Continues here

Gold's Next Leg— The 1970s Playbook is Back

Little-Picture Context

Authored by GoldFix

Fresh from breaking down both CITI’s latest Gold report reiterating $6,000 in ‘26; and Goldman’s pushback on naysayers we read Fred Hickey’s latest excellent HTS report, in which several grounded takeaways on gold stood out. They’re worth highlighting—Hickey is echoing themes we’ve recently emphasized here, and ones we’ve seen play out before, particularly in the 1970s, supported by relevant historical charts.

To Start Off— Gold’s liquidity remains a defining feature;1 it allows for efficient price discovery and rapid positioning shifts. That is why we believe events like Turkey’s selling (discussed below) actually make the case for Gold as an HQLA/REPO asset

In periods of stress, however, that same liquidity can facilitate short-term liquidation. Yet, the recent correction across precious metals has materially reset sentiment, reduced speculative excess, and lowered the probability of a near-term disorderly drawdown.

Quarter Recap Technically

In early Q1, the precious metals complex exhibited clear signs of speculative excess. Sentiment reached extreme levels, with (Fred notes) the Daily Sentiment Index approaching 90% bullish. ETF inflows were substantial, with 148 tons added to GLD and 52 tons to GLDM between August and February. Futures positioning surged, with open interest peaking near 550,000 contracts and daily volume hitting 656,000 contracts in late January, while Chinese markets showed similarly elevated activity alongside rising margin requirements.

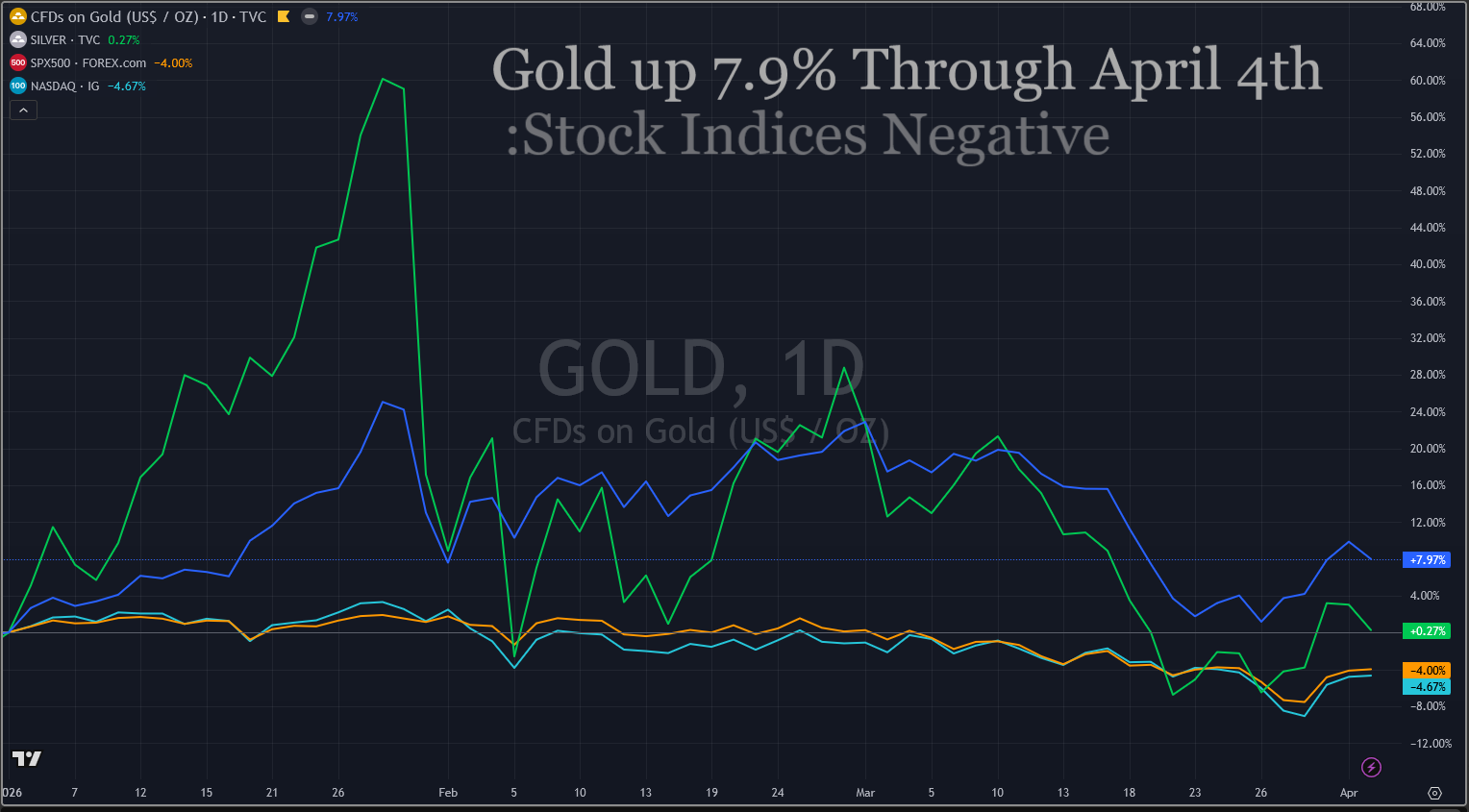

Technical indicators confirmed the overheating. Gold’s RSI reached 90%, MACD momentum extended beyond prior ranges, and the Gold Miners Bullish Percent Index hit 100%. Prices peaked at $5,600 before a sharp correction to $4,100, marking a 27% decline in seven weeks; silver fell by roughly half.

Despite this, year-to-date performance remains positive, with gold up 7.6%, silver up 3%, and gold miners outperforming broader equity indices.

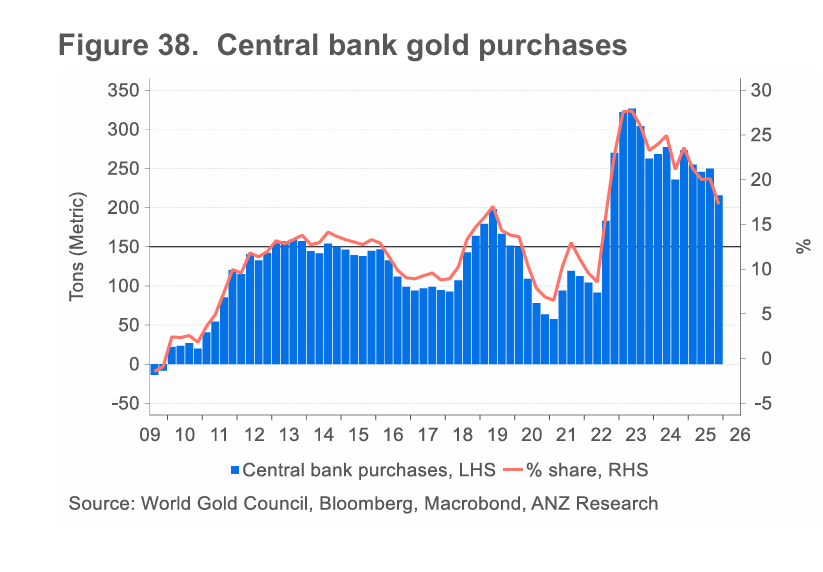

Central Bank Selling Was Not Abnormal

Recent central bank activity has been cited as a source of pressure on gold, though the underlying dynamics appear more cyclical than structural. Russia’s central bank reduced holdings in January and likely February, consistent with its pattern of actively managing reserves without materially altering its long-term gold position. Rising oil prices, which improve Russia’s external balance, may ultimately offset the need for continued sales.

Turkey’s actions reflect a similar pattern of tactical intervention. The central bank sold or swapped approximately 58 to 60 tons in March to stabilize the lira, mirroring prior behavior in early 2023 when larger sales were used to manage external imbalances. That episode was followed by nearly two years of consistent repurchasing, suggesting these moves are temporary liquidity measures rather than a reversal of broader accumulation trends. In effect, Turkey is just trading around its core gold position opportunistically.

Central bank activity in February showed a return to net accumulation following a brief pause. Poland’s central bank (rumored to be selling) actually added 20 tons to its gold reserves, reinforcing its ongoing diversification strategy. On taht note, Who was the buyer of Turkey’s Gold is probably of more importance than the sales themselves. Because given the massive dumping of metal, Gold should/could have fallen much further.

It was reported that Poland’s central bank was considering selling some of its gold to fund its increased defense spending, but that idea was ultimately nixed (at least for now) by the government.

Goldman Pushes Back on Gold-Doubters

Goldman Sachs argues gold’s recent sell-off reflects positioning unwinds and higher-rate repricing, not structural weakness. Supply-driven inflation pressures gold short term, but normalized positioning, expected Fed easing, and strong central bank demand support a medium-term rebound, with upside driven by portfolio reallocation and downside limited to liquidation scenarios.

Miners Best Quarter Ever?

Moving on to miners, we have noted repeatedly that earnings this Q1 for 2026 will likely be the best earnings ever and have taken positions to that effect in this dip adding to WRLG and creating GDX speculative length headed into it.

Contributor posts published on Zero Hedge do not necessarily represent the views and opinions of Zero Hedge, and are not selected, edited or screened by Zero Hedge editors.

Loading...