The Fed’s Great Illusion

What’s behind the numbers?

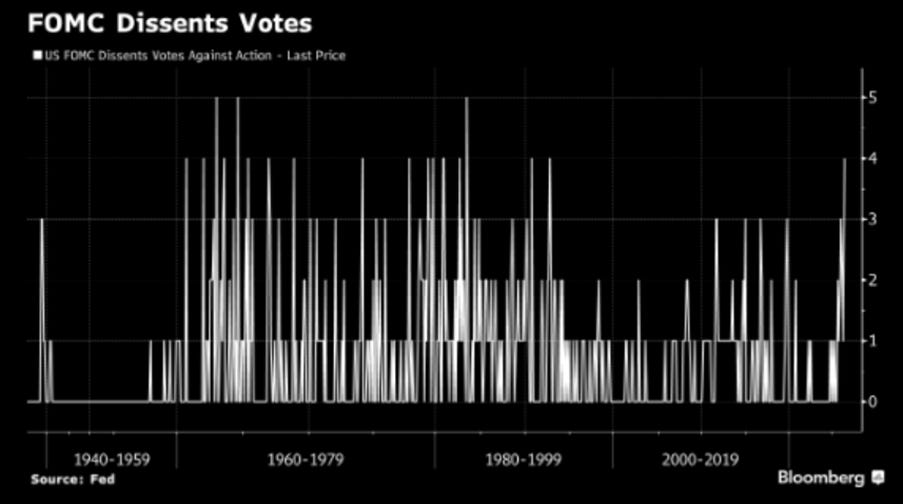

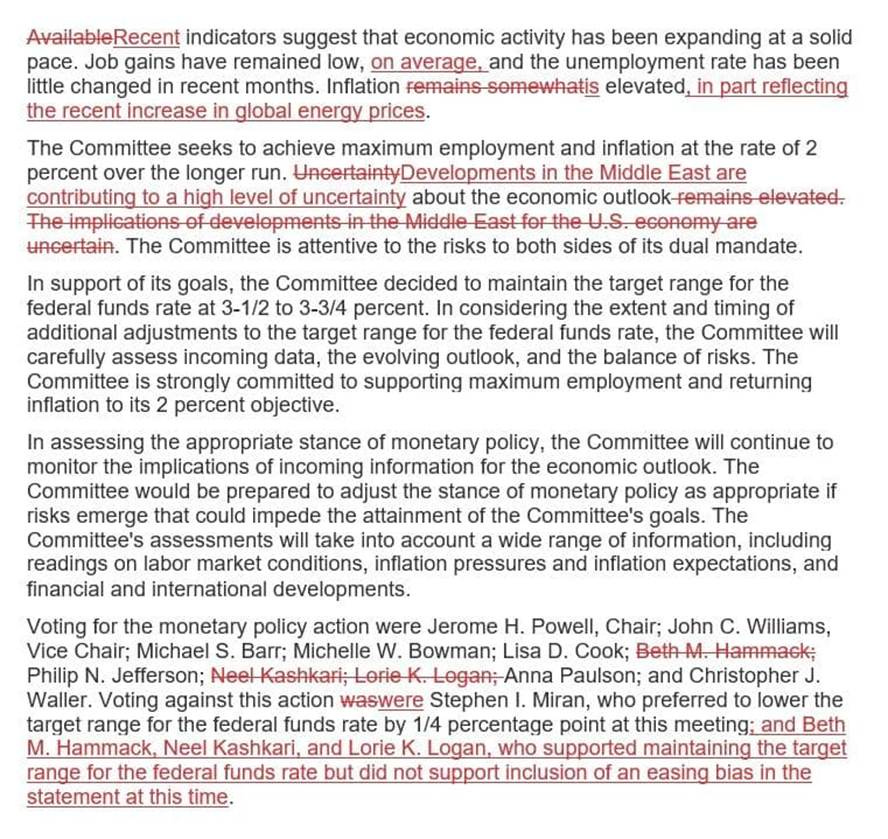

As predictably as a well-rehearsed policy script, the Federal Reserve voted 8–4 to keep rates neatly parked at 3.5%–3.75%, with Jerome Too Late presiding over his most divided meeting in decades. Four dissents added a touch of drama—some arguing against easing, one pushing for cuts—because nothing signals clarity quite like policymakers disagreeing in every possible direction while doing absolutely nothing.

The Federal Reserve helpfully upgraded Middle East risks from “uncertain” to “very uncertain,” then delivered a statement so finely balanced it managed to say everything and nothing at once. Some officials even dissented over an “easing bias” that isn’t explicitly there—apparently spotting cuts hidden between the lines. In short, maximum transparency achieved: the Powell era ends with a masterclass in signalling without actually signalling.

In his final press conference as Fed Chair, Jerome Too Late confirmed he will remain on the Federal Reserve Board of Governors until at least the resolution of an ongoing investigation, potentially extending his tenure through 2028. While he pledged to maintain a low profile and not interfere with incoming chair Kevin Warsh, the decision breaks with precedent and limits Donald Copperfield’s ability to appoint a replacement, adding a layer of institutional and political complexity to the leadership transition.

Dissents within the Federal Reserve and remarks from the Central Banker In Chief highlight the growing cross-currents shaping the policy outlook. Rising oil prices are exerting clear upward pressure on headline inflation, while the extent of pass-through into core inflation remains uncertain. At the same time, consumer resilience—partly supported by tax refunds—may prove temporary, with higher fuel costs likely to weigh on spending power later in the year. At his press conference, Powell characterized the leadership transition at the Federal Reserve as orderly and routine, but historical precedent suggests markets may not be as composed. Periods of Fed chair turnover have often coincided with heightened volatility and notable drawdowns in the S&P 500, even when medium-term returns were mixed. In this context, any shift toward more hawkish pricing following the latest meeting could increase near-term downside risks for equities.

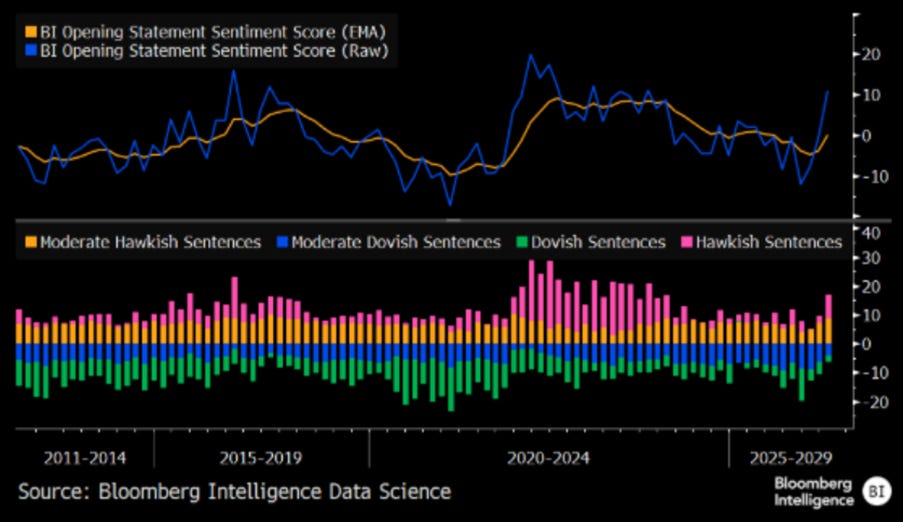

Powell’s opening remarks may not have moved markets immediately, but they signaled a subtly more hawkish tone from the Federal Reserve. NLP-based sentiment analysis points to a shift away from dovish language toward levels historically associated with tightening bias. While a rate hike does not appear imminent, the initial market reaction toward a more hawkish interpretation seems around the corner.

Thoughts.

While Wall Street and The Manipulator In Chief continue their favorite magic trick—convincing investors that the Federal Reserve can steer the business cycle—the reality is less enchanting: in every inflationary bust driven by rising oil prices, the Fed has historically been forced to raise rates, not cut them.

FED Fund Rate (purple line); S&P 500 Index to Oil ratio (green line); 7-Year Moving Average of S&P 500 Index to Oil ratio (red line).

The idea that central banks—especially the Federal Reserve—are all-seeing economic Jedi masters calmly steering the global economy through every storm is one of the greatest comedy sketches ever performed on Wall Street. The script assumes they can tweak interest rates with the finesse of a brain surgeon: trim inflation here, boost growth there, smooth the cycle like a freshly ironed shirt. In reality, history—particularly during energy shocks and good old-fashioned stagflation—shows something closer to a group chat reacting three weeks late to a crisis that already exploded. Less “surgical precision,” more “frantically Googling what just happened,” with results that range from delayed to delightfully ineffective.

US CPI Energy YoY Change (blue line); FED Fund Rate (red line).

When it comes to rising food prices, the Federal Reserve suddenly looks like a chef armed with a calculator trying to stop a boiling pot by adjusting the kitchen clock. Interest rates can go up, down, or sideways, but none of it magically produces more wheat, lowers fertilizer costs, or convinces chickens to lay eggs faster out of respect for monetary policy. As grocery bills climb, the Fed can only stand there, tightening policy like someone turning down the music at a party where the real problem is the house is on fire. In short, you can hike rates all you want—bread still costs more, and...

Read more and discover how to trade it here: https://themacrobutler.substack.com/p/the-feds-great-illusion

Visit The Macro Butler Website here: https://themacrobutler.com/

Join The Macro Butler on Telegram here : https://t.me/TheMacroButlerSubstack

Register your interest to The Macro Butler World Economic Summit 2026 here:

https://themacrobutler.substack.com/p/the-macro-butler-world-economic-s…

You can contact The Macro Butler at info@themacrobutler.com

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence