Continues here

The Petrodollar Breakdown is Real

TL; DR

The petrodollar loop is breaking down as the longstanding exchange of U.S. security for recycled Gulf dollar flows into Treasuries weakens

Foreign central banks have shifted into sustained Treasury selling, with New York Fed custody holdings falling roughly $82B to $2.7T

The Iran conflict is disrupting both sides of the system: importers are liquidating Treasuries for dollar liquidity, while exporters face constrained oil flows and reduced surplus generation

INTRO

Authored by GoldFix

After reading a Bloomberg opinion piece1 deconstructing the Petrodollar stresses currently manifesting from the war with Iran the following became apparent.

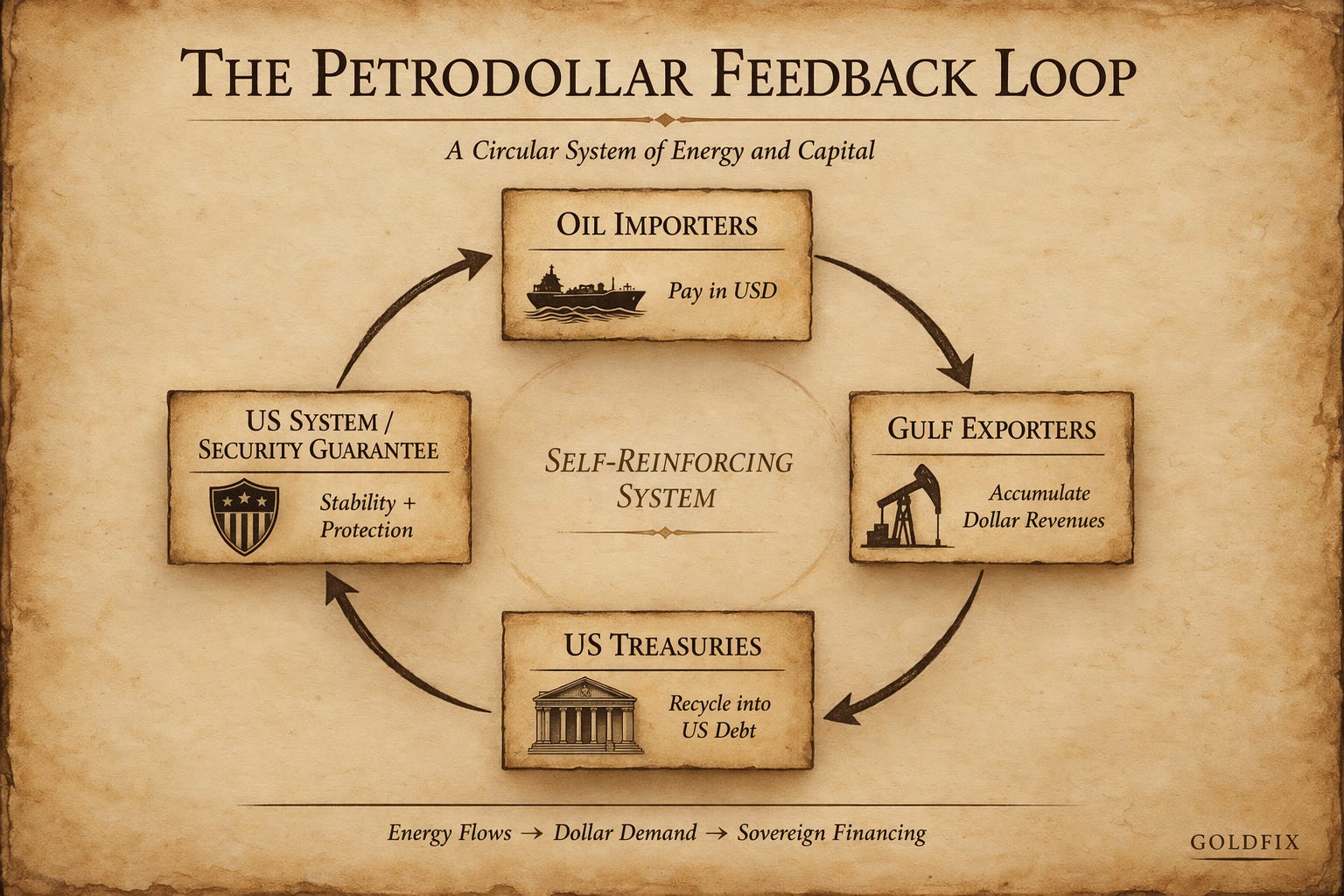

The longstanding financial arrangement in which the United States underwrote stability in the Middle East in exchange for Gulf states recycling dollar revenues into US Treasuries has fractured. What functioned for decades as a reinforcing loop between energy flows, dollar demand, and sovereign financing is now under strain.

The framework traces back to the 1974 agreement engineered under Henry Kissinger, in which Saudi Arabia priced oil in dollars and reinvested surpluses into US assets, primarily Treasuries. Other Gulf states followed, while the United States provided security guarantees and maintained the broader geopolitical order.

A Circular System of Energy and Capital

The system operated with internal consistency. Oil-importing nations paid in dollars; those dollars accumulated in Gulf economies; and surpluses were recycled into US government debt. This loop supported US borrowing conditions and reinforced the dollar’s reserve status.

That structure depended on two continuous processes: surplus generation through energy exports, and reinvestment into US assets. Both are now disrupted.

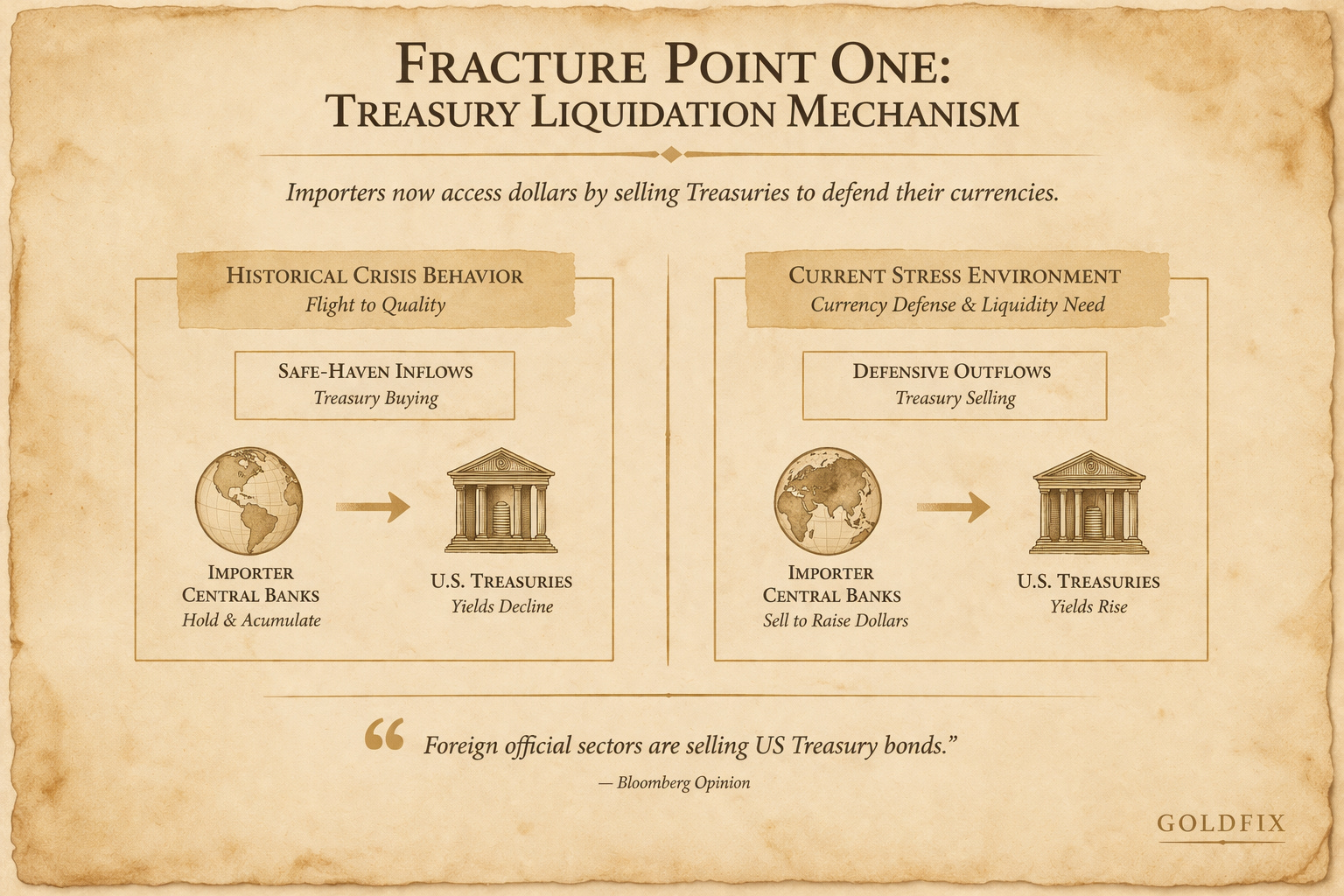

Fracture Point One: Importers Liquidate Treasuries

Following the escalation of the US-Israeli conflict with Iran, foreign central banks have shifted into sustained Treasury selling. Holdings at the Federal Reserve Bank of New York declined by roughly $82 billion over five consecutive weeks to $2.7 trillion, the lowest level since 2012.

At the same time, yields diverged from historical crisis behavior. The 10-year Treasury yield rose from 3.9% to above 4.4% instead of falling under safe-haven demand.

“Foreign official sectors are selling US Treasury bonds.”

The mechanism reflects currency defense. Oil-importing economies such as Turkey, India, and Thailand face rising dollar-priced energy costs alongside weakening domestic currencies. Stabilization requires dollar liquidity, sourced through Treasury sales.

Dollar Demand Turns Defensive

Dollar demand remains present, yet its form has shifted. Central banks are accessing liquidity through liquidation rather than accumulation. Treasuries function as a funding tool under stress rather than a passive reserve asset. A system built on steady accumulation behaves differently when forced into periodic selling.

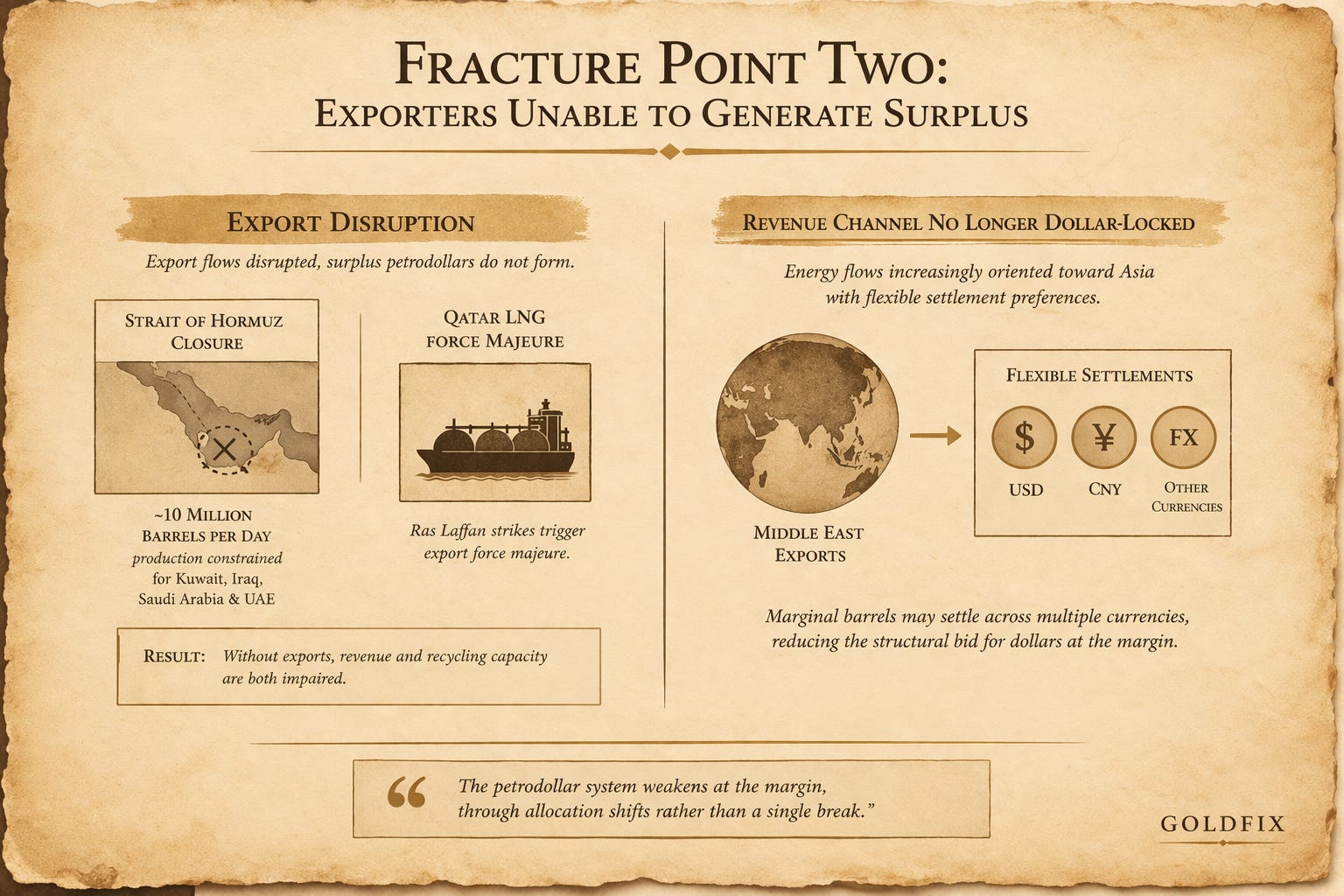

Fracture Point Two: Exporters Unable to Generate Surplus

Historically, higher oil prices increased Gulf revenues, reinforcing demand for dollar assets. This relationship has broken down. The closure of the Strait of Hormuz has constrained exports across Kuwait, Iraq, Saudi Arabia, and the UAE, with production cuts of roughly 10 million barrels per day.

Qatar’s declaration of force majeure on LNG exports following strikes on Ras Laffan further highlights the disruption.

Without export flows, surplus petrodollars do not form. The loop requires both income generation and reinvestment capacity. Both are impaired.

The Revenue Channel Is No Longer Dollar-Locked

This disruption intersects with a broader shift already underway. Middle East energy flows have increasingly oriented toward Asia, where settlement preferences are more flexible and, in some cases, non-dollar.

If export channels normalize under new conditions, marginal barrels may settle across multiple currencies. Incremental diversification reduces the structural bid for dollars without requiring full displacement.

The petrodollar system weakens at the margin, through allocation shifts rather than a single break

Balance Sheet Pressure Across Gulf Sovereigns

Kuwait, Saudi Arabia, and the UAE held roughly $300 billion in Treasuries as of January. These holdings now sit alongside declining revenues, elevated defense spending, and a reassessment of outward investment commitments.

Sovereign entities are reportedly reviewing force majeure clauses tied to prior investment pledges, including allocations to US assets.

Free Posts To Your Mailbox

Contributor posts published on Zero Hedge do not necessarily represent the views and opinions of Zero Hedge, and are not selected, edited or screened by Zero Hedge editors.

Loading...