Silver Institute: Silver Enters a Squeeze Regime

Silver’s market has shifted into a structural deficit regime, with six consecutive shortages drawing down global inventories. Supply growth remains constrained, while investment demand is replacing fabrication demand. This imbalance is tightening physical availability and increasing volatility, leaving higher prices as the primary mechanism to restore equilibrium in an increasingly fragile market.

The Silver Market Has Entered a Structural Tightness (Squeeze) Regime

Authored by Vince Lanci of GoldFix for Scottsdale Mint

Key Points

- Structural deficit regime: Silver has entered a multi-year shortage (6 straight deficits), with inventories steadily declining and no return to equilibrium in sight.

- Supply cannot catch up: Modest mine growth and recycling are constrained by byproduct dynamics and bottlenecks, limiting the system’s ability to respond.

- Demand is shifting, not falling: Industrial softness is being replaced by strong investment demand (coins, bars, ETFs), tightening the physical market further.

- Only resolution is price: With supply inelastic and inventories shrinking, the imbalance clears through higher and more volatile prices.

The global silver market is no longer operating within a cyclical framework at all. What was once a balance between industrial demand, investment flows, and responsive supply has shifted into a structurally constrained system defined by persistent deficits, declining inventories, and increasingly unstable liquidity conditions. Price is no longer the primary balancing mechanism. Availability is.

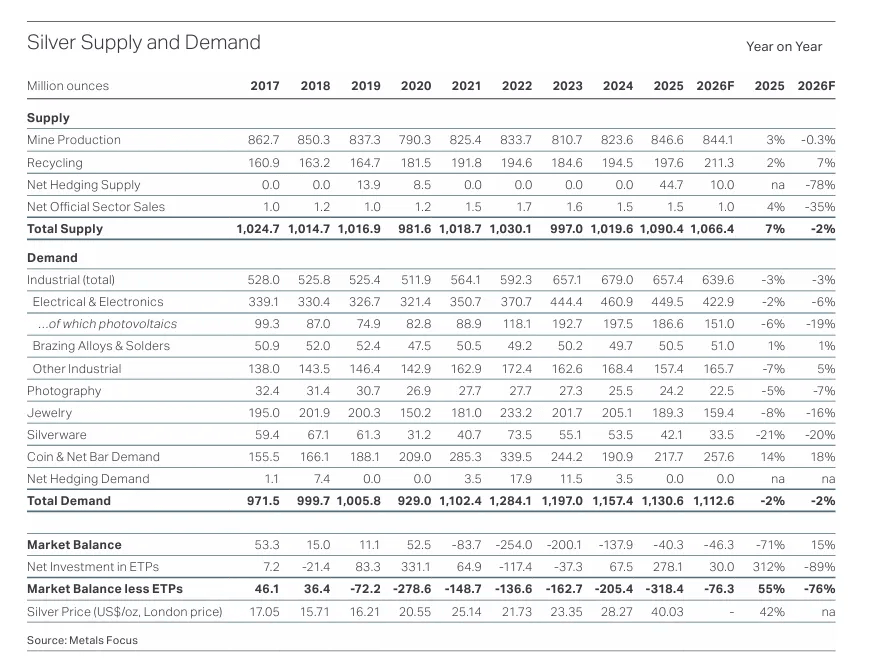

In the latest World Silver Survey 2026 from The Silver Institute, produced by Metals Focus, the data confirms that 2025 marked the fifth consecutive annual deficit, with a sixth already projected for 2026. This extends a multi-year drawdown in above-ground stocks and signals a transition away from equilibrium toward a structurally tight physical market.

“This was the fifth consecutive annual shortfall… adding further pressure to global stocks.”

Supply Growth Exists, But It Is Not Enough

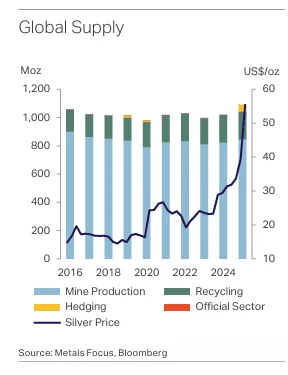

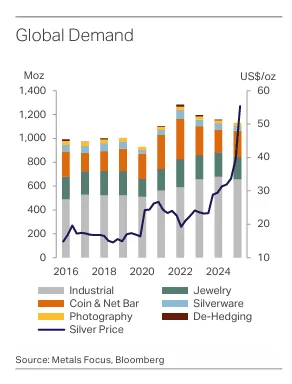

Global silver supply rose meaningfully in 2025, increasing 7% to just over 1.09 billion ounces. Mine production contributed a 3% gain, led by Latin America, while recycling rose to a 13-year high. On the surface, this appears to be a constructive response to higher prices.

The underlying structure tells a different story.

Supply growth remains incremental and reactive rather than transformative. The majority of silver production continues to come as a byproduct of base metal mining, limiting the industry’s ability to respond directly to silver-specific price signals. Even where prices incentivize recycling, bottlenecks in refining capacity and logistical constraints cap the upside.

“Recycling… was capped due to refinery bottlenecks which were exacerbated by elevated lease rates.”

Looking ahead, the report forecasts a slight decline in mine supply for 2026, reinforcing the view that the current supply base lacks the elasticity required to resolve the deficit. The absence of large-scale new projects and the reliance on incremental expansions suggest that supply will remain structurally constrained.

This is the first key imbalance. Supply is responding, but not fast enough, and not at scale.

Demand Is Rotating, Not Disappearing

Total silver demand actually declined modestly in 2025, falling 2% to 1.13 billion ounces. At first glance, this suggests weakening fundamentals. A deeper examination reveals a rotation rather than a contraction.

Industrial demand declined 3%, driven primarily by photovoltaic thrifting and substitution. Jewelry and silverware demand also fell sharply due to price sensitivity, particularly in India and Europe. These are price-elastic segments, and their response is consistent with historical behavior.

The critical shift is occurring elsewhere.

Investment demand surged. Coin and bar demand rose 14%, while ETP inflows reached one of the highest levels on record. This was not a marginal adjustment. It was a structural handoff.

“Coin and net bar demand rebounded by 14%, with sizable gains in several regions.”

“ETP holdings… generated a severe physical squeeze in the London market.”

Physical investment is replacing fabrication demand as the marginal driver of the market. This matters because investment demand is less sensitive to price and more responsive to macro conditions, monetary instability, and scarcity narratives.

The second imbalance emerges here. Demand is no longer anchored solely in industrial use. It is increasingly financial, discretionary, and reflexive.

Deficits Are Persisting, and Inventories Are Paying the Price

The most important data point in the report is not annual supply or demand. It is the continuation of the deficit.

2025 recorded a shortfall of 40.3 million ounces. 2026 is projected to widen slightly to 46.3 million ounces. This marks six consecutive years of deficits, with cumulative drawdowns now reaching hundreds of millions of ounces.

“With deficits set to remain in place… it is unlikely that we will see a return to the previous status quo any time soon.”

These deficits are being absorbed by above-ground stocks. That process is finite. As inventories decline, the system becomes increasingly sensitive to marginal flows. The result is not gradual repricing. It is episodic instability.

The October 2025 liquidity squeeze serves as a case study.

“An unprecedented liquidity squeeze… stressed parts of the supply chain for refining and manufacturing.”

This is the third imbalance. The market is no longer clearing through smooth price discovery. It is clearing through inventory depletion and periodic dislocations.

Price Is Finally Beginning to Reflect Structure

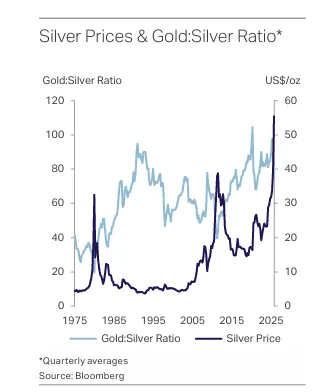

Silver’s price action in 2025 and early 2026 reflects this evolving structure. The annual average rose 42% year-over-year to just over $40, while spot prices exceeded $120 during periods of acute tightness.

These moves are not isolated events. They are manifestations of a system under strain.

Continues here (unlocked)

Free Posts To Your Mailbox