From Fuel to Food: The Bite of Stagflation

What’s behind the numbers?

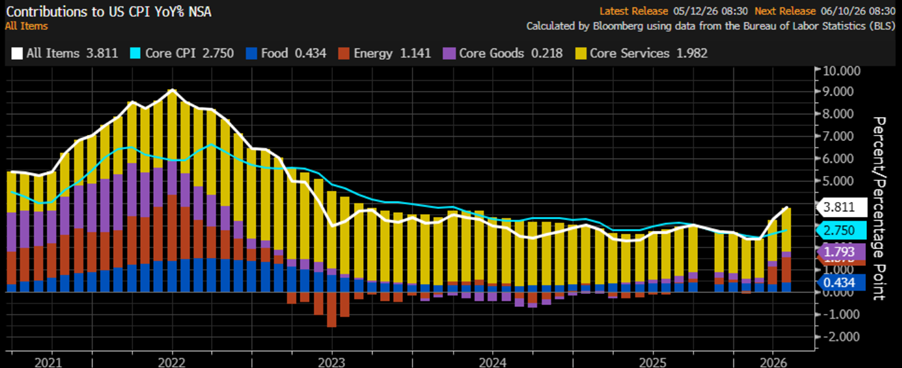

The fourth CPI print of the year delivered exactly what Wall Street ordered: a beautifully airbrushed +0.6% MoM, while YoY inflation came in at +3.8% — just a tiny “unexpected” upgrade from last month’s +3.3%. Apparently, inflation is only transitory when you zoom out far enough. Underneath the soothing headline theatre, food inflation slowed from its fastest annual surge since September… only to remain the hottest since November — and that’s before fertilizer shortages begin turning grocery aisles into luxury boutiques. Meanwhile, energy prices bounced back to their highest yearly increase since November 2022, because nothing says “price stability” quite like paying more for literally everything that moves.

Welcome to the opening act of Inflation Wave 2. Once fertilizer shortages and energy shocks fully leak into the data, consensus economists may finally have to retire the word “temporary” for good.

Core CPI delivered another thrilling episode of “nothing to worry about”: +0.4% MoM and +2.8% YoY, conveniently landing just above forecasts and last month’s reading — because apparently inflation persistence is now considered a sign of economic resilience.

The real star of the performance was core services, the 76%-of-the-basket heavyweight that policymakers keep insisting is “normalizing.” Instead, it quietly accelerated to +2.48%, its highest level since last September. But don’t worry, we’re assured this is all perfectly manageable as long as nobody looks at the trend. Translation: inflation is behaving impeccably right before fertilizer shortages, energy spikes, and petrochemical supply-chain chaos arrive fashionably late to turn “soft landing” forecasts into collector’s items. Enjoy this brief moment of statistical serenity before the second inflation wave starts surfing straight through the consensus narrative.

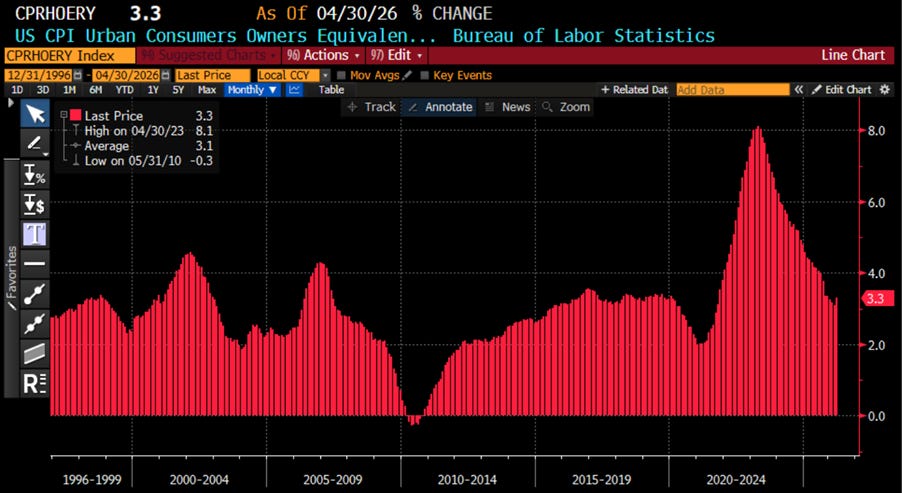

Cue the return of the party pooper for the “Inflation Is Dead” cheerleading squad: Owners’ Equivalent Rent — the CPI’s favourite zombie metric — reaccelerated to +3.3% YoY in April, up from March’s +3.1%, while proudly delivering its “coolest” reading since February 2020. Congratulations everyone, the undead have officially shuffled back into the spotlight. Sure, the metric is still elevated enough to quietly drain household purchasing power like a financial horror movie, but apparently, we’re supposed to celebrate because the zombie is limping instead of sprinting. Progress. Naturally, this is being framed as proof that shelter inflation is “under control,” which in modern central-bank dialect simply means prices are still rising, just not fast enough to cause immediate panic on CNBC.

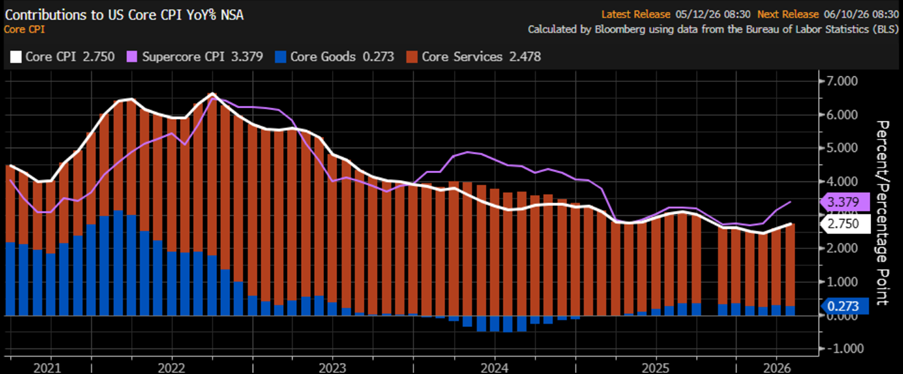

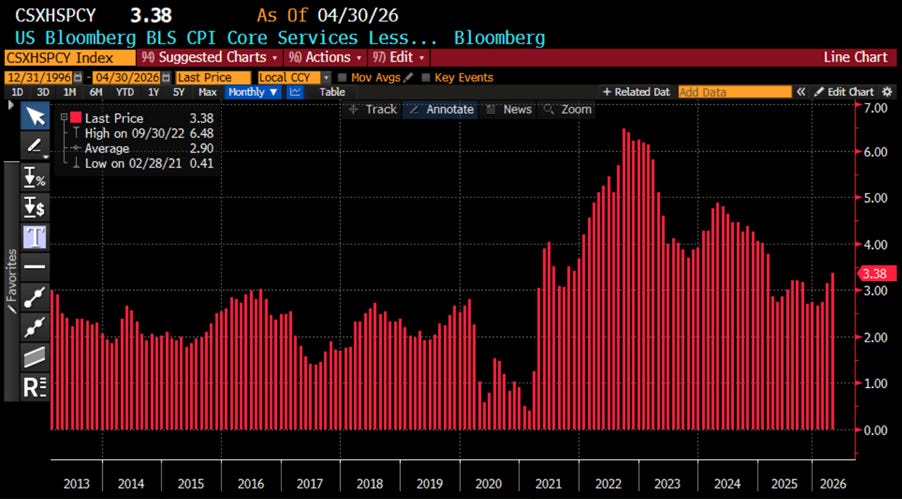

Adding to the “inflation is totally dead, trust us” propaganda tour: SuperCore CPI — core services ex-housing, or as the Fed prefers to call it, “the only inflation metric that matters whenever the headline looks inconvenient” — just reaccelerated to +3.38% YoY from March’s briefly reassuring +2.75%. Congratulations, we’re back to October 2021 territory — that magical era when inflation was still “transitory,” supply chains were “normalizing,” and central bankers were confidently explaining why you absolutely shouldn’t worry about prices exploding everywhere at once. Translation: that wasn’t “Mission Accomplished,” it was just a smoke break between inflation waves.

But by all means, keep repeating that inflation has been defeated. Just ignore rent, food, goods, energy, insurance, and the radical extremism of basic arithmetic. Refill the daily ‘hopium’ prescription, admire the emperor’s fabulous new clothes, and trust that this time the second wave will surely be different.

Thoughts.

April’s CPI will undoubtedly be marketed as a minor inconvenience caused by the Empire’s “tiny and totally successful” Middle East excursion — you know, the one declared won sometime around Hour 1 of Day 1, yet somehow still managing to rattle global oil supply routes 73 days later and counting. Victory has apparently become a subscription service.

For ordinary Americans not employed by the Malthusian Washington Swamp plutocracy, however, grocery prices will continue their inspiring journey upward, while energy costs remind everyone that “disinflation” was less an economic trend and more a seasonal marketing campaign. Inflation didn’t disappear. It just stopped to tie its shoes before sprinting into Wave Two less than five years after the first one.

Meanwhile, policymakers and market cheerleaders keep celebrating “transitory” inflation while preparing the next fiscal spending bonanza and geopolitical adventure package. Because naturally, the solution to too much money chasing too few goods is apparently… even more money chasing even fewer goods. And here’s the inconvenient part: inflation and collapsing institutional trust tend to move together like synchronized swimmers in a controlled demolition. The more households feel squeezed, the louder the official narrative insists everything is “resilient,” “stable,” and “well anchored.”

But don’t worry. Nothing to see here. Just keep trusting the government statistics while your grocery receipt quietly auditions for a Netflix true-crime documentary.

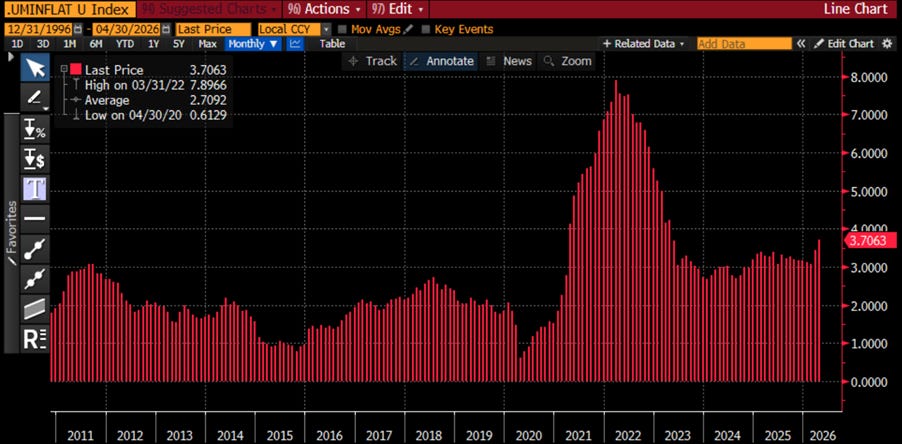

US Umbrella inflation Index (Average of CPI; Core CPI; PPI; Core PPI; Core PCE, 1-year consumer inflation expectations)

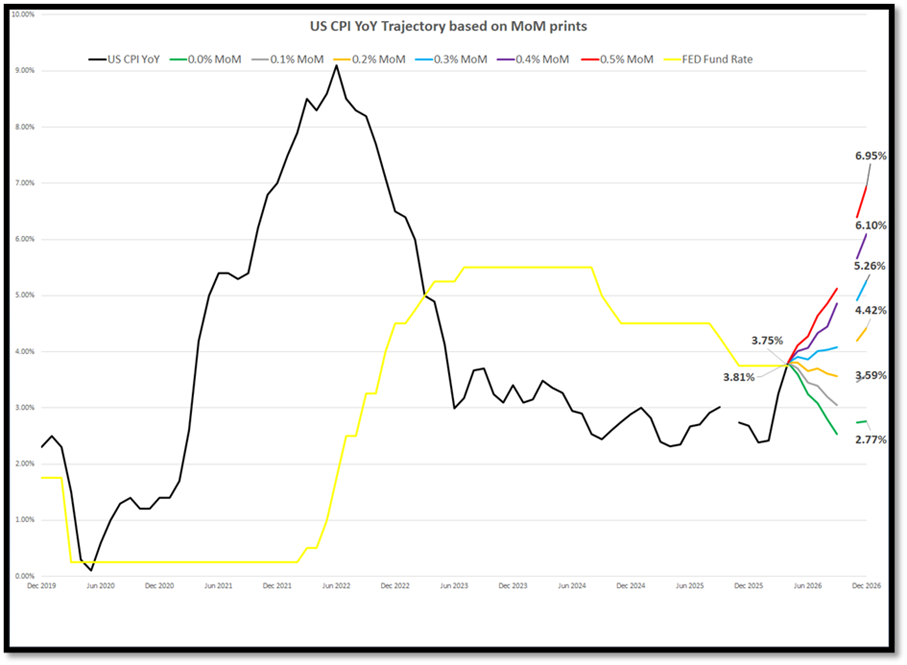

Instead of fantasizing about 2% inflation like it’s another campaign slogan, seasoned investors — unlike certain Wall Street strategists still overdosing on spreadsheet ‘hopium’ — can still perform elementary-school math.

For that miraculous 2% CPI target to materialize by the end of 2026, monthly inflation prints would basically need to hover around or below 0.0% from here onward. Best of luck pulling that off while a freshly politicized Fed chair gets ceremonially crowned and geopolitical conflicts spread faster than a viral TikTok conspiracy thread.

Meanwhile, if monthly CPI keeps printing at a far more realistic 0.3%+, we’re not heading toward “price stability” — we’re cruising straight into roughly 5.3%–7.0% CPI territory by year-end, complete with complimentary media excuses and emergency talking points.

And when reality finally crashes through the narrative, not even Donald Copperfield performing his latest “Central Banker-in-Chief” illusion from beneath a MAGA hat will conceal the fact that cutting rates into an inflationary boom ranked among the Fed’s more spectacular policy magic tricks.

Bonus round: all those delightful shortages, shipping disruptions, and energy shocks are lining up perfectly to collide with midterm election season — right when voters begin asking why their grocery bills now require small-business financing.

Abracadabra: your purchasing power vanished somewhere near the Strait of Hormuz, but thankfully the official CPI basket assures you inflation expectations remain “well anchored.”

Food inflation, the Master might say, is like a humble bowl of rice: often overlooked—until it is empty. Many mistake it for a mere annoyance at the market stall, a few extra coins for vegetables or grain. Yet in truth, it is less a nuisance and more a quiet rebellion of the natural order—one that has a habit of humbling emperors and economists alike. While central bankers sit in polished rooms contemplating “core inflation,” carefully trimmed and perfumed like a ceremonial garden, food inflation arrives uninvited, muddy boots and all. It does not ask for debate; it simply tightens the belt—sometimes literally.

In essence, food inflation is the persistent rise in the price of what sustains life itself. It is born not from a single cause, but from a rather unruly family gathering energy costs, broken supply chains, unpredictable weather, ambitious politicians, diluted currencies, and the eternal mismatch between what people need and what the earth provides. Yet, as any wise observer of the Dao of markets would note, the true root lies deeper. The journey of rising food prices begins not in the quiet dignity of the fields, but in the noisy, smoky ambition of oil wells—where the first seeds of inflation are, quite ironically, not planted, but pumped.

The Master, observing the markets as one might watch the seasons, would note a curious rhythm: when oil rises, food quietly follows—though never in haste, always with a delay of three to six months, as if contemplating the journey. This is no coincidence, but the natural unfolding of cause and effect. Energy, like qi, flows through all things, and agriculture is no exception. Modern farming, despite its pastoral appearance, is less a dance with nature than an alchemy of hydrocarbons into calories. The humble grain, it turns out, drinks as much from the oil well as from the rain. Fertilizers are born of natural gas, tractors feast on diesel, irrigation hums with energy, and ships carry harvests across oceans at the mercy of fuel. Thus, at every step—from soil to spoon—energy leaves its invisible...

Read more and discover how to trade it here: https://themacrobutler.substack.com/p/from-fuel-to-food-the-bite-of-sta…

Visit The Macro Butler Website here: https://themacrobutler.com/

Join The Macro Butler on Telegram here : https://t.me/TheMacroButlerSubstack

Register your interest to The Macro Butler World Economic Summit 2026 here:

https://themacrobutler.substack.com/p/the-macro-butler-world-economic-s…

You can contact The Macro Butler at info@themacrobutler.com

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence