Continues here

Goldman Raises Oil Target With $120 on Radar

Just one week after Bank of America stated Oil futures were way too cheap Goldman and Deutsche Bank seemingly concur and put out their own price upgrades for Oil. Markets are facing a sustained supply shock driven by Hormuz disruptions, enforcement actions, and delayed recovery timelines. Record inventory draws are tightening conditions despite softer demand, while limited supply response keeps the market undersupplied. Price risks are skewed higher, with forecasts rising and upside scenarios pointing to significantly elevated oil prices.

Escalating Supply Shock and the Repricing of Oil Risk

Authored by GoldFix

The global oil market is shifting from episodic disruption to a cumulative supply shock. What began as a localized bottleneck around the Strait of Hormuz has evolved into a layered constraint system involving reduced flows, active enforcement, and delayed recovery timelines. The result is a tightening supply profile that is overwhelming baseline expectations and forcing a repricing of risk.

Analysis from Deutsche Bank and Goldman Sachs converges on three points. Disruption is intensifying, normalization is being pushed out, and price outcomes are skewing higher. The system is absorbing a shock that is both larger and more persistent than initially assumed.

Supply Disruption Becomes Structural

The Strait of Hormuz remains the central pressure point. Reduced tanker transit volumes and U.S. vessel seizures are compressing exports beyond what surface flow data suggests.

“Data updates point to two new developments and an intensified supply disruption recently – fewer vessels transiting the Strait of Hormuz, and US vessel seizures totalling 8 mmbbl of crude cargo.”

This introduces a second layer of constraint. Flows are not only declining; they are being selectively restricted, distorting traditional export proxies.

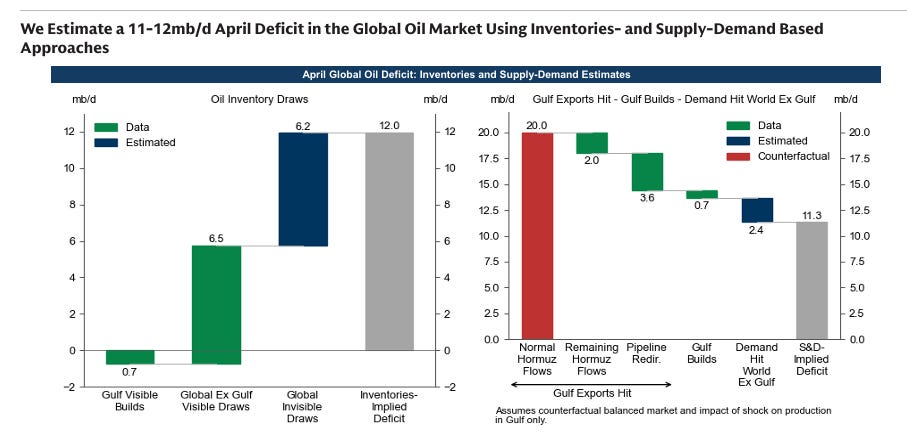

Goldman Sachs quantifies the scale of the disruption.

“We estimate that 14.5mb/d of Persian Gulf crude production losses are driving global oil inventories to draw at a record 11-12mb/d pace in April.”

Both institutions now push normalization into late June, extending the duration of the shock.

“The earliest date of a Strait reopening looks likely to slip from May to June.”

Longer timelines increase operational risks. Reservoir pressure declines and restart inefficiencies raise the probability that part of the lost supply becomes persistent, introducing capacity scarring.

Inventory Depletion and Non-Linear Price Risk

The transmission from supply shock to price is occurring through inventories. Drawdowns are accelerating into record territory.

This scale shifts inventories from buffer to signal. As stocks decline, pricing behavior becomes increasingly non-linear.

“Global visible total oil inventories are likely to reach the lowest level on record… even in the benign scenario.”

At critical thresholds, price formation moves away from marginal cost and toward scarcity pricing. The system begins to embed uncertainty around replenishment and supply reliability.

Demand Weakness Is Insufficient

Demand is adjusting, but not enough to offset the shock.

“We assume that global oil demand falls on a year-over-year basis by 1.7mb/d in 2026Q2… given the jump in refined product prices.”

Higher product prices and shortages are suppressing consumption, particularly in price-sensitive regions. However, the scale of demand destruction remains well below the magnitude of supply loss.

The adjustment is also uneven. Weakness is more visible in China through declining refinery runs, while U.S. demand remains closer to seasonal norms. This fragmentation limits the ability of demand to rebalance the system efficiently.

Contributor posts published on Zero Hedge do not necessarily represent the views and opinions of Zero Hedge, and are not selected, edited or screened by Zero Hedge editors.

Loading...