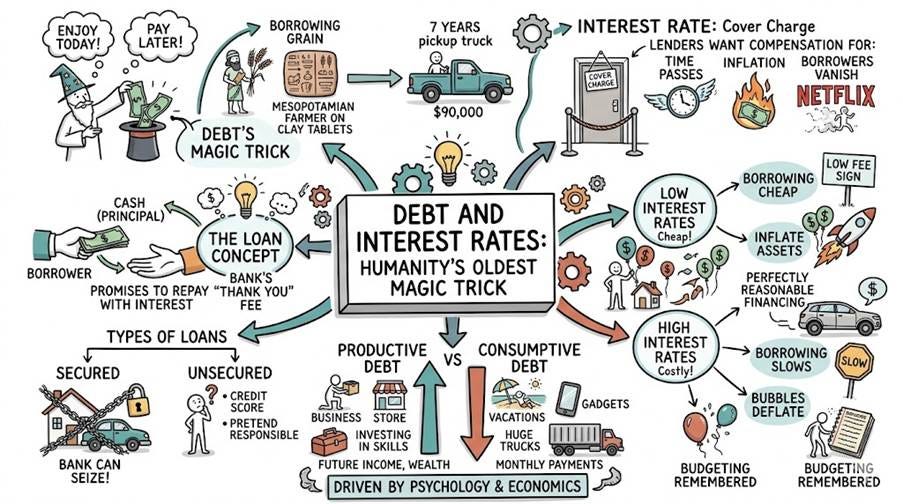

A World on Borrowed Time

Debt is basically humanity’s oldest magic trick: enjoying money today and praying your future self-figures it out later. From ancient Mesopotamian farmers borrowing grain on clay tablets to modern consumers financing a $90,000 pickup truck over seven years, the principle has not changed much. A loan is simply the official contract behind this beautiful act of financial optimism. The lender hands over the cash — called the principal — while the borrower promises to repay it with interest, otherwise known as the bank’s “thank you for the risk” fee. Some loans are secured, meaning the bank can seize your house or car if things go badly, while unsecured loans rely entirely on your credit score and your ability to convincingly pretend you are financially responsible.

Interest Rate is basically the financial system’s cover charge. Lenders want compensation because time passes, inflation destroys purchasing power, and borrowers occasionally vanish like Netflix passwords after a breakup. Low interest rates make borrowing cheap, inflate asset prices, and convince consumers that financing a luxury SUV for seven years is perfectly reasonable. High rates do the opposite: borrowing slows, bubbles deflate, and suddenly everyone remembers what a budget is.

Not all debt is created equal. Investment debt is the kind that at least has the decency to try making you richer in the future — borrowing money to build a business, buy productive assets that can generate future income. Consumption debt, on the other hand, is financial time travel: enjoying tomorrow’s paycheck today on things that will probably lose value faster than your New Year’s resolutions. A loan used to expand a factory and build a bridge may create jobs and cash flow; a credit card used to finance a luxury vacation mostly creates Instagram stories and monthly payments. One debt plants a tree. The other buys a very expensive cocktail under a palm tree.

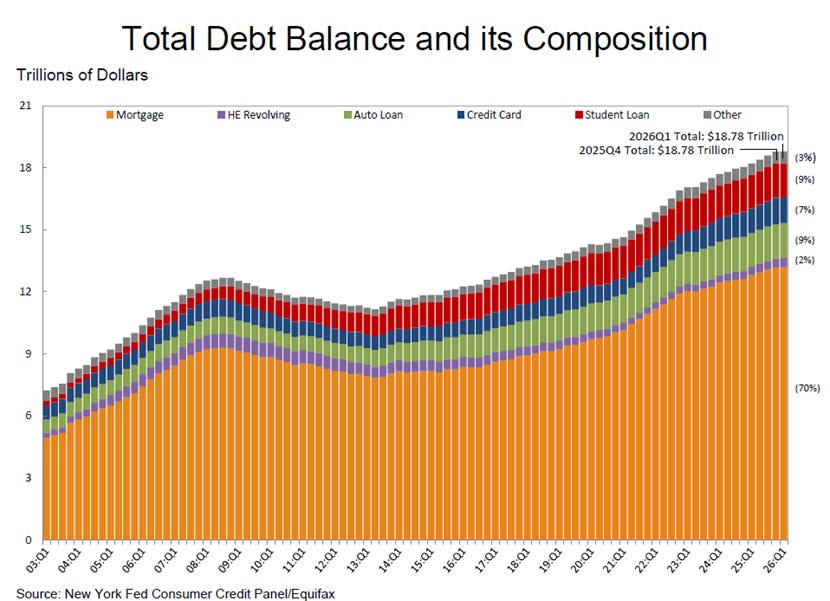

Mortgage debt is America’s favorite long-term relationship with a bank. It allows households to buy a home today and spend the next 30 years convincing themselves they are “building equity” rather than paying mostly interest for three decades. With roughly $12 trillion in outstanding balances, mortgages are the largest form of consumer debt in the US economy. The housing boom of 2020–2022, fuelled by ultra-low rates below 3%, turned millions of Americans into amateur real estate speculators overnight. Then rates jumped above 7%, creating the famous “lock-in effect”: homeowners with cheap mortgages are now financially glued to their houses because moving would mean replacing a bargain mortgage with monthly payments that resemble luxury car leases for a medium-sized suburban home.

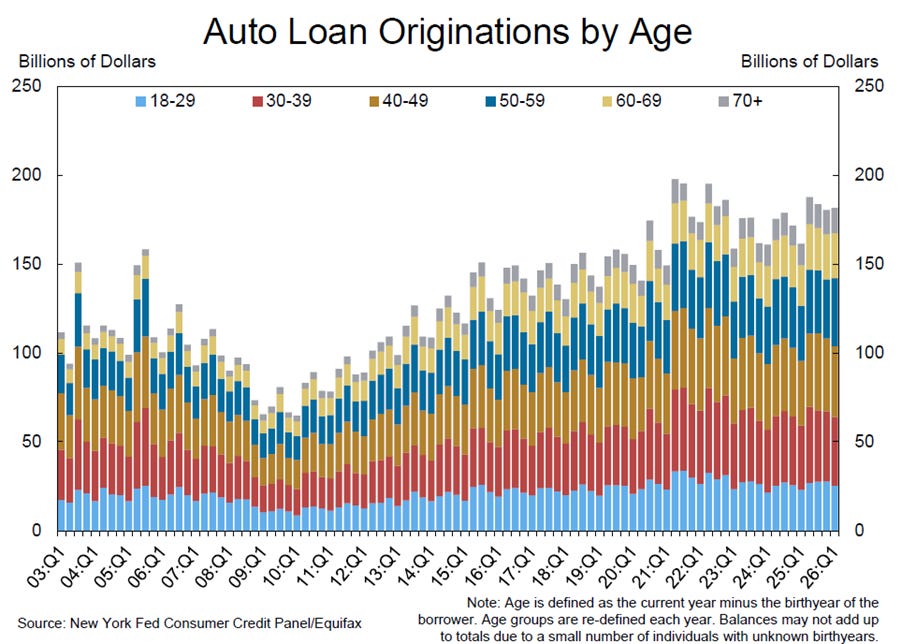

Auto loans are America’s preferred method of turning a depreciating asset into a long-term financial commitment. Consumers now routinely borrow over $40,000 to buy vehicles that lose value faster than politicians lose campaign promises. Thanks to rising car prices and seven-year financing terms, cars have evolved from transportation tools into rolling monthly payment subscriptions. Even better, many borrowers end up paying nearly luxury-vacation money in interest for a vehicle worth half its price by the time the loan is finally paid off. Meanwhile, the rapid growth of subprime auto lending means the industry has quietly recreated the same “what could possibly go wrong?” energy that once fuelled the housing bubble.

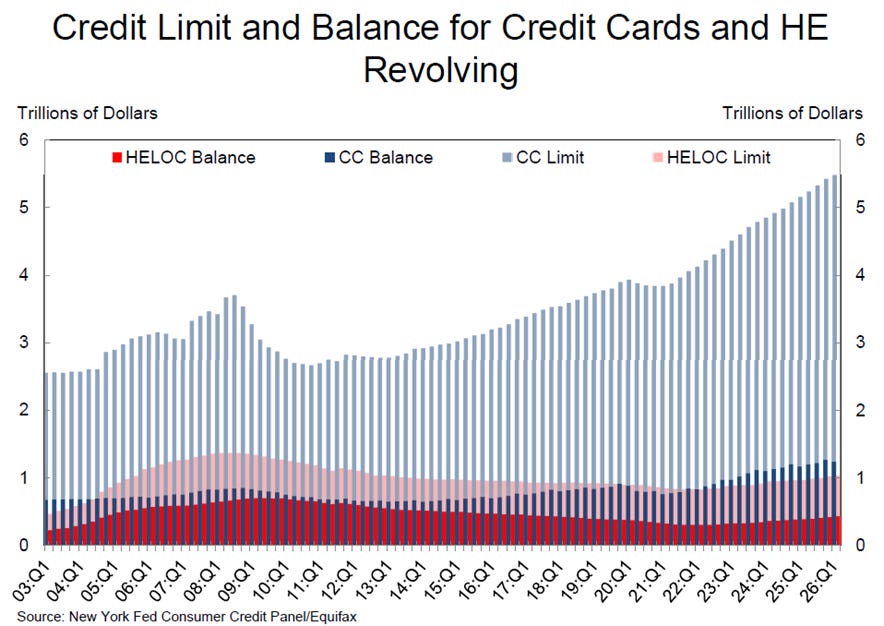

Credit card debt is the financial equivalent of setting your wallet on fire very slowly. Americans now carry over $1 trillion in revolving credit card balances, often at interest rates above 20% — high enough to make loan sharks look competitively priced. The system is beautifully designed for banks: minimum payments are so small that borrowers can spend decades paying interest on restaurant meals, groceries, and gadgets already forgotten or broken. The recent surge in balances is less a sign of consumer confidence than a national distress signal: when households start financing eggs and gasoline with credit cards, the economy is no longer booming — it is over drafting.

Student loan debt is the uniquely modern experience of paying university prices for a degree and then discovering the real major was compound interest. Americans now owe nearly $2 trillion in student loans, often borrowed without much consideration for whether the future salary can actually repay the debt. Universities happily raised tuition for decades knowing federal loans would keep flowing, while millions of graduates entered adulthood carrying debt large enough to delay buying homes, starting families, or occasionally even ordering guacamole without financial anxiety.

The modern American consumer economy rests on four great pillars of debt: the mortgage loan, the auto loan, the credit card, and the student loan. The mortgage finances the house you barely leave because you are working to pay for it. The auto loan finances the car you use to drive to the job paying for the house. The credit card finances everything your salary no longer covers after paying for the house and the car. And the student loan finances the degree required to qualify for the job needed to pay for the first three. Together, these four pillars transformed the American Dream into what increasingly resembles a...

Read more and discover how to trade it here: https://themacrobutler.substack.com/p/a-world-on-borrowed-time

Visit The Macro Butler Website here: https://themacrobutler.com/

Join The Macro Butler on Telegram here : https://t.me/TheMacroButlerSubstack

Register your interest to The Macro Butler World Economic Summit 2026 here:

https://themacrobutler.substack.com/p/the-macro-butler-world-economic-s…

You can contact The Macro Butler at info@themacrobutler.com

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence