Continues here

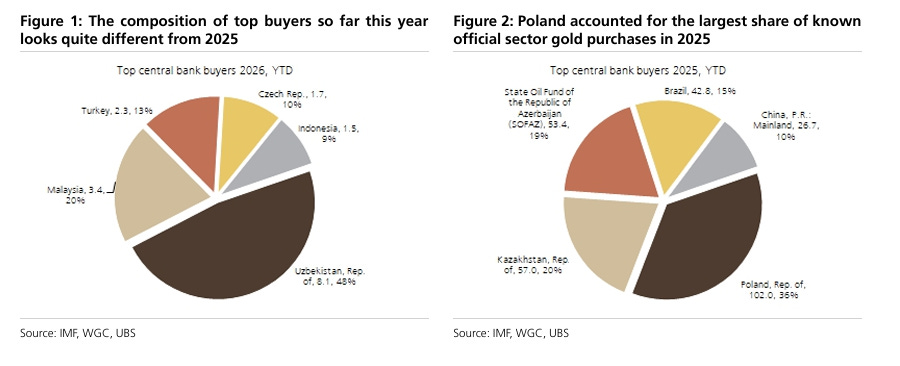

UBS: Was Turkey Selling Gold an exception or not?

Central bank gold buying remains structurally intact despite recent market volatility and price declines. UBS argues current selling concerns are overstated, with official sector demand likely moderating, not reversing. Strategic buyers have paused amid volatility, while China demand stabilizes prices, leaving medium-term upside supported by inflation risks and geopolitical uncertainty.

Central Bank Gold Buying: Cyclical Pause or Structural Shift?

Authored by GoldFix

Gold markets have come under pressure in recent weeks, with prices declining sharply amid geopolitical volatility and tightening financial conditions. The central question emerging across market participants is whether official sector demand, a key pillar of the gold bull case, is beginning to reverse or simply entering a temporary pause.

According to a recent report by UBS Global Research, central bank gold buying remains intact as a structural trend, despite concerns that selling activity contributed to the roughly 16% decline in gold prices during March. The bank frames current developments as cyclical rather than indicative of a broader regime shift in official sector behavior.

From Buyers to Sellers? Market Concerns vs Structural Reality

Recent price action, combined with escalating geopolitical tensions, has led to speculation that central banks may be forced to liquidate gold reserves to manage inflation, currency weakness, and slowing growth. These concerns have been amplified by reports of selling activity, particularly in emerging markets.

“Although we cannot rule out central bank gold selling, we think it is very unlikely that there is a structural shift in the official sector trend.”

The report emphasizes that intermittent selling is not uncommon and does not necessarily indicate a reversal in long-term positioning. Over the past fifteen years, central banks have steadily accumulated gold, and periodic reductions in holdings have historically reflected tactical adjustments rather than strategic exits.

UBS continues to project net official sector purchases of approximately 800 to 850 tonnes in 2026, slightly below the roughly 860 tonnes recorded in 2025, suggesting moderation rather than reversal in demand.

Interpreting Turkey: Policy Tool vs Market Signal

Recent reports indicating that Turkey sold approximately 50 tonnes of gold have drawn significant attention. However, the report cautions against interpreting these flows at face value.

Turkey’s gold reserves operate within a unique policy framework, where gold is used as a liquidity management tool within the domestic banking system. A portion of reported reserves reflects commercial bank positions, and transactions may include swaps rather than outright sales.

As a result, headline figures may not accurately represent directional positioning by the central bank itself. More granular data is required to distinguish between policy-driven adjustments and genuine reserve liquidation.

Strategic Buyers Step Back Amid Volatility

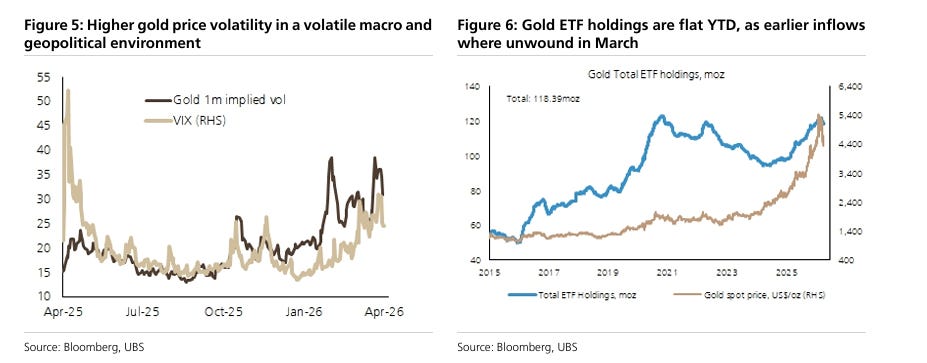

The report highlights a shift in market participation during the recent selloff. Central banks and other long-term investors, typically active buyers on price weakness, have remained largely on the sidelines.

This pause appears to be driven by heightened price volatility and macro uncertainty. The gold market had already been consolidating prior to the escalation in Middle East tensions, and the increase in volatility reinforced a wait-and-see approach among strategic allocators.

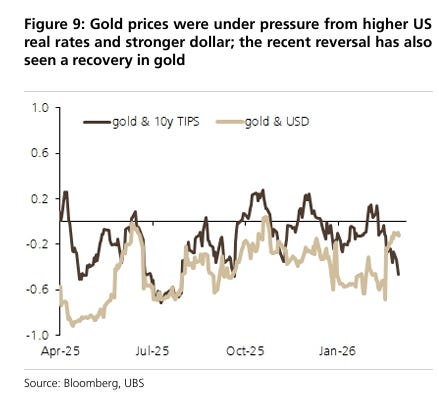

In the absence of consistent dip-buying from these participants, gold’s short-term price dynamics have become more sensitive to macro variables, particularly U.S. real interest rates and the strength of the dollar. Rising real yields and a stronger dollar contributed to liquidation of long positions and the emergence of short selling during the March decline.

China Demand and Market Stabilization

Despite the pullback in Western investment flows, physical demand from China has provided a stabilizing force for the market. Onshore premiums and continued inflows into Chinese investment channels have helped anchor prices during periods of stress.

Free Posts To Your Mailbox

Contributor posts published on Zero Hedge do not necessarily represent the views and opinions of Zero Hedge, and are not selected, edited or screened by Zero Hedge editors.

Loading...