The War Machine and The Printing Press

What’s behind the numbers?

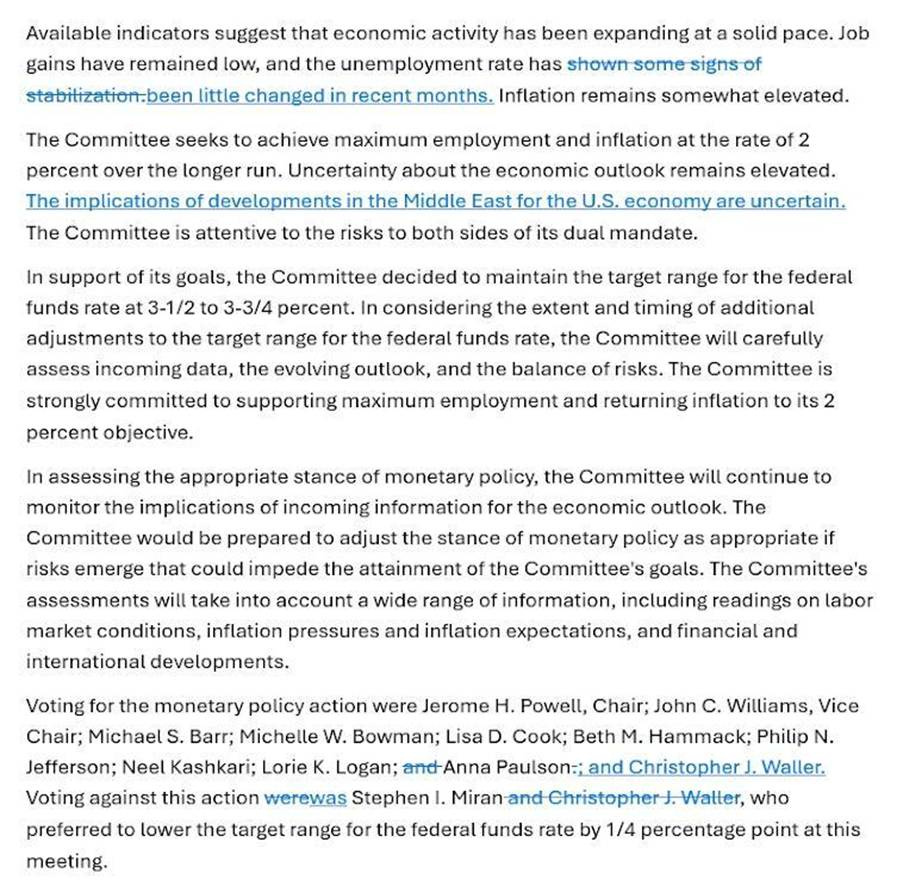

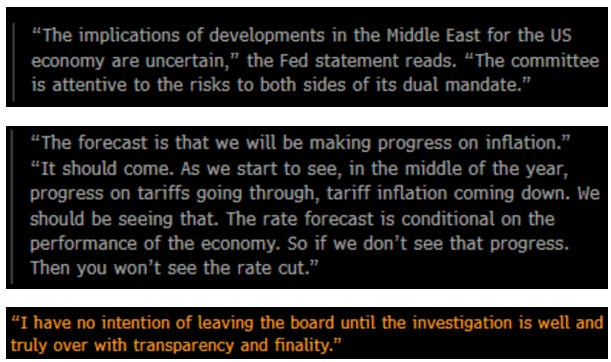

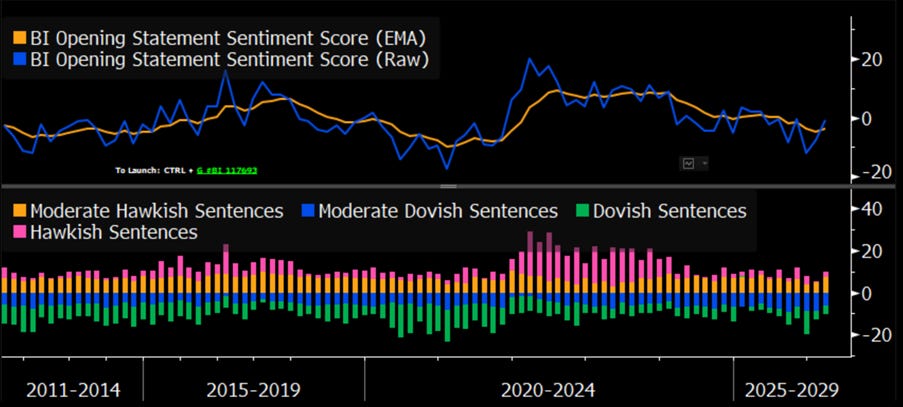

As predictably as a pre-written script of a holy war, the Federal Reserve voted 11–1 to keep rates comfortably parked at 3.5%–3.75%, with Stephen Miran bravely auditioning for the role of “lone dissenter” by suggesting a modest cut. The Federal Reserve delivered exactly what markets were promised: a masterclass in saying almost nothing with great precision. The labor market was gently downgraded from “some signs of stabilization” to the far more thrilling “little changed,” while the war in the Middle East earned a brief cameo as “uncertain”—a bold analytical breakthrough. In short, the statement was carefully engineered to avoid signaling anything at all, while reassuring everyone that the Fed is, as always, “closely monitoring” developments it cannot control.

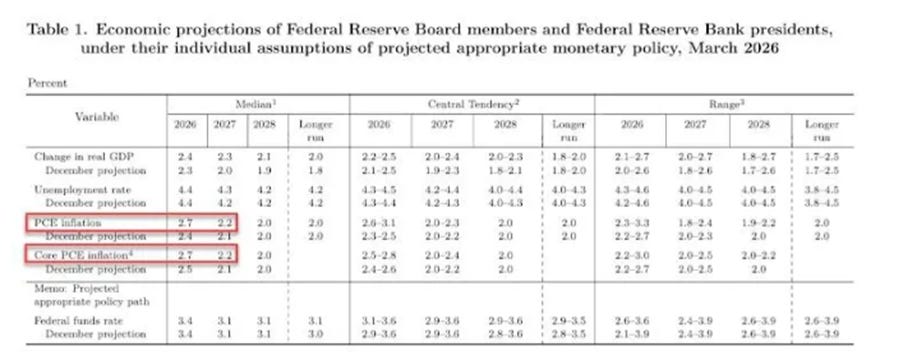

In its latest projections, the Fed now expects core inflation to settle at 2.7% by end-2026 (because optimism is policy), while GDP growth was nudged up to 2.4%—a reminder that in central banking, the forecast is always just one revision away from perfection.

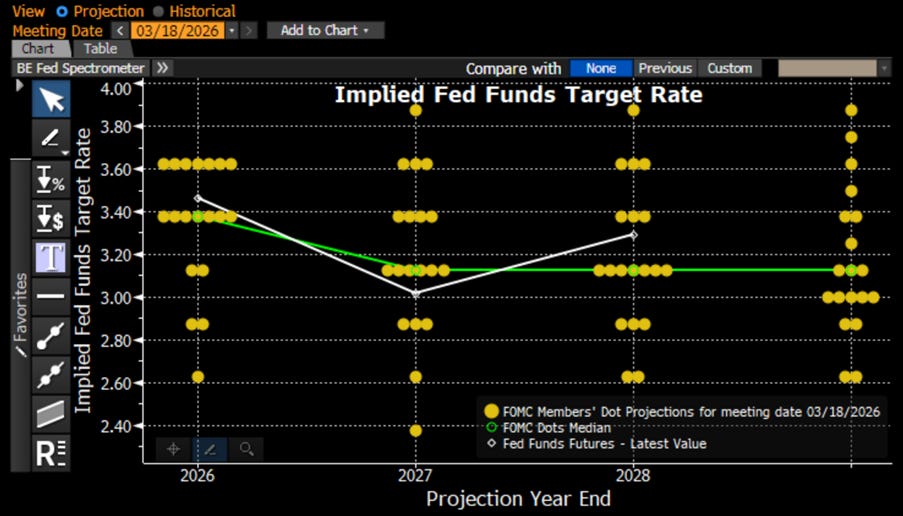

The latest “dot plot” from the Federal Reserve shows a committee delicately split between doing nothing and doing almost nothing—seven members favor holding rates steady through year-end, while twelve still cling to the hope of at least one cut. By 2027, rate hikes have practically gone extinct, with only one lonely outlier still believing in them. Officially, the Fed maintains its forecast of one cut in 2026 and another in 2027, while already quietly acknowledging higher inflation expectations—likely a polite nod to rising oil prices rather than any sudden outbreak of honesty. The message, as always: policy remains “data-dependent,” but the data has already been gently nudged to fit a slightly higher inflation baseline.

At the press conference, Jerome Powell tackled the oil shock from the ‘Epstein Fury’ with admirable clarity: nobody knows anything. Faced with repeated questions, he explained that the economic impact could be bigger, smaller, much bigger, or much smaller—an impressively comprehensive forecast. On his own future, he remains equally decisive, confirming he may or may not stay, but will definitely remain for now. As for stagflation, Powell firmly rejected the comparison to the 1970s, arguing that despite slowing growth and persistent inflation, this is not that kind of stagflation—just a different, more modern version of the same problem.

According to the Fed Sentiment model, Jerome’s opening remarks took another small step away from dovishness—but only a small one..

Thoughts.

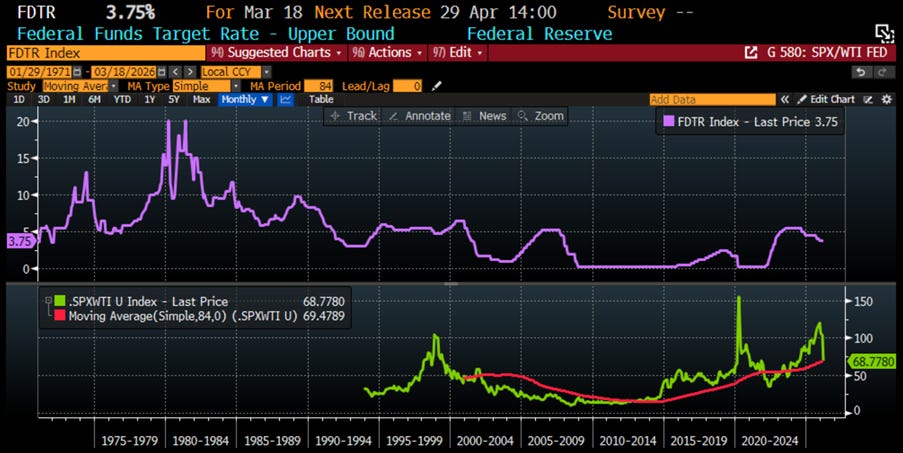

While Wall Street and Donald Trump continue their favorite magic trick—convincing investors that the Federal Reserve can steer the business cycle—the reality is less enchanting: in every inflationary bust driven by rising oil prices, the Fed has historically been forced to raise rates, not cut them.

FED Fund Rate (purple line); S&P 500 Index to Oil ratio (green line); 7-Year Moving Average of S&P 500 Index to Oil ratio (red line).

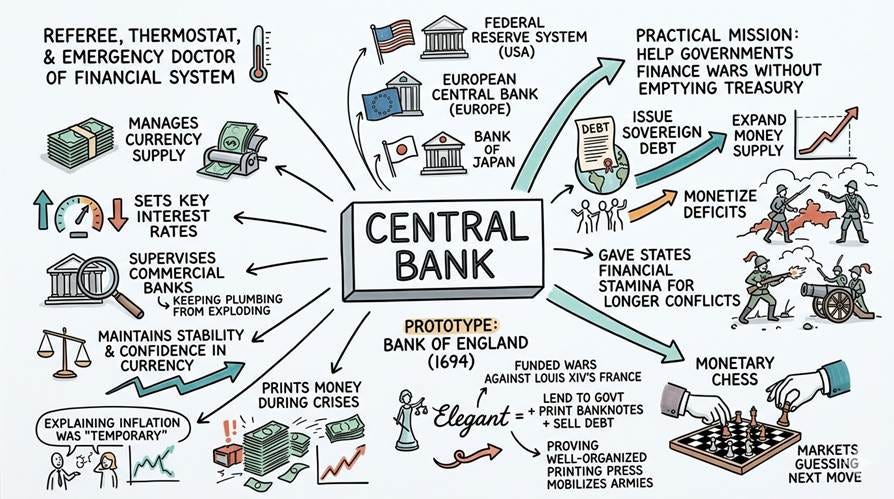

War and money have long walked the same path. A ruler who empties his treasury cannot sustain his armies, just as an army without provisions cannot march far. From the earliest kingdoms to the modern state, those who govern have depended on financial systems capable of gathering vast resources swiftly when danger approaches. In the present age, the institution that has perfected this task beyond all others is the central bank.

A central bank is the institution in charge of a country’s monetary policy and its currency—something like the referee, thermostat, and emergency doctor of the financial system all at once. It manages the supply of currency, sets key interest rates, and keeps an eye on commercial banks to make sure the plumbing of the financial system does not explode at the worst possible moment. In theory, it exists to maintain stability and confidence in the currency; in practice, it often finds itself printing money during crises and explaining afterward why inflation was “temporary.” Famous examples include the Federal Reserve System in the United States, the European Central Bank in Europe, and the Bank of Japan—institutions that spend their days moving interest rates up or down while financial markets try to guess their next move like a high-stakes game of monetary chess.

Central banks were not created merely to smooth business cycles, despite what economic textbooks politely suggest. Their more practical mission was to help governments finance wars without immediately emptying the treasury. By issuing sovereign debt, expanding the money supply, and monetizing deficits, central banks gave states the financial stamina to fight longer conflicts. The prototype appeared with the creation of the Bank of England in 1694, when Britain needed a clever way to fund its wars against Louis XIV’s France. The solution was elegant: create a bank that could lend money to the government and print banknotes while investors happily bought the debt. The formula worked so well that it quietly spread across the world—proving that when it comes to war, nothing mobilizes armies faster than a well-organized printing press.

The same logic eventually shaped the financial architecture of the United States. When the Federal Reserve System was created in 1913, the country had already endured several banking panics, including the famous Panic of 1907. Officially, the new institution was meant to stabilize the financial system and prevent future crises. Yet history has a sense of timing: only a few years later, the world plunged into the catastrophe of World War I. The young Federal Reserve quickly found a more practical role—helping finance the war. The U.S. government issued vast quantities of Liberty Bonds, while the Fed ensured the financial system had enough liquidity to absorb them, expanding bank reserves and effectively supporting the surge in public debt.

The same mechanism appeared again during World War II. To finance the fight against the Axis powers, Washington issued enormous amounts of Treasury debt, and the Federal Reserve agreed to cap long-term yields to keep borrowing costs low. In practice, this meant the central bank was ready to purchase government bonds whenever necessary—an elegant way of monetizing wartime spending. The arrangement allowed the United States to mobilize extraordinary financial resources without triggering a debt crisis, turning the Federal Reserve, at least temporarily, into the quiet financial partner of the U.S. Treasury.

Read more and discover how to trade it here: https://themacrobutler.substack.com/p/the-war-machine-and-the-printing

Visit The Macro Butler Website here: https://themacrobutler.com/

Join The Macro Butler on Telegram here : https://t.me/TheMacroButlerSubstack

You can contact The Macro Butler at info@themacrobutler.com

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence