Barrels for Debt: The Coming Middle East Reckoning

Debt is often spoken of as if it were a balanced instrument—neither good nor bad, merely a bridge between present desire and future attainment. Such a view is comforting, yet it clouds judgment. In truth, debt is seldom neutral. It carries within it an imbalance of power. It binds the borrower to the lender, ties today’s decisions to tomorrow’s obligations, and when taken without restraint, may bend even sovereignty toward dependence.

At its root, debt is a claim upon what has not yet been produced. It draws from the future to satisfy the present, sustained by laws, institutions, and the authority of the state. When governed with discipline, it may serve order and development. But when it grows beyond the capacity to be honoured, it loses harmony. What was once a tool can become an instrument of constraint—not by intent, but by structure. Thus, the wise understand that conflict need not arise from force alone. When obligations outweigh means, the act of repayment itself becomes a field of contest. No armies are required when imbalance has already taken hold. In this, one may observe the present condition of the Middle East, where the seeds of obligation have been sown beyond measure, and the test of balance approaches.

https://www.imf.org/external/datamapper/GG_DEBT_GDP@GDD/CHN/FRA/DEU/ITA/JPN/GBR/USA/FADGDWORLD

In the teachings of the old masters, it is said that when a man borrows a small sum, he sleeps lightly; when he borrows greatly, it is the lender who sleeps peacefully. So, it is with nations. Debt, when kept in proper measure, behaves like a well-trained servant—useful, discreet, and easily dismissed. But when it grows beyond what can be repaid, is endlessly rolled forward, and invites the lender to whisper advice into matters of state, it sheds its humble robe and begins to act like an uninvited elder at the family table. At first, there is optimism—grand plans, fine speeches, and confident nodding. Then comes dependence, as obligations pile up like unpaid tea bills. And before long, the borrower discovers, with some embarrassment, that he is no longer hosting the banquet but merely attending it, while the creditor quietly rearranges the seating. Thus, without a single soldier crossing the border, authority changes hands—not by force, but by the gentle, persistent weight of obligation.

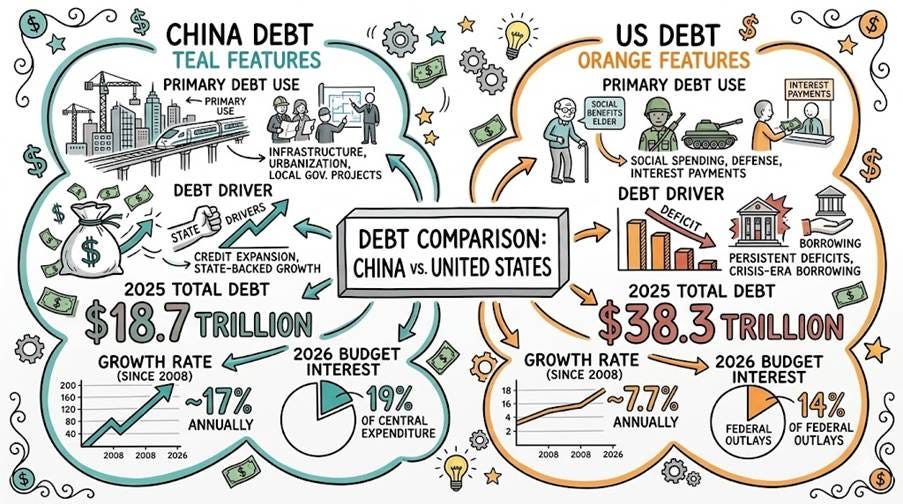

Not all debt is invited to the same banquet. When a state borrows to build roads, ports, and industries—as in the case of China—the debt at least brings tools to work and may one day repay its host with greater prosperity. But when a state borrows to consume—to fund endless trinkets, generous social promises, and distant geopolitical adventures—as in the United States—the debt arrives empty-handed, eats heartily, and leaves the bill for future generations. One might say the first plants an orchard and hopes for fruit, while the second hosts a perpetual feast where the guests grow louder, the dishes more extravagant, and the kitchen increasingly indebted. In both cases, the tea must eventually be paid for—but only one has a chance of having grown the leaves.

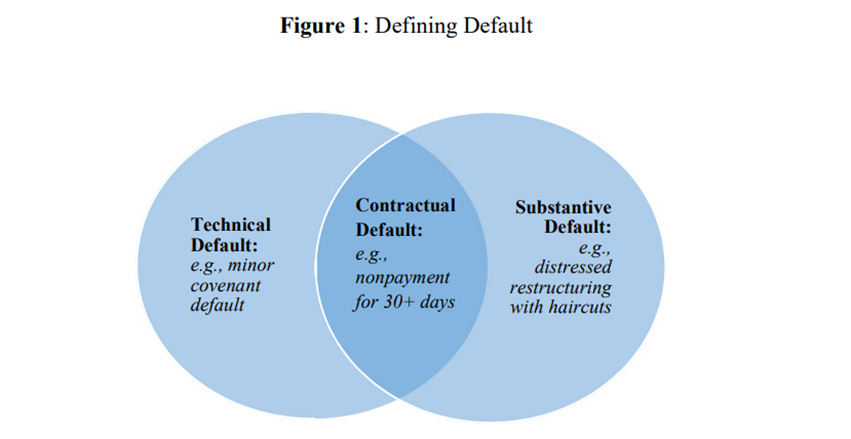

When a state borrows too much, it does not fall in a single dramatic bow but rather performs a series of increasingly creative excuses. Sovereign default, then, is not one event but a full banquet of outcomes. Sometimes the ruler simply refuses to pay at all—this is the loudest gesture, like flipping the table and sending creditors running for the door. At other times, he pays, but with adjustments: “Let us extend the timeline, reduce the burden, and call this wisdom,” he says, while quietly serving a smaller portion—this is the polite default, dressed as negotiation. Then there is the selective approach, where some guests are honoured and others are conveniently forgotten, depending on who sits closest to power. The more subtle ruler misses a deadline here, bends a rule there, claiming it is merely a technical matter—though the cracks begin to show. And finally, the most refined method of all: he repays in coin so diminished that the creditor receives much but holds little, thanks to inflation, devaluation, and the gentle confinement of capital. In every age, the forms differ, yet the lesson remains unchanged: when obligations exceed virtue, repayment becomes a matter not of ability, but of ingenuity.

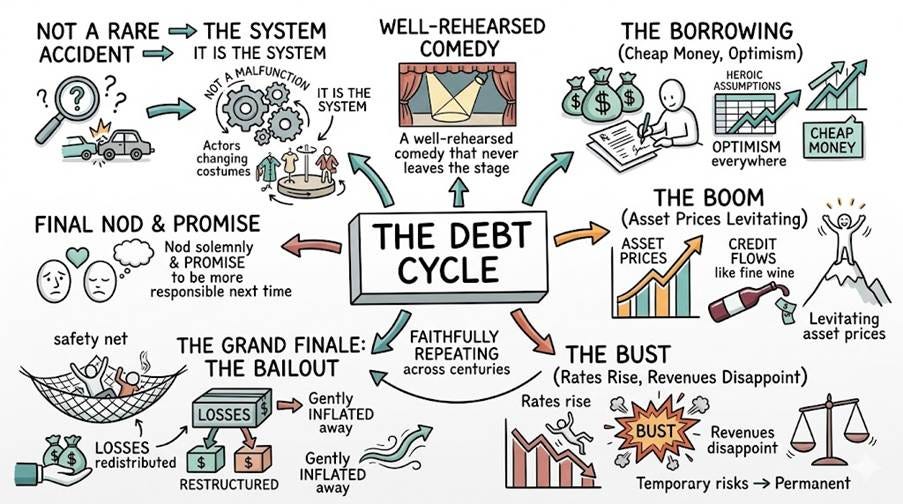

The debt cycle is often treated like a rare accident, when in reality it behaves more like a well-rehearsed comedy that never leaves the stage. First comes the borrowing—money is cheap, optimism is everywhere, and everyone suddenly becomes a visionary with spreadsheets full of heroic assumptions. Then arrives the boom, where asset prices levitate, credit flows like fine wine, and confidence reaches a level usually reserved for lottery winners. Inevitably, the bust crashes the party—rates rise, revenues disappoint, and all those “temporary” risks reveal their permanent nature. Finally, the grand finale: the bailout, where losses are politely redistributed, quietly restructured, or gently inflated away, allowing everyone to nod solemnly and promise to be more responsible next time. It is not a malfunction of the system—it is the system, faithfully repeating its favourite joke across the centuries, with only the actors changing costumes.

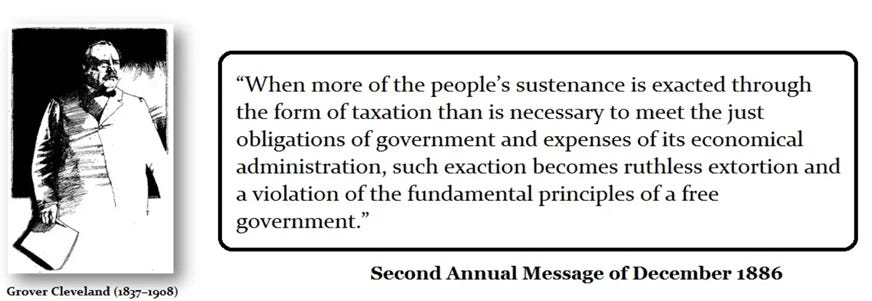

Governments begin gently, with taxation framed as duty and necessity—but as deficits swell and interest payments rival entire ministries, the tone shifts from request to requirement. In the United States, trillion-dollar deficits are no longer an emergency but a routine, and so the search for revenue expands into once-unthinkable territory: wealth taxes, levies on unrealized gains, transaction tolls on capital itself. Predictably, those with means begin to move—out of high-tax states, across borders, beyond reach—triggering a quiet panic within the system. What follows is a familiar escalation: tighter rules, exit taxes, and the slow construction of digital frameworks designed not merely to observe but to contain. In this evolution, taxation ceases to be a tool of funding and becomes an architecture of control, where the objective is no longer to collect from prosperity, but to ensure that prosperity has nowhere left to go.

The comforting tale says that developed nations are too refined to default—that their debts are sacred and always repaid in full, like a gentleman settling his accounts before tea. Reality, however, has a more mischievous sense of humour. Countries repay when it is convenient, and default when it is necessary—preferably with a well-crafted explanation. They always have, and they always will. For in the end, default is not decided by spreadsheets but by politics: when honouring the debt begins to...

Read more and discover how to trade it here: https://themacrobutler.substack.com/p/barrels-for-debt-the-coming-middle

Visit The Macro Butler Website here: https://themacrobutler.com/

Join The Macro Butler on Telegram here : https://t.me/TheMacroButlerSubstack

Register your interest to The Macro Butler World Economic Summit 2026 here:

https://themacrobutler.substack.com/p/the-macro-butler-world-economic-s…

You can contact The Macro Butler at info@themacrobutler.com

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence