Continues here

Higher in Steps: UBS Sees Copper Marching Toward $15,500

Higher in Steps: UBS Sees Copper Marching Toward $15,500

Authored by GoldFix

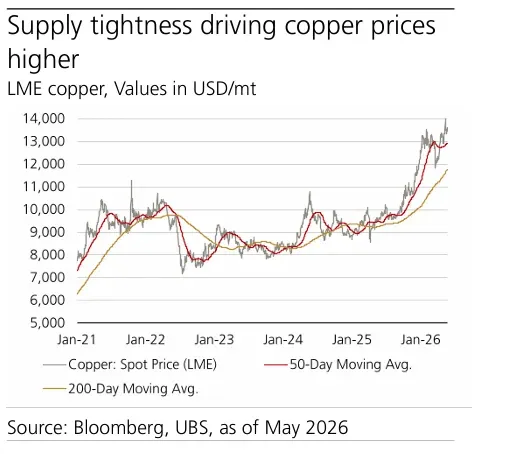

The copper market continues to trade as a supply-constrained industrial system rather than a cyclical commodity market. In a May 22 report titled Higher in Steps, analysts at UBS argue that structural shortages across concentrates, scrap, sulfur, and refined output are forcing prices steadily higher despite mixed global growth signals.

UBS now forecasts copper prices reaching USD 14,000/mt by September 2026, USD 14,500/mt by year-end, USD 15,000/mt by March 2027, and USD 15,500/mt by June 2027. The bank maintains a constructive stance and continues to recommend long exposure to copper, particularly during price pullbacks.

The Market Is Tightening from Multiple Directions

The core thesis behind the report is simple: copper supply growth is struggling to keep pace with electrification-driven demand growth.

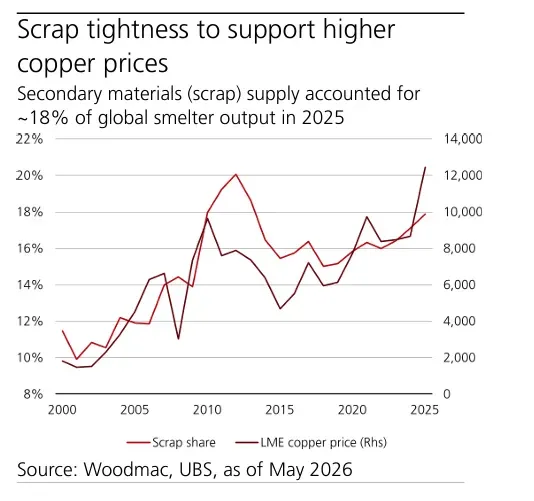

According to UBS, sulfur shortages in China have intensified after Beijing imposed new sulfuric acid export restrictions. That has raised costs for higher-cost leaching operations while simultaneously tightening the broader refining chain. At the same time, copper concentrate and scrap availability remain constrained, creating aggressive competition among smelters for feedstock.

Treatment and refining charges (TCRCs), which are often viewed as a gauge of concentrate availability, have effectively collapsed.

“2026 Annual benchmark global treatment and refining charges (TCRCs) [fell] to USD 0/mt… and spot charges below USD -100/mt amid fierce competition among smelters.”

That matters because negative treatment charges imply smelters are effectively paying to secure material. In commodity markets, this is usually a sign of severe upstream tightness.

The report also highlights tightening scrap flows. China’s stricter tax compliance standards and invoice quotas are reducing available recycled material, while Japan is increasingly retaining domestic scrap as its own smelters shift toward recycled copper processing.

Electrification Demand Remains Intact

Despite slowing global manufacturing activity, UBS argues the larger structural demand trend remains firmly supportive for copper.

The bank estimates global copper consumption will rise 2.8% in 2026, driven primarily by grid investment, electric vehicle adoption, renewable infrastructure, and the continued expansion of data centers.

This is an important distinction. Traditional cyclical demand indicators, such as manufacturing PMIs, have softened around the margins, yet copper demand tied to electrification infrastructure continues to expand.

China remains central to that story.

While January-April copper imports into China declined year-over-year, April imports alone still rose 2.3%

Free Posts To Your Mailbox

Contributor posts published on Zero Hedge do not necessarily represent the views and opinions of Zero Hedge, and are not selected, edited or screened by Zero Hedge editors.

Loading...