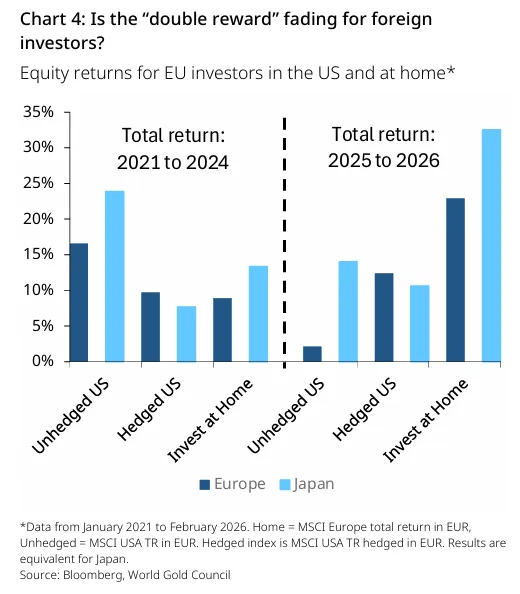

The Fading “Double Reward” for Foreign Investors

For much of the past decade, foreign investors benefited from the combination of rising U.S. equity markets and a strengthening dollar. That dynamic amplified returns for international capital invested in U.S. assets. The report suggests this “double reward” may now be fading.

The chart illustrates the evolving decision facing global investors. Investors can continue holding U.S. equities while hedging currency exposure, which reduces total returns, or rotate capital toward markets offering more attractive valuations. Europe and Japan increasingly appear as viable alternatives, supported by fiscal capacity in Germany, corporate reform momentum in Japan, and growing concerns about concentration risk within U.S. equity markets.

If international capital begins shifting toward these regions, currency flows could amplify the dollar’s downward trajectory. Because European and Japanese equity markets remain smaller than the United States, even modest reallocations could move prices meaningfully and reinforce the trend.

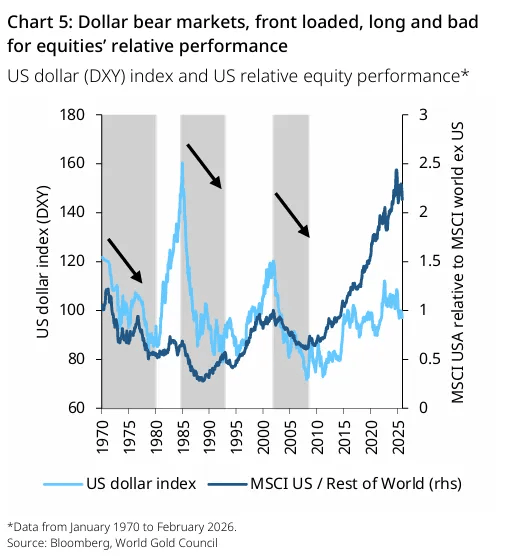

Lessons from Previous Dollar Bear Markets

Historical precedent also informs the report’s analysis. Previous dollar bear markets have exhibited two recurring characteristics. Currency declines were often front-loaded, meaning the sharpest moves occurred early in the cycle. These periods also coincided with relative underperformance in U.S. equities.

This relationship reflects a feedback loop in global capital flows. When investors begin reallocating capital away from U.S. assets, currency depreciation can reinforce those outflows by reducing the attractiveness of dollar-denominated investments.

At present, these rotations appear concentrated primarily in equities rather than fixed income markets. U.S. Treasuries continue attracting inflows due to favorable interest-rate differentials. However, if equity flows increasingly dictate global capital movements, the dollar may face sustained pressure over time.

Geopolitical Catalysts and Gold’s Reaction Function

The report also considers geopolitical developments that emerged at the end of February. Escalation in the Middle East produced an immediate reaction across global markets. Oil prices rose, the dollar strengthened temporarily, and Treasury yields declined as investors sought safety. Gold also reacted quickly, gaining nearly five percent across two trading sessions.

Historically, gold has responded positively to spikes in geopolitical tension roughly two-thirds of the time. However, the report cautions that the medium-term response is less predictable. In the two weeks following major geopolitical events, gold returns have historically ranged from gains of roughly eight percent to declines of around three percent.

The implication is that geopolitical shocks may catalyze immediate safe-haven demand, but longer-term price direction remains tied to macroeconomic forces.

Continues here