State Gold Returns: Wyoming’s Vault Strategy

Authored by GoldFix for Scottsdale Mint

A quiet policy shift is unfolding across parts of the United States. Rather than relying exclusively on traditional financial instruments, several states are beginning to hold physical precious metals inside their public investment portfolios. The move is small in scale relative to national markets, yet it reflects a growing debate about monetary risk, sovereign debt and the long-term role of gold in financial systems.

A recent article in The Wall Street Journal by Jared Mitovich documents one of the clearest examples of this trend. Wyoming has begun purchasing and storing gold as part of its state investment strategy, becoming one of several states experimenting with precious metals allocations as a hedge against economic instability.

The state’s first purchase was modest in institutional terms but symbolically significant.

Wyoming acquired roughly 2,312 troy ounces of gold, valued near $10 million at the time of purchase, now estimated around $11.6 million as prices have risen. The bars are stored in a vault operated by the private firm Wyoming Reserve in Casper.

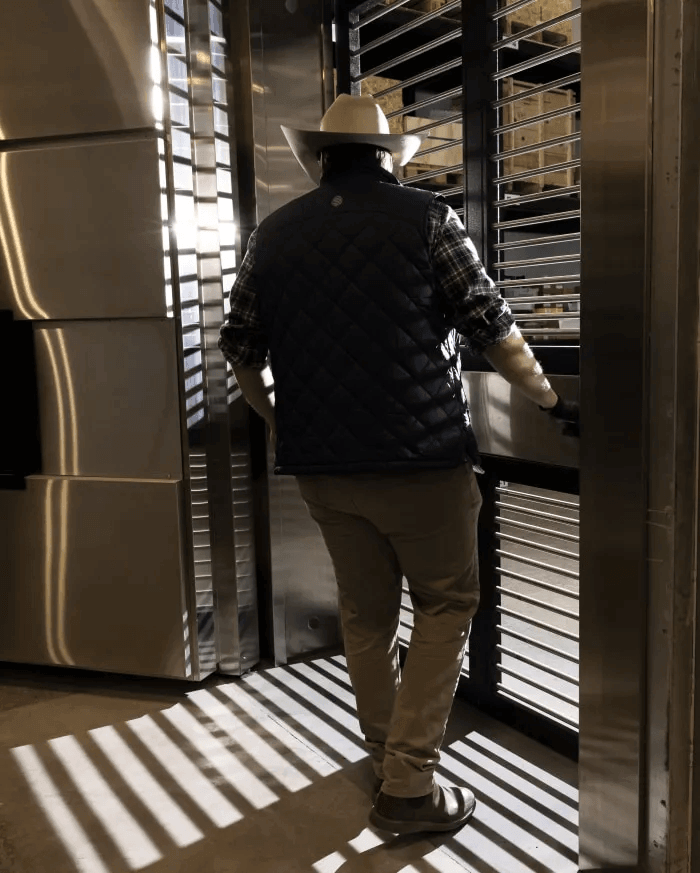

The facility itself reflects the seriousness with which the state approached custody.

According to Wyoming Reserve CEO Josh Phair, the vault structure is layered and heavily fortified.

“The vault is structured like an onion layer,” Phair said, describing a facility anchored to bedrock and designed for secure storage.

The gold purchase was mandated by the Wyoming Gold Act, legislation passed with strong support in the state legislature. The law requires Wyoming’s investment portfolio to include precious metals as a hedge against potential economic shocks.

Supporters of the policy frame it in explicitly macroeconomic terms. Senator Bob Ide, the bill’s lead sponsor, tied the legislation to concerns about federal fiscal stability.

“I can’t put a timeline on it, but there’s gonna be a sovereign-debt crisis,” Ide said. “There’s no will to rein in spending.”

Ide’s view reflects a broader anxiety among some policymakers that rising federal debt and monetary expansion could eventually weaken confidence in the U.S. financial system. In that context, gold functions less as a trading asset and more as a long-term monpetary hedge.

Ide described the metal in blunt monetary language.

“Gold is the lie detector; it’s the BS meter,” he said. “It’s the only real money that can’t be debased.”

The decision has not been universally supported inside Wyoming’s government. Governor Mark Gordon allowed the bill to become law without signing it, warning that mandating gold purchases could interfere with traditional portfolio management practices.

In a letter outlining his objections, Gordon argued that gold lacks the characteristics of a productive investment.

“Gold is not an investment as much as it is a commodity or store of value,” he wrote. “The only income to be derived from gold is to sell it for a greater price than it was purchased.”

Critics also point to gold’s price volatility. The most active gold futures contract reached $5,354 per ounce earlier this year before falling sharply, highlighting the metal’s capacity for rapid price swings even during strong bull markets.

Despite those objections, Wyoming’s treasury officials remain supportive of the strategy.

State Treasurer Curt Meier described the purchase as a modest but prudent diversification within the state’s $12 billion Permanent Wyoming Minerals Trust Fund, which was created in 1975 to invest revenue from natural resource extraction.

In his view, the current allocation represents only a starting point.

“The amount that we’ve purchased so far is de minimis,” said state Rep. John Bear, a member of the legislature’s investment committee. “But we needed to have some.”

Wyoming’s move is part of a broader pattern emerging among resource-heavy states. Utah led the modern wave in 2011, reaffirming gold and silver as legal tender. More recently, Utah authorized the purchase of up to $140 million in precious metals, stored in a Brink’s vault in Salt Lake City.

Other states are now considering similar legislation.

Lawmakers in West Virginia, Tennessee and Georgia have introduced bills that would allow state investment funds to hold gold and silver. Tennessee has already taken steps toward creating a dedicated precious-metals fund.

Utah may push further still. Representative Ken Ivory has proposed allowing mining companies to pay certain taxes directly in gold, a policy he argues would expand access to sound money protections for citizens.

“I can’t bear the thought of passing this off to my grandchildren without doing everything I can to try to fix it,” Ivory said, referring to federal debt levels.

Economists remain divided on whether these policies reflect prudent diversification or misplaced anxiety.

Steve Hanke, an economist at Johns Hopkins University who previously served on President Reagan’s Council of Economic Advisers, views the initiatives primarily as political responses to fears of monetary disruption.

“The idea that somehow the dollar is gonna be displaced and people are gonna de-dollarize, it’s just not gonna happen,” Hanke said.

Yet he also acknowledged a cultural dimension behind the policies. States with strong extraction industries often maintain a closer relationship with commodity markets.

“They’re commodity states,” Hanke said. “They have ranches; they have mines. The talk, the chatter is always what’s happening to commodity prices.”

For now, the scale of these programs remains small relative to state investment portfolios and insignificant relative to global gold markets. Wyoming’s purchase represents only a fraction of its trust fund assets and a microscopic share of worldwide bullion supply.

Still, the symbolism is difficult to miss. At a moment when national debt and monetary policy dominate political debate, some U.S. states are quietly placing physical gold back onto their balance sheets.

The amounts may be modest today. The policy signal is considerably larger.

Continues here

Free Posts To Your Mailbox