Oil: The Ultimate Weapon of Mass Disruption

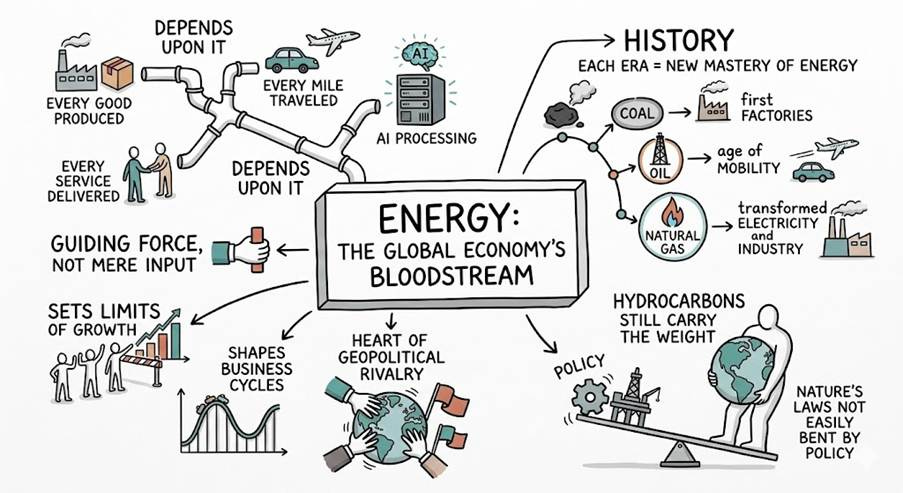

Energy is the bloodstream of the global economy. Every good produced, every service delivered, every mile travelled, and every data center processing artificial intelligence ultimately DEPENDS UPON IT. Yet modern macroeconomic discourse often treats energy as a mere input rather than a guiding force. History teaches otherwise: energy is not simply a cost, but a constraint. It sets the limits of growth, shapes the rhythm of the business cycle, and increasingly stands at the heart of geopolitical rivalry.

From the Industrial Revolution to the digital age, each era of prosperity has followed a new mastery of energy. Coal powered the first factories, oil unleashed the age of mobility, and natural gas transformed electricity and industry. Though many speak of transition, hydrocarbons still carry the weight of the global economy, reminding us that nature’s laws are not easily bent by policy.

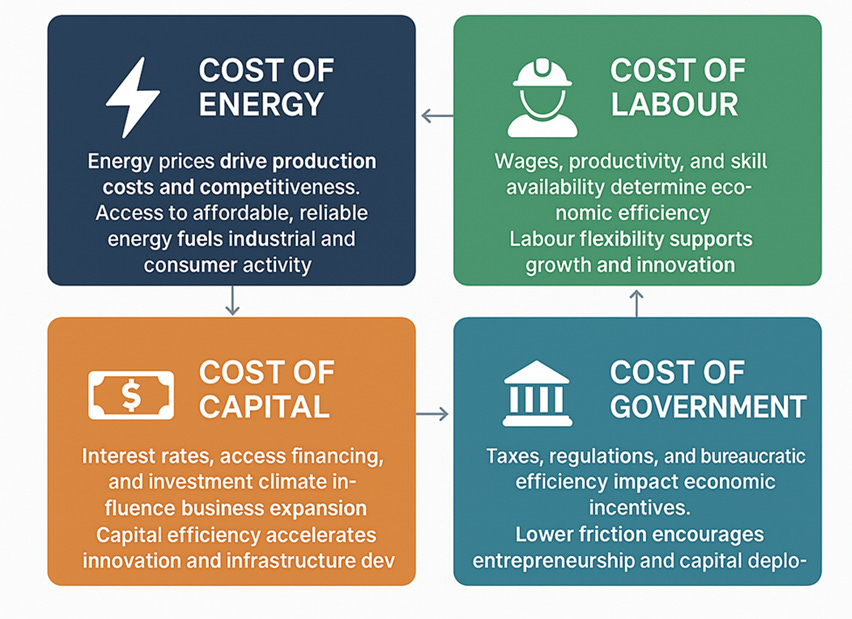

To understand energy is therefore to understand the economy itself. The cost of energy governs the fortunes of industry, the purchasing power of households, the path of inflation, and the balance between producers and consumers. When energy is abundant and inexpensive, growth finds fertile ground. When it becomes scarce and dear, economies slow and recessions appear. Such is the quiet law by which the modern world moves.

This truth lies quietly at the heart of the business cycle. For decades, the link between energy prices and economic growth has been evident, as many post-war recessions in advanced economies were preceded by sharp increases in oil prices. When energy becomes expensive, it acts like a tax upon the entire economy: transport costs rise, industrial margins compress, agricultural inputs become dearer, and households must devote a larger share of their income to fuel and electricity. The oil shocks of the 1970s offered a clear lesson, as the sharp rise in Middle Eastern oil prices plunged Western economies into stagflation—slow growth accompanied by rising inflation—leaving central banks struggling with a shock born not from excess money but from constrained energy supply. Similar patterns emerged before the 2008 financial crisis and again after the pandemic, when surging energy prices helped ignite a wave of inflation that forced aggressive monetary tightening. Thus, energy quietly governs the rhythm of expansion and contraction: when it is abundant and affordable, economies grow with ease; when it becomes scarce and costly, activity slows. In this sense, the price of energy sets the true speed limit of the global economy.

S&P 500 to Oil Ratio (blue line); 7-Year Moving Average of S&P 500 to Oil Ratio (red line).

Oil is the most geopolitical of all commodities. Unlike many industrial inputs, its supply rests in a few regions where political stability is often uncertain. Much of the world’s reserves lie in the Middle East, particularly around the Persian Gulf, where history has long been shaped by rivalry, conflict, and fragile alliances. Thus, the price of oil carries not only the balance of supply and demand, but also a premium for uncertainty. The global supply chain itself passes through narrow gateways—most notably the Strait of Hormuz, through which nearly a fifth of the world’s oil flows—while pipelines across Eastern Europe and Central Asia have become tools of political influence. The disputes surrounding Russian energy exports to Europe have shown how quickly infrastructure may become an instrument of power. Oil, therefore, is not merely a commodity traded in markets; it is a strategic asset woven into national security, diplomacy, and the shifting balance of nations.

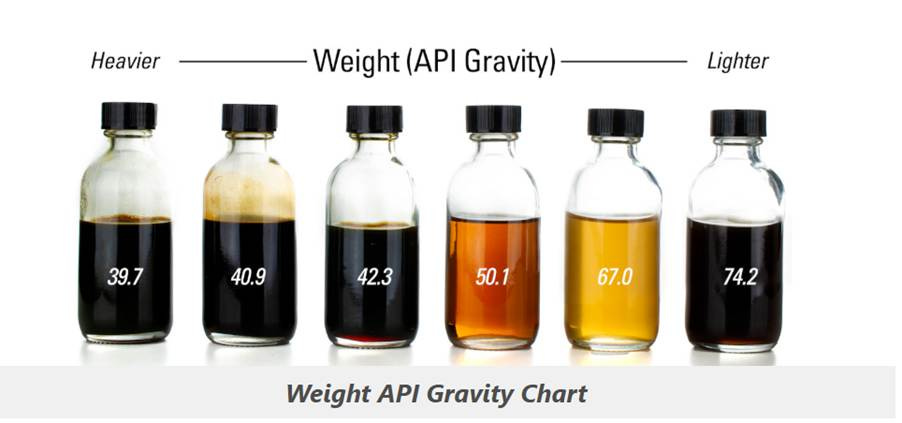

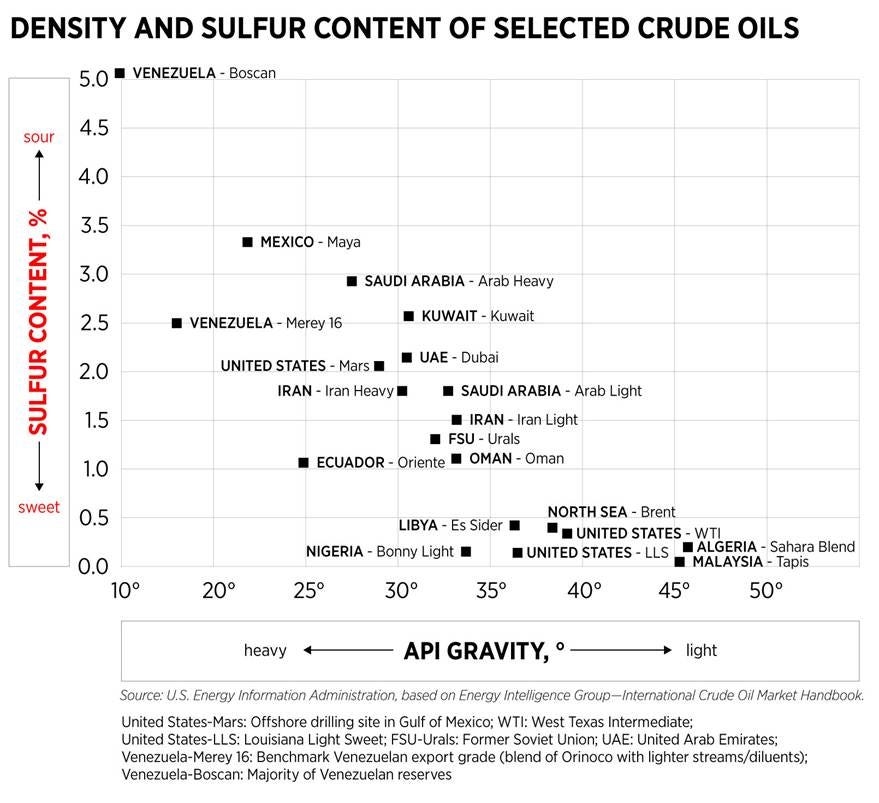

Crude oil, much like wine or coffee, comes in different varieties—though far less pleasant to taste. It is commonly classified by density (light or heavy) and sulphur content (sweet or sour). Light sweet crude is the refinery equivalent of an easy recipe: simple to process and quick to turn into gasoline and diesel. Heavy sour crude, by contrast, is more like a complicated stew that requires extra cooking, expensive equipment, and a fair amount of patience to remove sulphur and break down the thicker molecules.

https://kimray.com/training/types-crude-oil-heavy-vs-light-sweet-vs-sour-and-tan-count

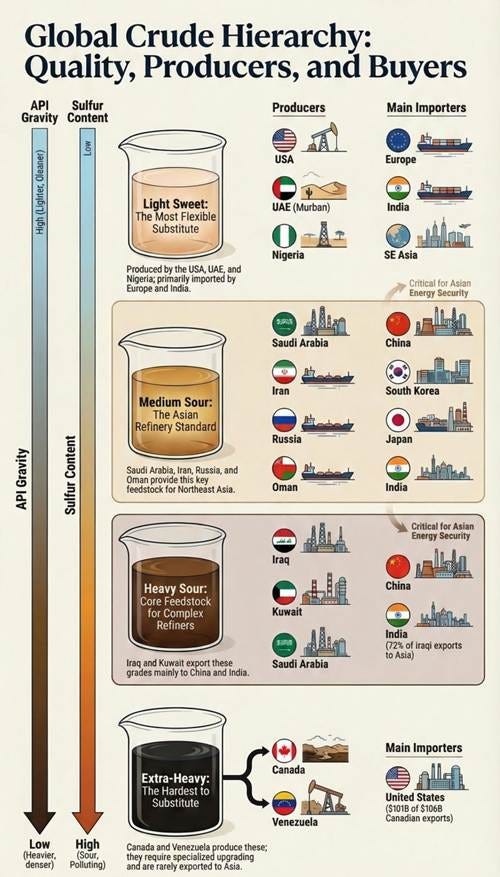

Over time, refineries around the world have become accustomed to particular “flavours” of crude depending on what their nearby producers supplied. Many refineries on the U.S. Gulf Coast and in Asia were built as industrial heavy-duty kitchens capable of handling the thickest and sourest barrels from the Middle East, Venezuela, or Canada. Meanwhile, several European refineries grew up refining the lighter crudes of the North Sea and Africa. The result is that the global oil market is not a simple buffet where any barrel can go anywhere. Each refinery has its preferred menu, which means that when a particular type of crude disappears from the market, the entire system starts behaving like a restaurant that suddenly ran out of the ingredients needed for its signature dish.

Asia’s refineries are engineered specifically for the heavy, sour crude grades that flow through the Strait of Hormuz — and that is precisely what is disappearing. The substitution problem is not a question of price but of chemistry: US Light Sweet crude does not run the same way through refinery configurations optimised for Gulf barrels, and there is no available alternative at scale. Russia is already maxed out with no capacity to increase exports meaningfully, and US Light Sweet is the wrong grade for the majority of Asian refining infrastructure. When the world’s most critical oil chokepoint closes because of insurers playing the role of the American Imperialistic agenda, it does not simply create a price shock — it creates a structural supply mismatch that no SPR release can resolve.

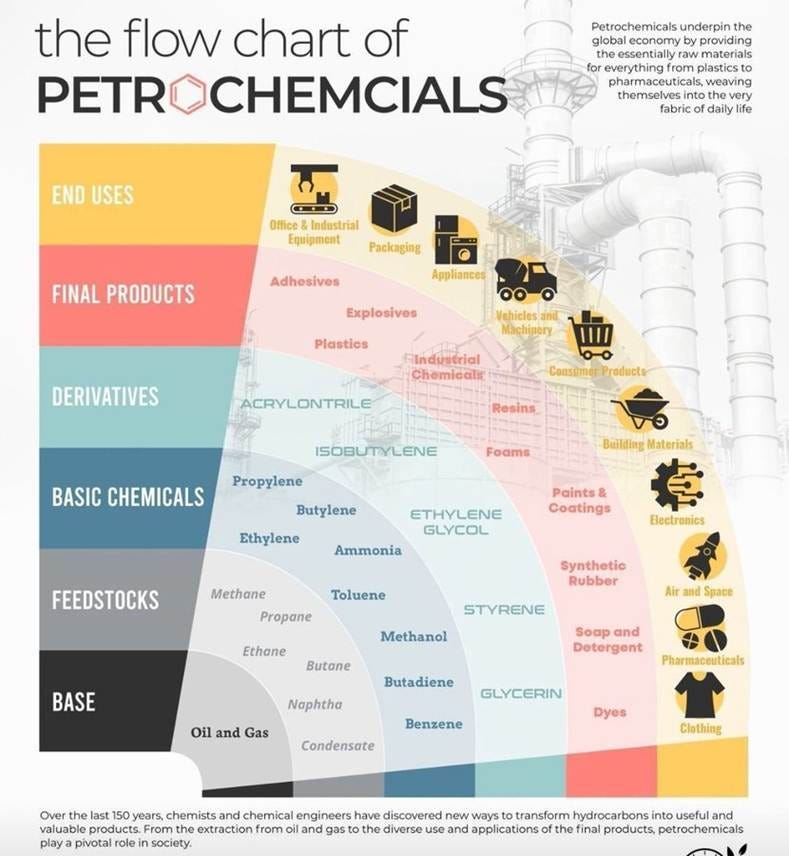

Oil is often praised for fuelling cars and airplanes, yet this is only its most visible talent. In truth, oil behaves like a quiet master in the workshop of civilization. When crude oil enters a refinery, it is patiently separated into different streams—gasoline, diesel, jet fuel, and naphtha. The fuels move the world, but naphtha travels to the petrochemical plants, where modern alchemists gently persuade it to become simple molecules such as ethylene, propylene, butadiene, benzene, toluene, and xylene. These modest-sounding substances are the humble scholars of the chemical world, from which thousands of useful materials are born. From ethylene comes polyethylene, the plastic found in packaging, pipes, insulation, and the many containers that guard our food and beverages. Propylene becomes polypropylene, which quietly serves in car parts, medical devices, carpets, and kitchenware. Butadiene lends its strength to synthetic rubber, allowing tires, shoes, and industrial belts to endure long journeys. Meanwhile, benzene, toluene, and xylene help create polyester fibres for clothing, as well as resins, paints, adhesives, and coatings that hold together the modern built environment.

Thus, oil does not merely power our engines; it shapes the very objects of daily life. The phone in one’s pocket, the fibres in one’s clothing, the packaging around one’s lunch, and even the fertilizer that nourishes tomorrow’s harvest all trace a quiet lineage back to the same barrel of crude. One might say that while men debate energy in loud voices, oil simply continues its work—turning itself into ten thousand useful things, without asking for applause.

The list of petrochemical companies declaring force majeure is now longer than the queue for a new iPhone launch—which is ironic, since those iPhones won’t be manufactured much longer without feedstock. Asian steam crackers, which brilliantly decided to source 60% of their naphtha from the world’s most stable region (the Middle East), are now scrambling to cut production, shut units, and explain to customers why chemical deliveries won’t be happening. From Malaysia to Vietnam, refineries are shutting down faster than you can say “global supply chain,” with companies rationing feedstock like it’s the apocalypse and praying they can avoid full shutdowns (restarting takes two weeks, and apparently nobody thought to keep more than a month’s supply on hand).

The punchline? All those consumer products on store shelves—literally everything involved in modern consumption—are made from petrochemicals, so get ready for shortages that’ll take months to resolve even if peace magically breaks out tomorrow. Inflation’s about to boomerang back hard when consumers discover that their entire lifestyle is basically refined crude oil with marketing. Who knew centralizing critical global infrastructure in an active war zone could have consequences?

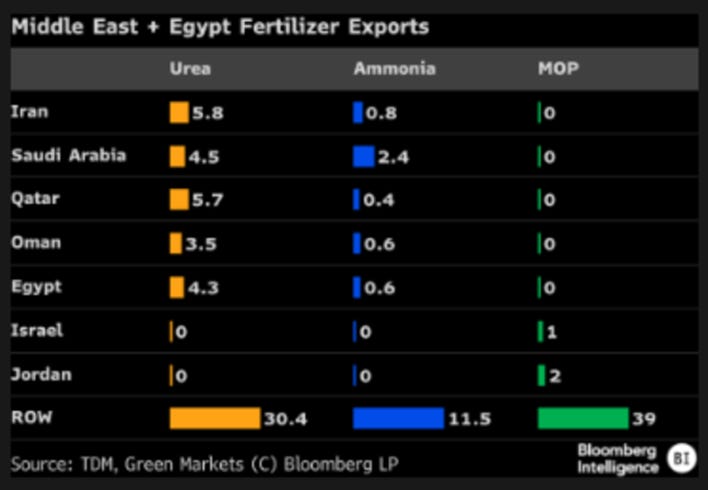

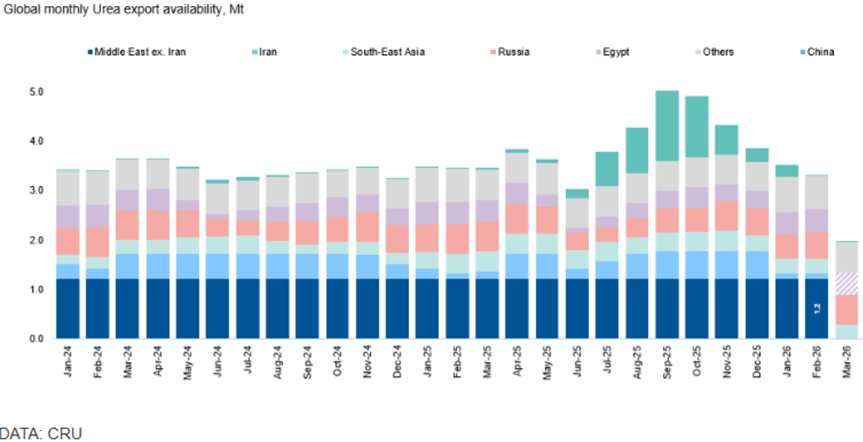

Turns out also the world’s fertilizer supply—the stuff that literally grows your food—flows through the same geopolitical powder keg where everyone’s currently having disagreements with missiles. Nitrogen production is heavily concentrated around the Persian Gulf, with Iran alone controlling 5% of global urea and 11% of ammonia trade through seven urea and 13 ammonia facilities (all conveniently US-sanctioned, so they sell slightly below market to India, Turkey, and Brazil—capitalism finds a way). Nearly half of global urea exports sail through the Strait of Hormuz, because apparently humanity decided the best place to produce fertilizer is right next to where we keep having wars about oil. Prices typically jump in Q2 when US farmers start buying and China decides to hoard theirs, but this year we’ve got the bonus wildcard of potential supply disruptions. Nothing says “stable investment” quite like fertilizer companies mining the Dead Sea while missiles fly overhead.

As of March 11th, 2026, global urea export availability has already plunged — and even should Operation Epic Fury cease tomorrow, the damage to agricultural supply chains is not a future risk but a present reality, unfolding with the quiet inevitability of a harvest that was never planted. Urea, that most essential of fertilisers upon which modern food production depends, joins an already lengthening list of commodities moving from abundance to scarcity on the world’s shelves — and food supply chains operate on agricultural cycles that no central banker can accelerate, no sanctions waiver can replace, and no Truth Social post can harvest. As the Master might conclude: “The army that wins the battle but empties the granary has not secured victory — it has scheduled the next crisis.”

Natural gas has become a quiet but essential pillar of the modern energy system. It powers electricity grids, heats industries, and provides the feedstock for fertilizers that sustain global agriculture. Unlike oil, gas has long depended on pipelines, which bind producers and consumers together in relationships that often-last decades. Such ties bring stability in times of peace but reveal vulnerability in times of tension, as Europe discovered ...

Read more and discover how to trade it here: https://themacrobutler.substack.com/p/oil-the-ultimate-weapon-of-mass-d…

Visit The Macro Butler Website here: https://themacrobutler.com/

Join The Macro Butler on Telegram here : https://t.me/TheMacroButlerSubstack

You can contact The Macro Butler at info@themacrobutler.com

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence