Is The Fed's Worst Nightmare Actually The Greatest Opportunity for Investors?

(Written by Bert Dohmen & Dion Dohmen, contains excerpts from our latest May 17, 2026 Wellington Letter)

The most important question we are focusing on now is, “could the potential of accelerating inflation be the market’s propellant?”

We believe the biggest investment theme for the next few years, which should enable our readers and smart traders/investors to make a fortune, is inflation.

Although we believe a stock market correction is likely in the coming months, the longer-term picture looks similar to the late 1970’s.

You see, inflation can actually be a positive factor for many stocks, especially those in a handful of sectors. It happened about 46 years ago.

That is counterintuitive, as it was in 1978 when we correctly predicted that. Of course, we don’t know if those in charge in Washington will follow the same agenda this time.

Over the past several months, we have been writing about the growing similarities between now and the historic period between 1978 to 1980 when our members were able to profit greatly. Not only in gold and silver, but many other commodities that soared in price.

This is why we have been saying the propellant for the recent rise in the stock market indices could be the same forces that drove the markets higher in the late 1970’s.

Currently, everything has lined up perfectly, and this time the opportunities may be even greater.

The first confirmation signal of our forecast was the upside breakouts of the commodity indices. This gave us more conviction in our comparison between the two periods.

Last week, we got further confirmation of our analysis of the past 6 months or more as the April CPI (+3.8%) and PPI (+6.0%) showed inflation is soaring. These are things they can no longer hide.

In 1978, just one year after we founded our firm, Dohmen Capital Research, the new Fed chair (T. William Miller) declared he would not fight inflation with “tight” money but would do it with higher interest rates. That was the reason we forecasted at the time we would see double digit inflation, a 20% prime rate, and soaring stocks.

And that’s exactly what happened: from 1978-1980 inflation climbed to double-digits and the prime rate soared to 20% in 1980, and later to 21.5%, as we had forecast.

Although those moves initially turned most analysts bearish on the market, we said in 1978 that inflation would be bullish for many stocks.

It happened. Our forecast was called “absurd” by a prominent chief economist of a major Wall Street firm, who said stocks could not rise with rising interest rates. He was wrong.

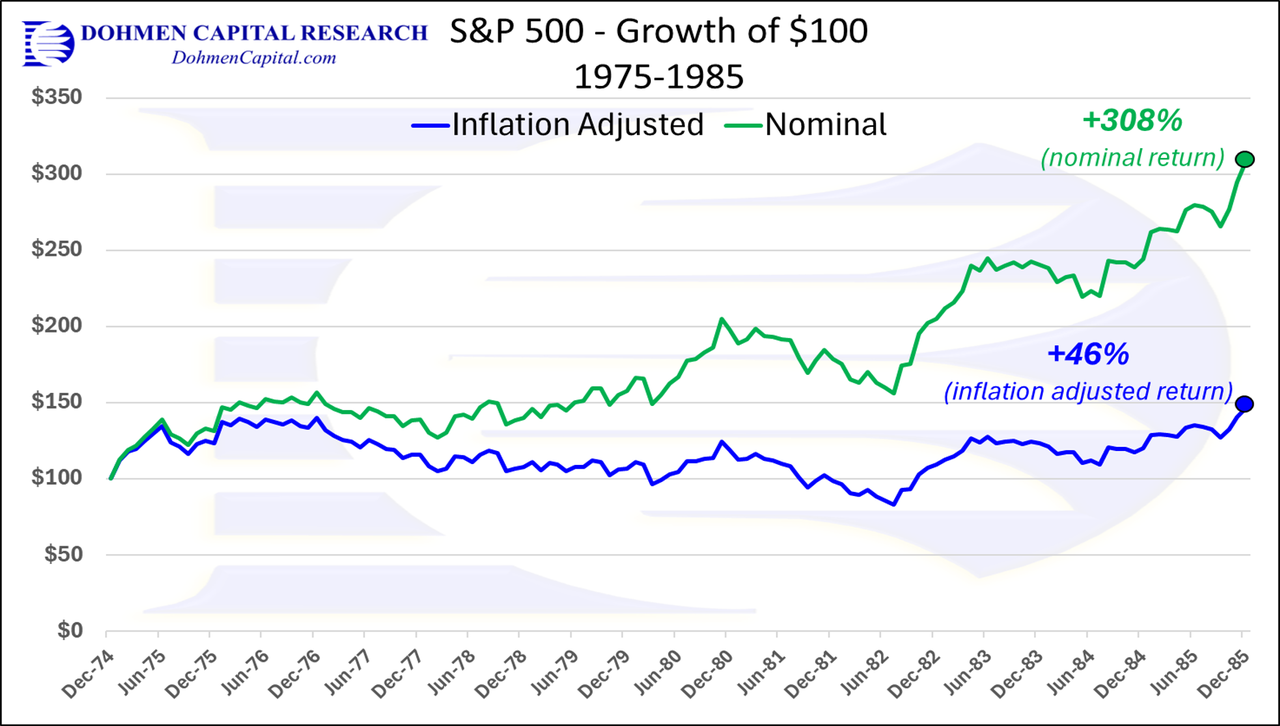

The chart below shows how the S&P 500 did during 10 years of 1975 to 1985, nominal vs inflation adjusted. It shows the growth of $100 starting in 1975.

The S&P 500 rose 308% during that period (green line) as it was driven by inflation. The bottom line (blue) shows the S&P 500 returned just 46% on an inflation-adjusted basis.

Note that inflation was the big driver for the nominal stock indices (green line), which is the price you see on financial TV. The $100 would have grown to $308 in 10 years. And you pay taxes on the illusionary inflation gain. It is actually not much of a gain at all once you factor out inflation and taxes. Here you can see how inflation makes important metrics very deceptive.

On the chart above you can see the big upsurge in the market lasted until late 1980. That’s when Fed chair Volcker actually fought inflation by tightening money. Then, after a market correction and bear market through late 1982, the market rallied strongly again.

Below is the yearly performance below of the S&P 500 from 1975 to 1981 with context.

- 1975: +37.20% nominal return; market recovery following the 1973-1974 recession; SEC abolishes fixed commission rates ("May Day")

- 1976: +23.84% nominal return; strong rebound continues; significant influx of financial stocks added to the index

- 1977: -7.18% nominal return; index dipped due to inflation and economic uncertainty

- 1978: +6.56% nominal return; index rebounded

- 1979: +18.44% nominal return; oil shocks and inflation pressured stocks

- 1980: +32.42% nominal return; index surged on strong corporate earnings

- 1981: -4.91% nominal return; index fell on high interest rates (and “tight “ money)

Look at the years of easy but expensive money and the great nominal performance of the indices (1979: +18.44% and 1980: +32.42%).

These are the periods when interest rates went to double digits, and as we had predicted, stocks soared.

That seems like it is being repeated now although “official inflation” numbers are being artificially reduced in order to hide the true double-digit inflation we already have.

CONCLUSION: We seem to be going into a similar type of environment at the late 1970’s at this time. That would mean informed, smart investors, who are not greedy, can do well.

Most analysts in the media were not working in the market at that time. We were there and were even one of the very few who predicted what unfolded. In fact, we don’t know anyone else who did.

As always, we will continue to put our 50 years of experience successfully guiding investors in the markets to work for our valued readers, helping them to protect and grow their wealth while most investors will see their assets depreciate.

You can read more about our current analysis, forecasts, and how we examine the markets in our latest research report, available FREE for a limited time to ZeroHedge readers.

In this 18-page report, we explain what could be “The Trigger For The Next Global Financial Crisis.” Keep in mind this report focuses more on longer-term vulnerabilities of the global markets and is separate from our intermediate term forecasts written above.

You can get your FREE copy today at DohmenCapital.com/SpecialReport2026

Wishing you successful investing,

Bert Dohmen, Founder

Dion Dohmen, Vice President

Dohmen Capital Research